- Access finance

- Case studies

-

Informing today's market

Financing tomorrow's trade

Soft commodities trader

Due to increased sales, a soft commodity trader required a receivables purchase facility for one of their large customers - purchased from Africa and sold to the US.

Metals trader

Purchasing commodities from Africa, the US, and Europe and selling to Europe, a metals trader required a receivables finance facility for a book of their receivables/customers.

Energy trading group

An energy group, selling mainly into Europe, desired a receivables purchase facility to discount names, where they had increased sales and concentration.

Clothing company

Rather than waiting 90 days until payment was made, the company wanted to pay suppliers on the day that the title to goods transferred to them, meaning it could expand its range of suppliers and receive supplier discounts.

Get Trade Finance

Informing Today’s Market, Financing tomorrow’s Trade.

-

- Case studies

What is IGST, CGST and SGST?

Access trade, receivables and supply chain finance

We assist companies to access trade and receivables finance through our relationships with 270+ banks, funds and alternative finance houses.

Get Started

Contents

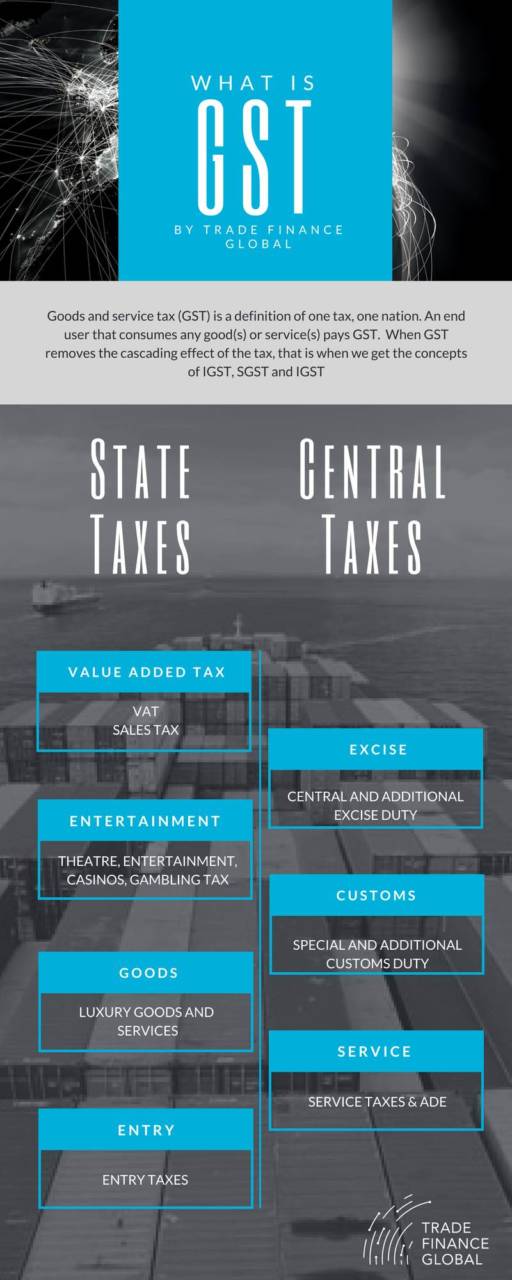

The Goods and Service Tax (GST) is a term signifying one tax, one nation policy. An end-user that consumes any good(s) or service(s) pays the GST. We get the concepts of IGST, SGST and CGST when we observe the ways in which GST removes the cascading effect of taxes.

These terms have the following meanings:

IGST

Integrated goods and service tax

SGST

State goods and services tax

CGST

Central goods and services tax.

GST replaces which taxes?

Before the introduction of GST, there were multiple taxes, such as the service tax, central excise, and state value-added tax (VAT). However, GST is just one tax with three categories—IGST, SGST, and CGST—that depend on whether the performed transaction is intrastate or interstate.

What determines which category of GST is applicable?

We need to understand whether the transaction is an intrastate or an interstate supply of goods and services to determine which category of GST is applicable

Testimonials

A business owner Dipesh from Rajastan had sold his finished goods to Jyoti from Gujarat worth a total value of Rs. 10,00,000. The GST rate is 18%, which is split into a total of 18% of IGST. In this case, the dealer must charge Rs. 180,000 as IGST, which will go to the Centre.

– Dipesh B, Goods Manufacturer

Case Study

Goods Distributor

Trade Finance Global along with their partner freight forwarders and tax assistants helped us file our returns, arrange transportation and sort out our duties in India.

- All Topics

- Key Terms

- Incoterms Resources

- Podcasts

- Videos

- Conferences