- Access finance

- Case studies

-

Informing today's market

Financing tomorrow's trade

Soft commodities trader

Due to increased sales, a soft commodity trader required a receivables purchase facility for one of their large customers - purchased from Africa and sold to the US.

Metals trader

Purchasing commodities from Africa, the US, and Europe and selling to Europe, a metals trader required a receivables finance facility for a book of their receivables/customers.

Energy trading group

An energy group, selling mainly into Europe, desired a receivables purchase facility to discount names, where they had increased sales and concentration.

Clothing company

Rather than waiting 90 days until payment was made, the company wanted to pay suppliers on the day that the title to goods transferred to them, meaning it could expand its range of suppliers and receive supplier discounts.

Get Trade Finance

Informing Today’s Market, Financing tomorrow’s Trade.

-

- Case studies

Home /

Introduction to letters of credit | 2026 guide

Access trade, receivables and supply chain finance

We assist companies to access trade and receivables finance through our relationships with 270+ banks, funds and alternative finance houses.

Get Started

ADVERTISEMENT

Contents

Letters of Credit

Welcome to TFG’s Letters of Credit hub. Find out how we can help you access Letters of Credit to increase your imports and exports to guarantee the payment and delivery of goods – or discover the latest research, information and insights here.

What is a Letter of Credit (LC)?

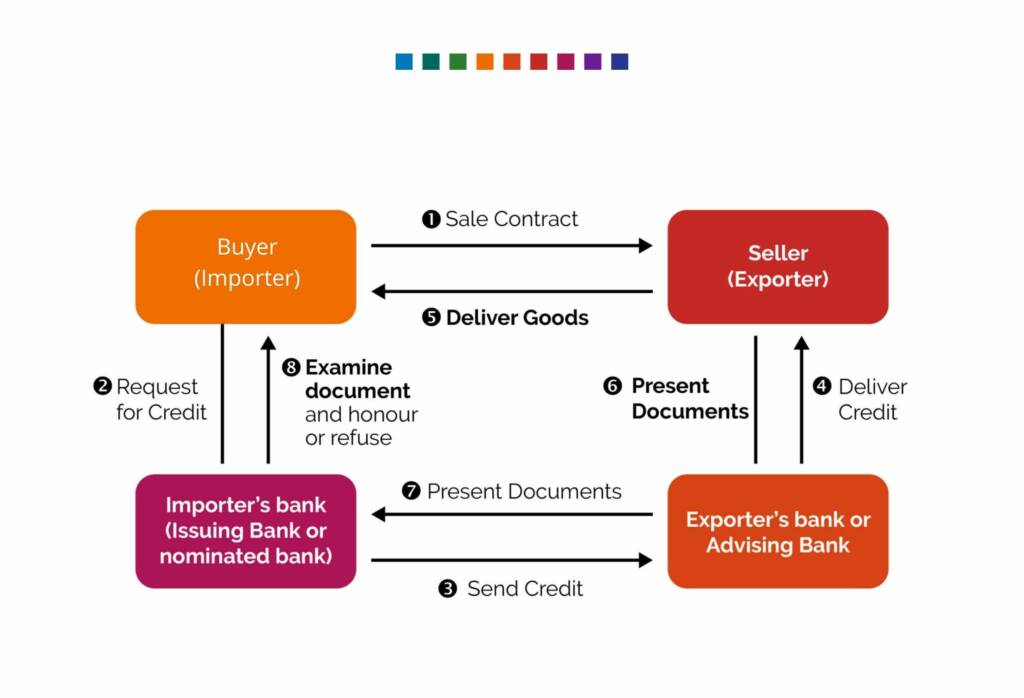

Letters of Credit (also known as documentary credits in the US) are a financial facility issued by a bank that effectively functions as a guarantee to the seller that the buyer in a transaction will pay on time.

How do LCs work?

Letters of Credit (LCs) are used to guarantee payments and facilitate trade, especially in international transactions. When a seller wants assurance of payment, the buyer may offer an LC. This acts as a commitment on the part of the buyer’s bank that the seller will be paid on time, even if the buyer is unable to make the payment themselves.

LCs are regulated by the UCP 600, a set of standards and regulations issued by theInternational Chamber of Commerce (ICC). Information about LCs is transmitted via the Swift messaging platform through one or more MT 700 messages.

Letters of Credit – 2026 update

LCs have been used for years and are a staple of the trade finance industry, so they are unlikely to go through major changes soon. The standards regulating LCs, the UCP 600, were last updated in 2007 and are not set to be reviewed in the near future.

The most significant changes around LCs are being driven by individual countries and their courts. In 2022, the UK High Court considered a case in which the claimant held that an LC’s own terms could incorporate its own credit norms, which differed from those set by the UCP 600. The court ruled that the UCP 600 could not be overridden, continuing the UK’s trend of favouring an international focus on interpreting the regulation.

In the same year, the Central Bank of Egypt made it mandatory for importers to use LCs for international transactions. More recently, in 20225, several senior bankers were convicted in India for a fraud case involving forged LCs, showing that the instrument is still vulnerable to misuse when not properly verified.

There are several critical features of documentary credits/LCs:

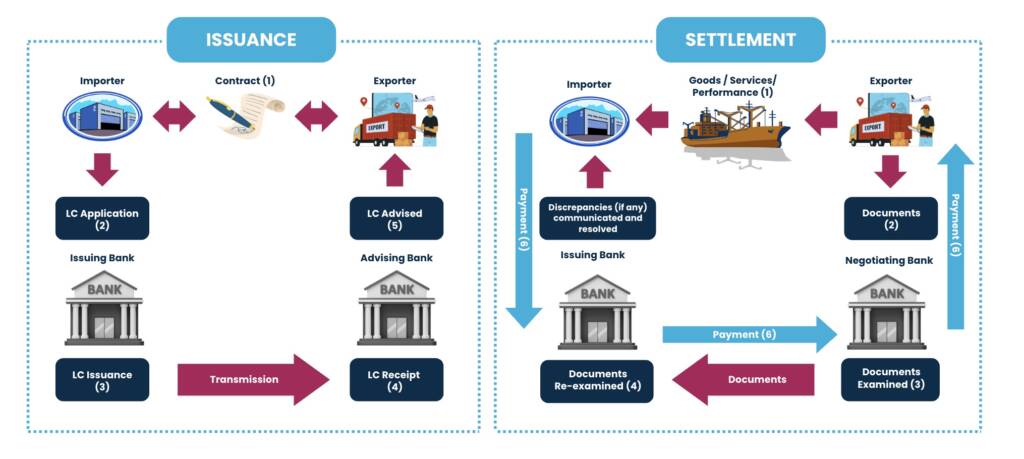

- Irrevocability: LCs constitute an irrevocable undertaking by the issuer to pay the seller. This means that, once issued, the issuing bank cannot revoke or change the credit. A credit can only be amended or cancelled with the consent of the issuing bank, the beneficiary, and the confirming bank.

- Documentary nature: LCs are documentary in nature, so the payment undertakings they contain are conditional upon receipt of documents as stated in the terms and conditions of the credit. The documentation, often detailed and containing information about the shipment and the transaction, can be submitted physically or in electronic form.

- Compliance: LCs are settled only when the documents presented by the beneficiary comply with the letter’s terms and conditions. If the documents contained do not comply or contain discrepancies, the issuing bank may refuse to honour the letter of credit. The bank is only obligated to pay if the non-complying documents are corrected before the credit expires, or if both the applicant and the issuing bank agree to waive any discrepancies.

- Payment mechanism: LCs are effectively a payment mechanism designed to facilitate the settlement of an underlying trade transaction. They function by placing the bank as an intermediary between the buyer (applicant) and the seller (beneficiary): when the buyer receives the goods or services, the seller obtains payment via the credit, which satisfies the buyer’s payment obligations.

- Independence and autonomy: LCs constitute an independent undertaking of the issuing bank and the confirming bank that is separate from the underlying sale or other contract on which it may be based. The principle of autonomy is articulated within the UCP 600, the ICC’s set of rules governing letters of credit, followed by banks all over the world.

LCs are crucial to facilitate trade all over the world and build trust between exporters and importers. They do this by eliminating counterparty risk between sellers and buyers, which is instead shifted to the bank.

LCs are independent of the underlying transaction. Banks will often ask the applicant (usually the buyer) to provide collateral before issuing a Letter of Credit. This means that banks will only deal with documents – not with goods, services, or transactions to which the documents may relate.

Diagram: LC processing

Diagram: Issuance & Settlement

Access Letters of Credit and Documentary Credits with TFG

The TFG team works with the key decision-makers at 270+ banks, funds and alternative lenders globally, assisting companies in accessing Letters of Credit.

Our international team are here to help you scale up to take advantage of trade opportunities. We have a team of sector specialists, from fuel experts to automotive gurus.

Often the financing solution that is required can be complicated, and our job is to help you find the appropriate trade finance solutions for your business.

Read more about Trade Finance Global, and how we can help you with your Letter of Credit queries, here.

Learn more

Look no further. We’ve put together our feature insights, research and articles: you can catch the latest thought leadership from TFG, listen to podcasts, and digest the latest news from the LC community right here.

Frequently Asked Questions

t

Our trade finance partners

- Letters of Credit / Documentary Credit Resources

- All Letters of Credit Topics

- Podcasts

- Videos

- Conferences