")

The business world is experiencing its most transformative era. Innovators, entrepreneurs, and forward-thinking enterprises are embracing Distributed Ledger Technology (DLT) solutions to bring revolutionary changes to supply chains, global trade, international payments, the world’s food supply, and more. These changes are strengthening trust and transparency. This article examines the meaning of the term “DeFi” and dives deeper into some of its more nuanced technological aspects, providing insight into its foundation and the potential hurdles that it may face on the path ahead.

What is Defi?

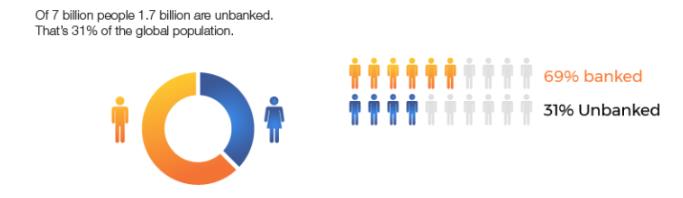

DeFi – ‘Decentralized Finance’ – is the latest term in the world of FinTech, RegTech, cryptocurrencies, and digital assets. DeFi protocols aim to bank the unbanked with intuitive applications, leading to greater competition and diversity in the financial system while reducing the systemic importance of some existing entities.

Decentralized Finance may first appear similar to “Financial technology” (FinTech for short), which also aims to use technology in order to improve financial services. However, the key difference between the two is that FinTech merely builds upon traditional financial infrastructure, while DeFi is built with underpinnings in DLT.

DeFi is a peer-to-peer electronic financial instrument system and refers to projects that are using cryptographic tokens and blockchain to enable anyone to issue, transfer, and own financial instruments. The backbone of all DeFi protocols and applications are “Smart Contracts”. The term smart contract generally refers to small applications stored on a distributed ledger and executed by the many computers on the distributed ledger’s network.

While smart contracts are relatively inefficient compared to traditional centralized computing, their advantage is a high level of security. Smart contracts guarantee deterministic execution and allow the resulting state changes to be verified by anyone. When implemented in a secure manner, smart contracts are highly transparent and minimize the risk of manipulation and arbitrary intervention.

Technological Side of Defi

At the core of DeFi, and fundamental drivers of the FinTech and RegTech revolutions, stand a number of new technologies best summarized with the acronym ABCD: Artificial Intelligence, Big Data, Cloud Computing, and Distributed Ledger Technology.

There are five key layers of DeFi, each with its own specific role or purpose:

- The settlement layer consists of the blockchain and its native protocol asset. This layer allows the network to securely store ownership information and ensures that any state changes adhere to the network’s predefined rule set. The blockchain can be seen as the foundation for trustless execution as it serves as a settlement and dispute resolution layer.

- The asset layer consists of all tokens that are issued on top of the settlement layer. This layer includes the native protocol asset as well as any additional tokens that are based on token standards supported by the blockchain.

- The protocol layer provides specific standards for specific use such as decentralized exchanges, debt markets, derivatives, and on-chain asset management. These standards are usually implemented as a set of smart contracts and can be used by any user (or DeFi application). As a result, these protocols are highly interoperable.

- The application layer creates user-oriented applications that connect to individual protocols. The smart contract interaction is usually abstracted by a web-browser-based user interface, making the protocols easier to use.

- The aggregation layer is an extension of the application layer. Aggregators create user-centric platforms that connect to several applications and protocols. They usually provide tools to compare and rate services, allow users to easily perform otherwise complex tasks by connecting to several protocols simultaneously, and finally combine relevant information in a clear and concise manner

An example of how DeFi might manifest may prove helpful. Perhaps the most successful example so far is the cryptocurrency BitCoin. Libra, the virtual currency proposed by Facebook, is an excellent example that shows how decentralized finance does not necessarily require all parts of the system to be decentralized. Libra’s node function is, at least initially, only partially distributed. This is because the underlying blockchain operates as a private, rather than public, system. The potential liability of the large players that function as nodes of the Libra blockchain provides an important incentive for this approach: their large balance sheet and clear localization mean they would be held liable in case of default, malfunction, or misconduct.

Opportunities for DeFi

There exist a handful of key opportunities for further DeFi development.

Payments and settlements – Service providers in this sector have already begun to incorporate decentralized technologies. For example, foreign exchange platforms that directly match end-users have begun to complement – and in some places replace – traditional interbank payment systems for retail cross-border payments. If decentralized payment and settlement systems achieve scale, this may result in decentralization of record keeping.

Trade finance – This area may benefit from technologies that allow verification of information to take place in a decentralized manner. This is due to a lack of established infrastructure or trusted intermediaries through which to verify information between stakeholders. DLT might enable participants from different sectors – for example finance and freight shipping – to interact and share information in a more verifiable and decentralized manner.

Capital markets – The tokenization of securities – that is, the digital representation of traditional assets using DLT – has the potential to further decentralize capital markets. Smart contracts might become more widely applied and provide an opportunity to further automate certain financial services such as settlement and custody, which are activities that are currently undertaken by traditional financial intermediaries.

Lending – Online lending platforms (and other similar technologies) make lending decisions without relying on conventional financial intermediaries. Such platforms typically carry out credit scoring directly on a granular basis, sometimes making use of novel sources of data on borrowers (such as social networks).

Connectivity – DeFi connects many servers around the globe that are owned, operated, updated, and otherwise influenced by many different entities. While the network structure can reduce the risk of manipulation, as with distributed ledgers, it also enhances two other type of cyber risks. First, the number of access points to the network have multiplied. Each access point provides a cyber risk that needs to be managed. Second, many servers are connected, and new risks may come from this connectivity.

DeFi’s unleashed wave of innovation

New and increasingly innovative institutions and entities are entering the finance world. These firms are helping to drive the transformation for finance and will help the unbanked finally join the ranks of the banked.

DeFi has unleashed a wave of innovation, offering exciting opportunities and the potential to create a truly open, transparent, and immutable financial infrastructure. Consisting of numerous highly interoperable protocols and applications, all transactions can be verified by every individual and data is readily available for users and researchers to analyze. This level of security means that individual users will be disincentivized from using multiple platforms for their transactions.

DeFi platforms may remove the complexity added by regulators in the interest of keeping economies walled and will provide retail investors access to commodities, exotic assets, derivatives, foreign currencies and even equity.

Let the transformation begin.

ARTICLE: What is DeFi and Why is Everyone Talking About it?

This article was written by a member of TFG’s 2020 International Trade Professionals Programme. Find out more here.

Disclaimer: The views that have been expressed on this page are that of the author, which may or may not be in line with their company, Trade Finance Global or London Institute of Banking and Finance’s view.

Type a message