Momentum behind updating the framework for Europe-Africa cooperation may have slowed as nations tackle the Coronavirus outbreak, but the pause will only be temporary. Speaking to TFG, Jeff Fallon, Head of Client Coverage at British Arab Commercial Bank (BACB), argues that deeper Africa-Europe integration will be challenging in the new environment, but specialist banking partners are on hand to help.

2020 was set to be a pivotal year for Europe-Africa trade. In March, the EU published its “Comprehensive Strategy with Africa” which laid out a forward-looking roadmap to further deepen the inter-continental relationship in areas such as green growth, energy access and digitalisation. But a few months down the line, and regions have had to divert their efforts almost exclusively onto mitigating the impacts of the Coronavirus outbreak.

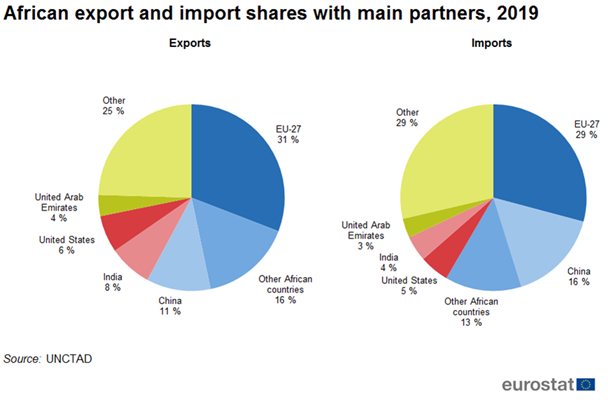

While controlling the social effects of virus remains the priority, Africa now must manage the economic ramifications of the pandemic – and this means keeping trade flowing as much as possible with key trading partners. The continent’s largest, in this respect, is the EU: in 2019, the EU-27 represented 31% of Africa’s exports, mostly comprising of primary goods such as energy, raw materials and food products.[1] Similarly, 29% of Africa’s imports – largely manufactured goods – are from Europe.

Fulfilling the aims of the “Comprehensive Strategy with Africa” is, therefore, crucial in the recovery years ahead for both regions – but a pause in proceedings may well be an opportunity for reflection. Since global supply chains already re-routing due to lockdowns, Africa may well stand to further increase its trade with Europe in the longer term – particularly given the closer geographic proximity compared to some other key partners, such as China. But the commercial benefits must outweigh the risks to ensure that this trade corridor remains attractive to corporates and FIs alike, and the Coronavirus has changed this landscape considerably.

Africa’s response

Africa’s response in limiting the social effects of the Coronavirus so far have been notable – better, in fact, than many had anticipated. Demographics may have helped – 60% of people on the continent are under the age of 65. But the level of coordination between African nations and the proactivity of their governments in implementing the “delay” phase of the virus response was also impressive, and demonstrates the advantages of preparedness and experience in tackling pandemics.

The economic ramifications across the continent have been plain to see, as largescale lockdowns restricted global commerce and triggered widespread economic contractions. Indeed, overall trade volumes between Europe and Africa experienced a slow-down in late Q1 and Q2 this year. Oil-exporting economies in Africa, such as Angola, Algeria and Libya, were then dealt a secondary blow when the price of oil slumped to below zero in mid-April.

While the current economic pressure is certainly attributable to Coronavirus- and oil-related external shocks, Africa’s trading prospects also face some systemic challenges that pre-dated the crisis and may have exacerbated the current situation. With some 41 currencies serving the region, many of which are rarely-traded on the global markets, hard currencies needed for trade can be in short supply at the best of times. Available resources contracted further during the crisis, as pressure was exerted on foreign exchange reserves to support monetary policy and defend currency positions.

The types of goods that African countries chose to import therefore narrowed in scope, with priority being placed on “essential” goods, such as food, energy or medical supplies. In turn, demand for trade instruments, such as letters of credit (LCs), slowed in line with the overall decline in global trade.

Article: BACB CEO Exclusive – Relationship banking remains the key to expanding African trade

Financial institutions change tack

The fast-moving trade conditions have required financial institutions facilitating flows to the region to be nimble. Banks, like many sectors, were quick to initiate contingency plans – by migrating to remote-working arrangements or establishing skeleton or segmented staff set-ups.

Traditionally a paper-based industry, trade finance was challenged to implement a large-scale and rapid overhaul of standard procedure. In some cases, there has been little choice but to turn to digital alternatives in order to keep essential trade flowing (and funding reaching where it is most needed).

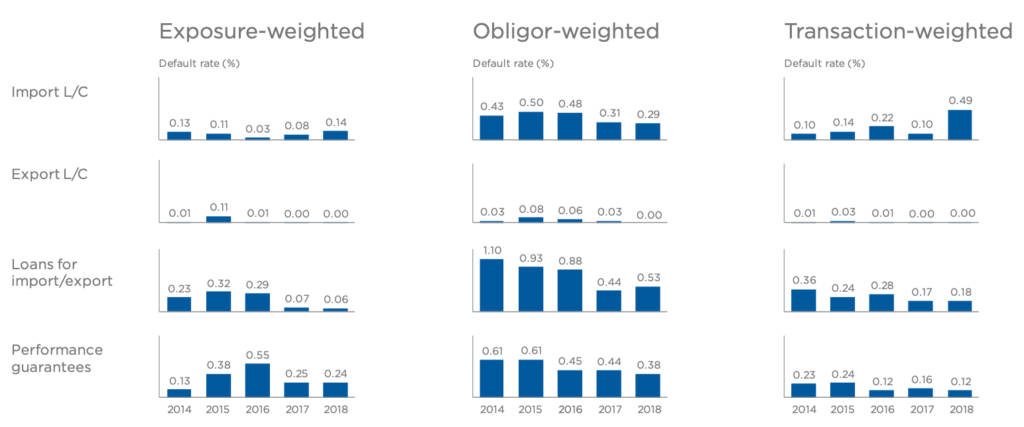

What’s more, the risks, both perceived and actual, of supporting such flows have understandably increased in the new environment. Delays on payments have been a more common occurrence and, in some cases, payment terms have been shortened to 90 days to cope with the uncertain longer-term picture. Growing uncertainty may deter lenders less familiar with, or less committed to, African markets from maintaining credit lines. However, fears around defaults on letters of credit (LCs) remain unsubstantiated – at least in our experience. The risk of default on LCs in African trade transactions was actually already very low. Between 2016 and 2017, for instance, weighted by obligor, default rates declined from 0.59% to 0.05% for export LCs and 0.48% to 0.14% for import LCs. Countries are all too aware that market has a long memory – defaults on payments are generally avoided at all costs even in times of crisis, as they can prove more detrimental in the long-run than the alternative.

ICC Trade Register

A revived partnership

Now only a few months later, the future is looking brighter: oil prices are gradually recovering and African countries have to some extent defied some pessimistic expectations in managing the myriad economic and social assaults that have arisen through the crisis. Commodity trade is still flowing (albeit at far lower levels), and despite all the challenges, African FIs have proved remarkably robust, adjusting well to the changed working environment.

It remains to be seen whether European trade partners will still see Africa as the land of opportunity that they had before. But we remain hopeful that appetite will bounce back. After all, the EU is Africa’s closest and largest trade and investment partner, as well as the main supporter of the African Continental Free Trade Area (AfCFTA), according to official sources. Not to mention that the EU’s “Comprehensive Strategy with Africa” includes plans on how to boost trade, and the future partnership will be a key topic of conversation during the EU-African Union (AU) Summit in October 2020.

The timing of this dialogue is fitting as we begin to move towards the recovery phase of the crisis – and get a clearer sense of how trade routes have been affected.

One possible consequence we may see is largescale reshoring of supply chains to African countries, where possible, as European companies look to diversify their exposures to safeguard business continuity in the future. Of course, commercial incentives will always prevail, but production and manufacturing capabilities are increasing in number and sophistication on the African continent, and may well increasingly provide viable alternatives. Not to mention that reshoring to African providers could also offer reduced transportation costs and less margin for time delays.

Insight: Rejigging Africa’s trade position post COVID19: The AfCFTA option

While the recalibration of global trade may have some welcome consequences, there is no doubt that the impacts of the crisis will linger for some time yet – as they will across all regions. Demand for commodities will likely not recover to usual levels immediately, particularly as much of the disruption has been linked to the futures markets. And soft commodities that rely on production capabilities – as we see in the production of cocoa and cashews – will continue to experience a host of logistical challenges until global lockdown measures are eased and commercial activity returns to normal levels. But Africa’s potential, while perhaps on hold for the time being, is still there.

No matter how the winds change, banks operating in specialist markets, like BACB plc, will remain on hand to provide support, and can help manage risk on both ends of the transaction to ensure that trade continues to flow to and from Africa. In times of crisis, partners with niche expertise truly show their worth in maintaining these vital connections between markets. Specialist banking partners, that bring deep-rooted, expert knowledge of trade in African markets, will be key to restoring confidence within the important, and potentially fruitful, Europe-Africa trade corridor.

Now launched! Summer Edition 2020

Trade Finance Global’s latest edition of Trade Finance Talks is now out!

This summer 2020 edition, entitled ‘Coronavirus & The Fourth Industrial Revolution’, is available for free online, covering the latest in trade, export credit insurance, receivables and supply chain, with special features on fintech and digitisation.