Estimated reading time: 6 minutes

Fire tests gold, adversity tests adaptability.

Trade finance finds itself at a crossroads; a vast and multi-faceted sector, it is an industry that continues to participate in extremely archaic processes.

For many, it can feel as if the ecosystem is in a constant tug-of-war between technological advancement and 19th-century practices.

Some may refute that trade finance, as the oldest domain of international finance, warrants its arcane methods; after all, many industry practices, such as the bill of lading (BL), emerged in the Middle Ages.

But increasingly, large market players are finding that this is not enough of an excuse.

COVID-19 served as a catalyst for many things, but, in part, it served as a wake-up call for the trade finance industry.

It narrowed people’s attention to the inefficiencies associated with shipping procedures, banking relationships, and sustainability measures.

This edition of Trade Finance Talks will explore these topics but also how, in an increasingly digital world, the payments industry has found itself evolving at a rapid pace.

In this new reality, where businesses are now expected to embrace 24/7 real-time payments and market innovations, those that fail to keep up may find themselves paying the price.

Trade finance digitisation: troughs and triumphs

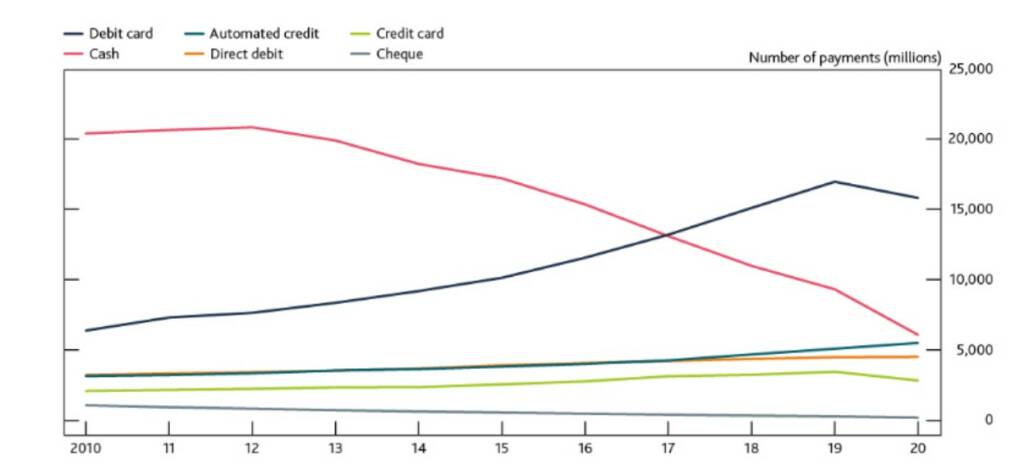

Cash is king, they say.

This may have been true a decade ago, but transactional cash use has fallen from over 50% of payments in 2010 to only 17% of all payments in 2020.

Digitisation has played a large part in increased payments accessibility, and this is not the only capacity in which it has helped progress.

The digital sector represents a wealth of opportunities. In 2019, the tech space contributed approximately £151 billion to the British economy alone.

Despite the world of opportunity, it can often be a long road until large market players, like banks, take any real interest in accommodating the digitisation of processes.

This could stem from varying reasons, but an overarching reality seems to be the lack of high-quality and reliable data on a real-time or near-real-time basis.

Fraud and payments: every action has an equal and opposite reaction

Data. An asset that could potentially solve many barriers to frictionless payments. In the same breath, conversations around data––and, more poignantly, data sharing––can invite a few furrowed eyebrows.

The reality of the situation is that, though interoperability could serve as a real solution for many businesses, it also introduces an increased threat of fraud.

Fraud remains an ever-present looming shadow and, unfortunately, continues to cause long-lasting issues for businesses. It is suggested that fraud tactics such as double financing are costing the industry as a collective up to £5 billion.

Inevitably, it is near-certain that this threat will always be a reality of the landscape, but the question remains: can we find a durable solution for mitigating this risk?

The ICC’s recent paper on fraud reduction shed some light on the situation. The paper included some recommendations on the development of common message formats, data exchange protocols, and standardised data.

Additional notes circled around the need for regulators to take note of the G20 roadmap to enhance cross-border payments.

Pay-ving the way: SMEs reaping the benefits of digitisation

Thanks to trade digitalisation, cross-border payments processes are now faster, more efficient, and less expensive. Not only has this improved transaction accessibility, but it has also bolstered emerging trading markets.

More specifically, it has allowed small- and medium-sized enterprises (SMEs) to better support their businesses.

Mpho Sadiki, head of realtime payments at BankservAfrica said, “If we can shift from a world where an SME waits for payments during the week––getting no real payments over the weekend––to a world where the payment happens instantly…they will be able to have cash flow available immediately.”

eBL adoption: all hands on deck

Since the creation of Model Law on Electronic Transferable Records (MLETR), only six states and seven jurisdictions have adopted its framework as law.

In October 2022, the UK became the next potential name to be added to the list, with the Bill beginning its journey through government.

According to Catherine Lang-Anderson, partner at Allen & Overy, the new law will create more comfort and legal certainty for banks around what they are able to do in a digital sense, further driving efficiency and potentially unlocking risk appetite in other areas.

Lang-Anderson is not alone in this sentiment.

ITFA Chairman Sean Edwards separately said, “The Bill will also break psychological barriers by emboldening market players to consider doing something they would never have before.”

Shipping, supply chains, and sustainability

Over 80% of the volume of international trade and goods are carried by sea.

Freight and forwarding is therefore an integral part of the trade finance eco-system. But shipping and logistics fall into a wider network––one heavily affected by macroeconomic fallout over the last few years: supply chains.

The increased acceptance of eBLs will no doubt aid significantly in many ways, but helping shipping become a more sustainable industry is one of its bigger advantages.

ESG compliance: Hail Mary or greenwashing magnet?

In a field such as trade finance––one almost defined by borders––it is rare for the industry to face a unifying problem such as global warming.

There’s more carbon dioxide in our atmosphere than at any time in human history, and this global crisis will persist if not addressed.

The UN’s 17 Sustainable Development Goals (SDGs) adopted by all member states in 2015 seemingly set the stage for active change in the industry.

Seven years later, the Earth is 0.13 degrees Celsius hotter and no closer to net zero.

Unfortunately, trade finance is a very culpable aggravator in this context. Supply chains, for instance, account for more than 90% of CO2 emissions.

Environmental, social and governance (ESG) was borne out of very relevant concerns about climate change. ESG refers to a set of standards or criteria that measures a company’s actions and how they affect the environment.

Instead of people turning to leading government bodies to solve this larger societal issue, they have, en masse, looked to private companies for answers.

Accordingly, recent polling shows that a large majority of the public believes it is companies who should be responsible for paying for the growing cost of climate mitigation.

Nevertheless, the ESG system has divided the trade finance industry; one side professes its importance, and the other warns against greenwashing.

Pierre Bollon, who serves on the European Economic and Social Committee (EESC) and general representative of AFG, the French Asset Management Association, said, “Companies are being asked by investors to produce more and more information on ESG as this becomes more mainstream, but there is no standardisation of this information.

Data providers are now a key part of the financial chain, and I do not see why this key part isn’t under scrutiny.”

The issue of compliance and how it interweaves with climate-conscious practices continues to unravel in different ways. But one thing appears certain, enforcing standards could be trade finance’s saving grace.