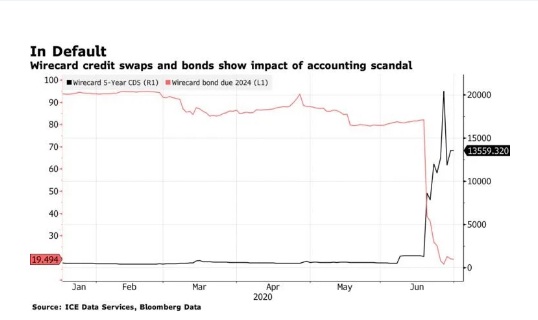

Wirecard AG filed for insolvency on June 25, 2020 due to her inability to pay creditors. Lenders are obviously not willing to increase their exposure to a company that is unable to account for about 1.9 billion euros in cash in a case of high-level accounting irregularities. Audited financial statements especially by reputable accounting firms have long been considered sacrosanct in extending credit lines but even this is proving to be unreliable. The trade finance community surely has some reflection to do.

The Wirecard Scandal

Wirecard AG is a financial technology company based in Germany. Its major operations include electronic payment services, risk management as well as issuance and processing of physical cards. Founded in 1999, the company is listed on German DAX which is the stock index for the 30 biggest companies in Germany. Wirecard operates in 26 locations across the world and until recently, laid claim to being one of the companies at the forefront of financial commerce. I say recently because the company is now embroiled in one of the biggest accounting scandals in recent memory where about 1.9 billion euros could not be accounted for on their balance sheet and the company’s auditors, Ernst & Young refused to sign off their 2019 financials.

Wirecard is suspected of misleading investors through aggressive accounting practices including inflating sales and revenue in order to appear to be performing better than it is actually doing. This misleading information allowed the company to gain the trust of many investors and their share price before the news of the possible accounting irregularities surfaced was over 100 euros. Of course, the share price has since plummeted by more than 90% with investors looking for a way to minimize losses.

Wirecard initially claimed that the missing funds were being held by some Philippine banks but these banks have already denied having any sort of relationship with the company. The company’s auditors, Ernst & Young and the German financial regulator, BaFin, have both come under serious scrutiny. As for Ernst & Young, their inability to detect the accounting irregularities despite being Wirecard’s auditors since 2008 have been called into question as well as their non-disclosure of the unconventional method Wirecard was using to recognize revenues earned from third party agents. BaFin on the other hand has been accused of being lax and ineffective in the conduct of their regulatory oversight over Wirecard while also ignoring calls from whistleblowers to conduct a deeper investigation into the company’s activities long before now.

Investors are always the worst hit when a company gets into trouble and rightfully so since they are also the ones who enjoy the dividends when all is well. It is a case of risk and return. However, investors should not be deceived into making decisions through outright misrepresentation as is the case with Wirecard. Investors typically base their decisions on the strength of a company as evidenced by their audited financials, credit rating and the perceived corporate governance in the company and or anti-money laundering procedure in place in the company’s country. All these boxes seemed to be green before the news of the aggressive revenue recognition technique by Wirecard broke out leaving investors both perplexed and bemused.

Not all that glitters is Gold: A peep into History

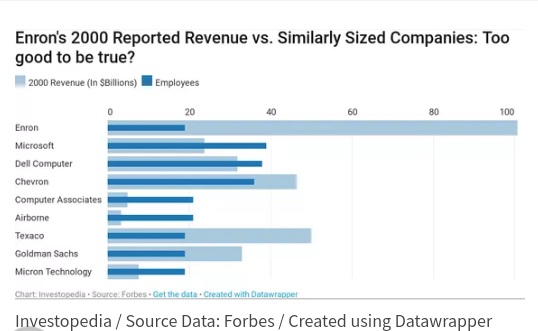

Wirecard’s current travails seem to mirror one that has appeared in many management and financial literature. The classic case of Enron Corporation bears great resemblance to the current scandal. Enron was an American energy trading company that went bankrupt in 2001 after a massive accounting fraud was detected.

Enron used Special Purpose Vehicles (SPV) to mask accounting irregularities for many years. A Special Purpose Vehicle is bankruptcy remote and Investopedia defines it as ‘‘a subsidiary created by a parent company to isolate financial risk. Its legal status as a separate company makes its obligations secure even if the parent company goes bankrupt’’. Enron used the SPVs they created to keep their troubled assets off the books and in the process kept many of their huge losses away from their accounting statement. This misled investors into believing that all was well with the company. Enron’s share price was very high and their revenue was way higher than those of their rival companies at the time but the investing public and financiers did not suspect anything especially as their auditors, Arthur Andersen consistently signed off their accounting statements. Enron eventually filed for bankruptcy in 2001 and admitted to inflating revenues since 1997.

There seems to be a common theme in the cases involving Wirecard and Enron. Both were high-flying companies operating at the peak of their powers when compared to peers and competitors. Both had huge potentials going by the tremendous growth recorded in early years. Of course, both companies were investors’ darling due to their capacity to produce huge returns. Both companies also adopted ‘unconventional’ accounting practices. Also, owing to the expectation of investors on the performance of these companies and forecast of increasing revenue, both felt pressured to sustain the momentum of their growth by whatever means possible even if it means ‘cooking’ the numbers.

If we are to learn anything from history, it should be that observing any of the themes listed above in a company should alert investors to carry out more due diligence if they are to avoid a severe loss that might arise from failing to spot the signals of an accounting irregularity. History advises caution when these signals are spotted and not necessarily that a fraud has taken place or is about to take place.

History also teaches that trade financiers and investors alike should carry out their own extensive financial analysis on audited financials before extending credit lines since even the auditors and regulators seem to be slow in discovering irregularities. It was Arthur Andersen that missed out on the case at Enron and now it is Ernst & Young.

Bigger is not always better

Trade finance in a broad sense refers to all the financial instruments used in facilitating trade. It is estimated that about 80-90% of all trade relies on some form of trade financing. Some trade finance instruments include letters of credit, Factoring, Export credit, Guarantees and Trade credit insurance. Trade finance usually involves offering trade credit to customers based on their perceived creditworthiness and financial strength.

The trade finance market is estimated to be worth close to 10 trillion dollars a year. Despite this, there is still a huge gap in trade financing globally. The Asian Development Bank estimates this gap to be about 1.5 trillion dollars globally which means that many customers’ requests are still being denied. The victims of this denial are usually SMEs who do not have a high reputation and are not even rated by credit agencies.

As part of the requirement for accessing trade finance, customers are usually required to produce their audited financial statements and the forecast of their expected revenue over a period of time. It is also normal to request for the company’s credit report in order to be able to measure and ascertain the debt burden on the company. There is no doubt that companies like Wirecard, with good credit ratings prior to now, will easily pass the test for accessing trade finance. They will even get a huge credit line in the process, thereby denying good companies with sound accounting practices access to funds as financiers’ resources are also finite.

Trade financiers surely need to look beyond the numbers or they will find themselves having unnecessary risk exposure to companies that look good on paper but are bedeviled by sharp accounting practices.

Trade Credit Insurance is of value

Trade credit insurance is a trade finance instrument which provides cover for companies in case counterparties are unable to pay up on their debts or delay payment beyond the agreed settlement date. Trade credit insurers cover majorly commercial and political risks. Commercial risk is the risk that a customer is unable to fulfill her obligations as a result of financial constraints including but not limited to insolvency or bankruptcy. Political risks on the other hand are usually beyond the customer’s control as they could include wars, foreign exchange scarcity or even natural disasters.

Wirecard was surely not considered a company with a serious commercial risk prior to now and Germany also cannot be considered a country with a high political risk but as this experience has shown us, that is exactly why trade credit insurance is important. Due diligence on a company cannot fully reveal the extent of their crisis but buying an insurance cover can surely mitigate the loss that can arise from an unexpected event, be it political or commercial. According to Bloomberg, some hedge funds which bought credit insurance on their debt to Wirecard are already enjoying a windfall as Wirecard has been ruled to have gone through a so-called bankruptcy credit event triggering payments.

Looking Forward

The scandal rocking Wirecard provides us with an opportunity to evaluate and assess the risks involved in international trade. A good accounting report does not necessarily translate to a high level of creditworthiness or financial strength. Third-party assessments, no matter how reliable, are also not sufficient. It is important to look beyond how a company projects itself as this can actually be different from reality as time has revealed of Wirecard. It is also of paramount importance to use the trade finance tools created for such purposes. To be forewarned is to be forearmed.

PODCAST: KYP (Know Your Policy) – Learnings from CPRI in a post-Covid world (S1 E40)

Now launched! Summer Edition 2020

Trade Finance Global’s latest edition of Trade Finance Talks is now out!

This summer 2020 edition, entitled ‘Coronavirus & The Fourth Industrial Revolution’, is available for free online, covering the latest in trade, export credit insurance, receivables and supply chain, with special features on fintech and digitisation.