Post COVID-19, trade credit insurance, can help SMEs scale-up and expand trade by overcoming challenges surrounding supply chain disruption, demand depression and access to credit by complementing governmental support measures.

SMEs: The Big Play in Trade Credit Insurance?

The coronavirus disease (COVID-19) has resulted in significant business interruption losses for Canadian small and medium-sized enterprises (SMEs), who account for 98% of all businesses and 90% of all employees. While the Canadian government has stepped in to offer subsidies, guarantees, loans and tax extensions, SMEs need to explore innovative financing options like trade credit insurance as they plan and prepare for the “new normal”. Trade credit insurance (TCI), is a relatively underutilised product in North America. It not only protects SMEs against the risk of non-payment arising from commercial and political risks, but also fills the financing gap to enable SMEs to narrow down relationships with existing customers and establish new ones, both locally and abroad.

SME Trade Credit Landscape

According to Euler Hermes, 80% of overall Canadian exports are headed to the United States. SMEs need to strongly consider diversifying their export base by exploring opportunities with countries and customers with whom they have no prior track record. In doing so, Canada is likely to gain from the participation of larger domestic firms in the global value chain and being less exposed to market shocks.

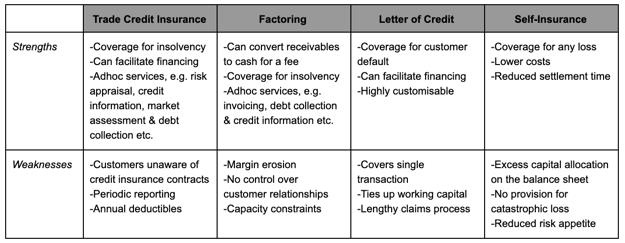

A majority of SMEs engaged in international trade deal on open account terms. They would require greater surety from customers for payment and security as a result of political uncertainty in foreign countries caused by restrictive trade practices due to COVID-19. SMEs generally use self-insurance, factoring, and letters of credit to mitigate risks in trade transactions. Table 1 illustrates how TCI offers a convenient alternative as a risk financing tool.

Responding to the COVID-19 Challenge

As SMEs move from shutdown to recovery, they will continue to face headwinds due to supply chain disruptions, depressed demand and access to liquidity, as a result of insufficient cash flows and working capital funding. These developments pose a significant concern since any economic recovery plan will rely on SMEs to progress seamlessly from a base of reliable financing planning to firm up orders/ purchasing materials to receiving orders/ becoming fully operational.

TCI delivers cover for business to business transactions, by acting as a hedge against non-payment of goods, invoices and other debts. It also assists SMEs in their international activities, where they have less expertise, bargaining power and financing capabilities.

The government needs to recognise the importance of TCI offered by private insurers as an effective instrument for complementing economic relief measures aimed at preserving buyers’ ability to pay once trading resumes. After determining the extent to which TCI is vital to trade and the economy, it needs to incentivise private insurers to design affordable tailor-made products for SMEs who can benefit from financial protection. Another option is to establish reinsurance schemes through a public-private partnership to enable the optimal sharing of risk between the government and private insurers. By doing so, SMEs, who typically carry lower cash reserves and have a lesser ability to absorb debtor defaults, can obtain the appropriate insurance coverage to meet their needs.

VIDEO: Development Finance – The Role of Export Credit Agencies, Trade Credit Insurers and Development Banks

Such initiatives also act as a catalyst for SMEs looking to fill in domestic demand shortfalls and expand reach outside Canada. With “covidisation” likely to push SMEs in search of alternate revenue streams towards unfamiliar customers and markets, TCI can provide a distinct advantage by selling off credit, as opposed to selling goods against cash or advance payment.

Benefits of Trade Credit Insurance to SMEs

On average, with accounts receivable representing more than 40% of a company’s assets and one in ten invoices becoming delinquent, TCI offers SMEs:

Protection from non-payment by minimising losses arising due to commercial risks- protracted defaults, delayed payments, insolvencies, bankruptcies, liquidation and winding-up. TCI can be used to reduce or eliminate bad debt reserves, secure acquisitions and hedge against idiosyncratic export risks without tying up the day-to-day capital of SMEs. Additionally, credit insurance premiums are tax-deductible, unlike bad debt reserves.

To boot, TCI often covers SMEs from political risks such as regulation changes, import-export license restrictions, expropriation, confiscation, war, riot, civil war and transfer delay.

Growing profits with increased credit limits by insuring receivables can help SMEs add credit to existing customers or implement higher credit limits beyond the insured’s “credit comfort zone”. By creating more revenue opportunities, SMEs can take on more orders from existing customers and pursue new and larger customers abroad.

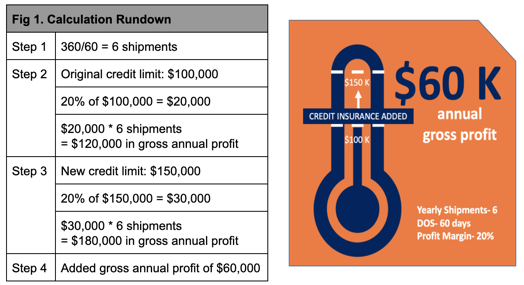

Figure 1 depicts an SME which decides to add TCI to increase its credit line limit from USD 100,000 to USD 150,000. With a 20% profit margin and 60 days of sales (DOS) outstanding, the SME can garner an added annual gross profit of USD 60,000.

Better borrowing terms and market information by insuring receivables can also provide SMEs access to more capital and negotiate a better cost of funds. Besides, SMEs can use the insurer’s knowledge and technology to reduce any information barriers to make risk-based decisions by carrying out credit evaluation of customers, prospects, industries and countries.

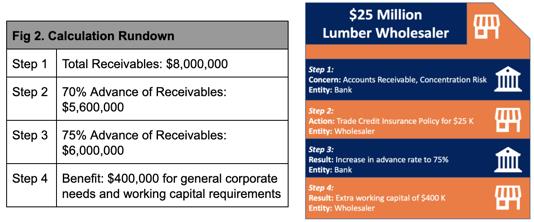

Figure 2 shows an SME that operates in the pulp and paper industry with an annual turnover of USD 25 million and accounts receivable of USD 8 million between eight clients. The SME has three clients that carry a high concentration risk of USD 6 million. In this case, the bank secures its lending relationship with the purchase of TCI, which provides comfort from the SME’s standpoint for meeting certain credit management thresholds of the lender. In return, with a USD 25,000 policy, the SME gets a higher advance rate of 75% for the benefit of USD 400,000 to fund general corporate needs and working capital requirements.

Accessing Trade Credit Insurance

TCI presents a massive opportunity for SMEs with average premiums around USD 35,000 covering up to USD 40 million of receivables. The uptake of TCI will further rise with increased competition and digitisation, which in turn will offer SMEs the flexibility to choose between insuring a single invoice or their whole turnover.

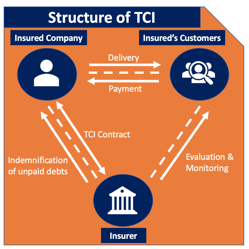

An SME can approach an insurer by providing relevant information regarding its business and customers. Upon evaluation of the risk profile of the SME’s customers, sector of trade and previous bad debts, the insurer will then set credit limits with invoicing periods. In some instances, insurers may assign a discretionary credit limit for multiple buyers to grant flexibility in trading. Once the policy terms and premium are drawn up by the insurer, the SME may negotiate parts of the quote e.g. coverage amount, level of co-insurance, deductible and minimum amount for the claim etc. Throughout the policy period, the insurer is responsible for monitoring the SME’s customers and adjusting the coverage amounts, if and when required. As the SME expands, it can also work with the insurer to add new customers under the policy. If an SME’s customer named under the insurance policy becomes insolvent or financially incapable of paying, it can file a claim with the insurer for indemnification.

Conclusion

TCI represents a USD 11 billion global market. North America’s share is approximately USD 1.5 billion, with only 3% of suitable businesses buying trade credit insurance, compared to Western Europe, which has a 15% penetration rate. The lower penetration is due to a lack of product awareness resulting in the majority opting for self-insurance. There are limited distribution channels with very few brokers on the ground due to “crowding out” by government export credit agencies. Added to that is the complexity of the product whose dynamic nature requires active monitoring and can prove challenging to SMEs without adequate time and resources.

ICC SOS – Save Lives. Save Livelihoods. Save Our SMEs (S1 E43)

TCI is integral to the business growth strategy of SMEs. By ensuring capital protection, cash flow conservation, better loan servicing and repayments, and secured earnings from events of default, TCI can help boost the growth of SMEs and work to indemnify losses. Besides, mitigating the financial risk, it also complements the credit management process by allowing SMEs to leverage their accounts receivable. A higher adoption rate of TCI would also make premium rates competitive.

Going forward, as the Canadian government maximises spillovers from new treaties and trade negotiations, it will be interesting to witness how it promotes export opportunities for Canadian companies by balancing its mandate for export credit agencies and private credit insurers.

This article was written by a member of TFG’s 2020 International Trade Professionals Programme. Find out more here.

Disclaimer: The views that have been expressed on this page are that of the author, which may or may not be in line with their company, Trade Finance Global or London Institute of Banking and Finance’s view.

Type a message