London, 25 March 2026: OakNorth, the digital bank for entrepreneurs, by entrepreneurs, has completed a $25 million loan-on-loan facility to Trade Finance Partners (TFP), marking its first transaction in the… read more →

The OPEC Fund for International Development has extended a $30 million loan to Ipak Yuli Bank, marking its first direct financing to a privately owned bank in Uzbekistan, the organisation… read more →

The U.S. Consumer Financial Protection Bureau (CFPB) will enforce certain credit card consumer protection rules on buy now, pay later (BNPL).

The Asian Development Bank (ADB) and the African Development Bank have today formalised a $1 billion sovereign exposure exchange deal with the objective of augmenting their capital adequacy levels and… read more →

A £26.3 million equivalent loan backed by the UK Government has allowed the Ukrainian government to start rebuilding six bridges and reopen vital supply routes near Kyiv. The loan has… read more →

Looking to further international trade, Tim Reid, CEO of UK Export Finance (UKEF) met with Albanian Prime Minister Edi Rama, and Finance Minister Deline Ibrahimaj to finalise a £4 billion… read more →

Surecomp® today announced that PT. Bank BTPN Tbk (BTPN), one of the leading privately-owned banks in Indonesia and part of the SMBC Group, is live with its DOKA™ solution to… read more →

ING announced today that it has spun out Loan Optics to vc trade GmbH, the leading digital platform in the market for private placement and promissory note loans. Loan Optics… read more →

UK Export Finance (UKEF) announced on Finance Day at COP27, November 8, that it will become the first export credit agency (ECA) to offer Climate Resilient Debt Clauses (CRDC) in… read more →

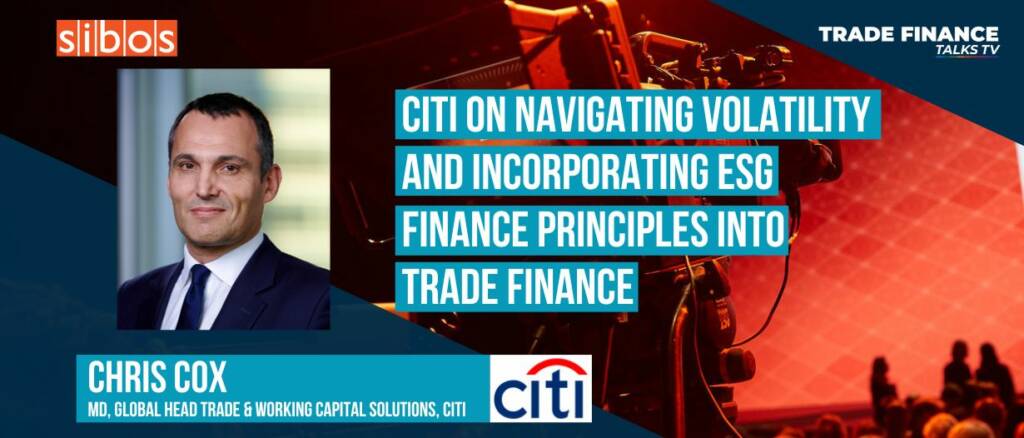

Citi has been working collaboratively with its institutional clients to incorporate more sustainability-based principles into their everyday operations; a movement taking place as the world increasingly moves towards a more sustainable, low-carbon economy.