Estimated reading time: 8 minutes

Digitisation was a good business practice within global supply chains long before the COVID-19 pandemic, but it really became a must over the last two years.

It moved from being one of several options for upgrading operations, to an absolute necessity to continue being in business.

Everything from product design to sampling, factory audits, production tracking, product inspection, pick and pack, and factory visits has become virtual or automated to the greatest extent possible.

At LFX, our digital product design business has continued to gain traction, as brands and retailers see that it is not only faster, but also more sustainable to go digital in the product design phase.

As for manufacturing, some say that the future factory may one day follow today’s “dark” warehouses, where lights can be off for most of the time, as robots perform manual tasks and digital sensors collect data and send it to the cloud to be analysed and actioned.

So what is stopping supply chains from moving decisively in this direction?

We have found that finance is a major barrier: factories and firms need substantial amounts of investment capital and trade finance in order to acquire technology, train up their staff, reorient their business processes, and support the increasing demand for working capital within the supply chain.

And while there will be a solid return on the investment, companies need the seed capital to get started.

Where will this come from?

Capital pain points in emerging markets

The supply chains that run across the world’s emerging markets – including key Asian production countries such as China, Vietnam, India, and Bangladesh – are dominated by small and medium-sized enterprises (SMEs) with thin capital bases and even thinner margins.

They are growth- and finance-constrained, and are mostly located in markets where the finance sector is not as developed as in the OECD economies.

As a result, they lack access to different forms of trade finance that would enable them to reach new customers, open up new markets, and grow their enterprises.

Indeed, in November last year, the International Chamber of Commerce (ICC), McKinsey & Co, and Fung Business Intelligence published a joint research paper based on interviews with over 60 export-oriented SMEs.

In their findings, they summarised the four key barriers to growth for SMEs as follows:

- Lack of liquidity – Driven by their own lack of access to steady funding, and buyers’ rising requirements which were exacerbated by the pandemic

- Complexity in accessing finance – Due to its reliance on paper-based procedures and lack of scale in processing

- Lack of growth opportunities locally and internationally – Due to a lack of resources for proper business development

- And a lack of institutional capacity – Particularly around digitisation, and a lack of such capacity even within their local finance providers or regulators

The pandemic exacerbated this situation, and anecdotal reports indicate that up to 10% of some regions’ factories have gone out of business due to financial hardship, despite strong export trading records.

It is no coincidence, then, that the global trade finance gap rose from $1.5 trillion to $1.7 trillion from 2018 to 2020, with SMEs accounting for over 40% of rejected applications, according to the Asian Development Bank (ADB).

The trade finance gap, persistent even in a strong economy, could imperil Asia’s recovery from the pandemic.

Indeed, the ICC has estimates that up to $5 trillion of trade finance may be needed globally for the gap to return to its 2019 level.

But even so, SMEs will remain last in line, both in terms of finance and access to technology, unless systemic changes are made.

The digital trade finance proposition

We believe that digitising trade finance could be a key part of the solution.

Indeed, a number of digital trade finance networks already exist, connecting supply chain partners and financiers through pooled data that are secured by blockchain to deliver speed, transparency, and security.

In China, for example, some digital trade finance networks already connect tens of thousands of enterprises.

The creation of digital trade finance networks is a good start. They expedite the flow of funds and achieve much higher levels of efficiency than paper-based trade finance processes.

This can allay the concerns of financial institutions, who find SME loan sizes too small given the intense paperwork involved.

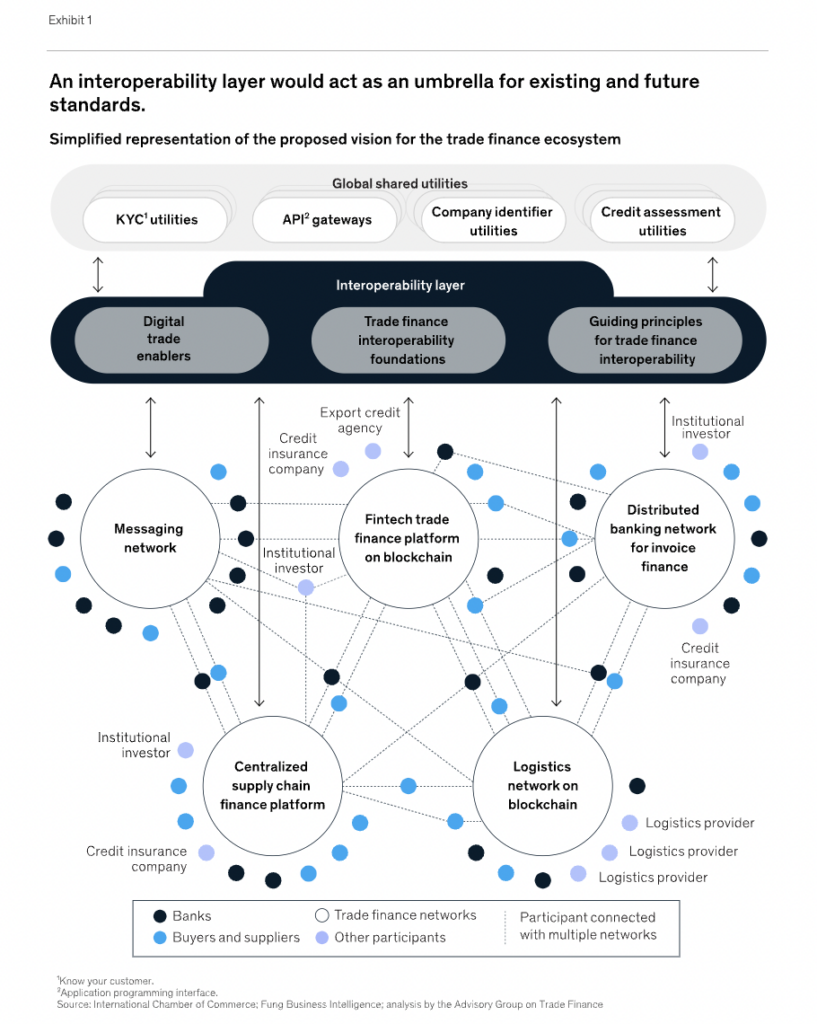

However, from a supply chain perspective, digital networks may add complexity unless they are interoperable.

As banks and financial providers establish digital trade finance networks – each with their own protocols, standards, data flows, and compliance requirements – a single factory could now be confronted with the need to satisfy multiple different standards and protocols, particularly as their trade finance might be linked to different buyers.

What was supposed to ease an administrative burden has now just multiplied it.

At the same time, data pools that could drive efficiency, transparency, and agility are left incomplete, as a single company’s data might sit across multiple networks, none of which talk to each other. Hence the term “data islands.”

The apparel industry faced this problem years ago with multiple audit standards for social and environmental compliance.

As an industry, we worked together to create common standards and drive interoperability – which we called equivalency.

A single audit became usable across multiple buyer and sourcing networks, thereby reducing duplication and administrative burden, without sacrificing standards.

Today we see an opportunity for the trade finance ecosystem to address long-standing challenges of access and efficiency, by building its future around interoperability as a core operating principle.

This is the vision recently put forth by ICC, McKinsey and the Fung Business Intelligence in Reconceiving the Global Trade Finance Ecosystem, which drew on consultations with over 100 experts and practitioners in trade, finance, and technology.

The report recognised that the progress made by digital trade finance networks could be amplified by scaling best practices across the entire ecosystem, while pooling data to improve risk management, access, and service delivery.

Importantly, data pooling would further improve SME access to finance, by enabling providers to make decisions based on a much wider data set.

Indeed, this has been shown already by the Hong Kong Monetary Authority’s (HKMA) Commercial Data Interchange in its pilot stages.

At LFX, our fintech supply chain finance venture, Air8, aims to leverage our domain supply chain knowledge and data-driven insights to connect our ecosystem stakeholders to make capital more widely available to SME factories.

An interoperable trade finance ecosystem would complement key initiatives to digitise cross-border trade, which are also built around interoperability.

The United Nations Economics and Social Commission for Asia and the Pacific (UNESCAP) has developed a Framework Agreement on Paperless Trade, and the United Nations Commission on International Trade Law (UNCITRAL) has also developed a Model Law on Electronic Transferable Records (MLETR) that gives legal status to digital trade documents.

Although only a handful of countries have ratified these, they will eventually attract greater acceptance because the benefits are so clear. These initiatives are all part of the supply chain of the future.

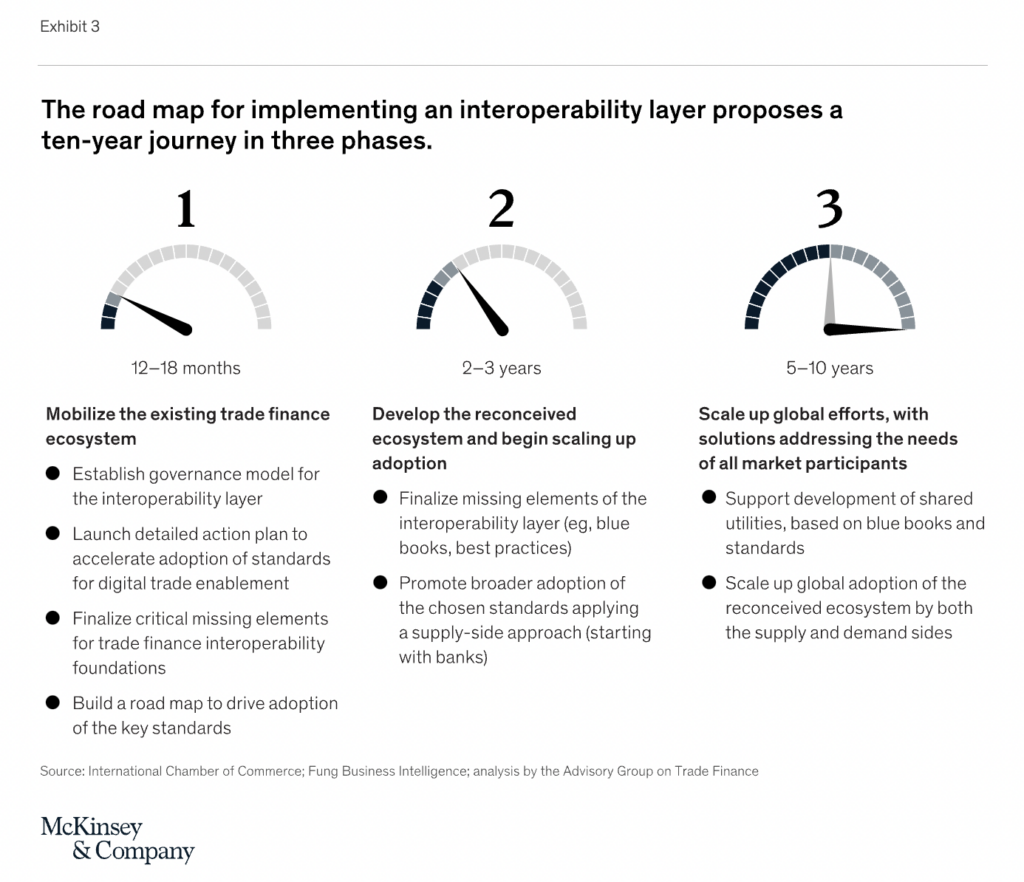

Delivering interoperability at speed

Expanding access to trade finance is not only a key to achieving the digital supply chain, but is critical to ensure the growth of SMEs, which are the backbone of job creation and stability in emerging markets.

In Southeast Asia, for example, SMEs comprise 97% of all enterprises, 69% of the total workforce, and 41% of GDP, according to the ADB.

In other words, solving the SME finance gap is not just a business opportunity, but could also be a critical contributor to addressing issues such as income inequality and poverty.

For years, supply chains have been mainly preoccupied with flows of products. Data and funds were transacted mainly to support the product flows.

Today, technology gives us the opportunity to marry flows of products, knowledge, and capital into a holistic supply chain – indeed, competing in the digital economy demands nothing short of this.

We should recognise that interoperability could not only drive growth and expand markets, but could also have important sustainability implications, by making capital available to those who need it most.

With all of our efforts, we hope that the day we see interoperability among trade finance networks will come much sooner than we expect.

*Ed Lam is the CEO of LFX; Pamela Mar is the Executive Vice President for Knowledge and Applications at the Fung Group. Both Ed and Pamela are based in Hong Kong.

Pamela was a key player on the team that put together Reconceiving the Global Trade Finance Ecosystem, jointly published by McKinsey & Company, the International Chamber of Commerce (ICC) and Fung Business Intelligence.

Read our latest issue of Trade Finance Talks, Spring 2022