A pleasant evening’s read about commodities supercycles generates as many variations on common themes as Shakespeare’s sonnet count.

History illuminates paradigm-shifting innovation, such as the rise of information technology at the turn of the millennium.

It shows systemically important and protracted fiscal spending, focused on timely and noble goals – think Net Zero 2050 – that extend into the private sector.

Sometimes, economic shocks precede them, as in the global financial criss of 2007-08. Always, they are layered with price-supporting, ever-present factors.

They are intertwined with recurring patterns and quiet boosters. Within a supercycle, commodity price drivers range from short-term momentum providers to cyclical and long-term shape shifters.

In a genuine supercycle, these commingled partners dance on a higher plane: prices trend with a higher set point.

The Bloomberg Commodity Index value on February 2, 2022 shows a 35% increase YOY (up 46% since January 2016, suggesting a different origin).

The over 80% rise since April 2020 launched the newest round of supercycle chatter.

Thousands of articles have recently appeared as market watchers debate whether these dynamics are exclusively cyclical, structural, or temporary.

Frankly, there are elements that would suggest each is in play to some extent. The final supercycle call depends on the magnitude, duration, and ramp speed of interacting and sometimes opposing forces.

COVID-19 is one such force – it disrupted many economies, businesses and supply chains. The economic recovery from COVID-19 may be an ephemeral revival or a bridge to the next inflation-augmented supercycle.

Given the unique demands arising from climate change abatement, price destiny for some commodities could fragment for the first time in long-term history, and some prices may substantially outpace others.

Whether price increases will sustain for two years or 30, it still matters. It will shift the development trajectory of all countries, especially emerging markets and developing economies (EMDEs) that deeply rely on commodities for income, growth, and life itself.

The view from emerging markets

Commodity futures prices form the basis for contracts that move goods across EMDE borders.

As commodity prices rise, emerging market commodity exporters have opportunities to leverage increased export dollars for sustainable, inclusive growth and increased financial stability.

Many commodities have experienced exponential price increases YOY, with many near or above their highest level in at least a decade.

For example, agricultural products (coffee, soybeans, wheat) and metals (copper, lithium) may provide new advantages to several exporting EMDEs (from Romania to Madagascar, Zambia, Brazil, Vietnam, Mongolia, and beyond).

However, all is not rosy. Many EMDEs rely on imports for the energy that powers their most basic economic function, and those prices are also increasing (e.g. the more energy-efficient liquified petroleum gas (LPG)).

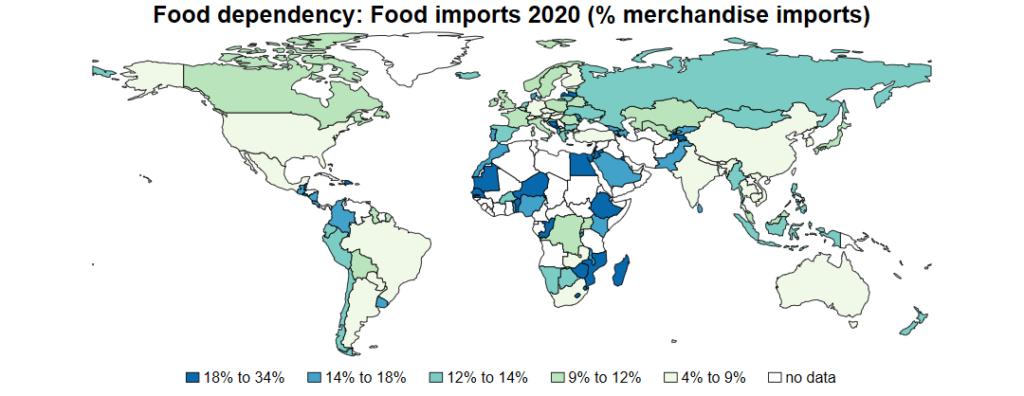

Focusing on agricultural commodities, many EMDEs – often the smaller and poorer ones – are dependent on imports to maintain access to food, as shown in the figure below.

In 2020, there were 29 EMDEs for which food imports represented at least 20% of merchandise imports.

Cereals make up more than 10% of total imports for 12 International Development Association (IDA) countries.

Ten of the top 20 broken rice importers are Sub-Saharan African countries. Food supplies need to be continuously replenished; imports need to keep coming across borders.

Most importing EMDEs are price takers: demand spikes in systemically large countries affect smaller countries directly.

Tightening US monetary policy will further increase USD-based import contracts. Whether a supercycle is launching or not, rising commodity prices cost these countries more to import the same volume of actual goods.

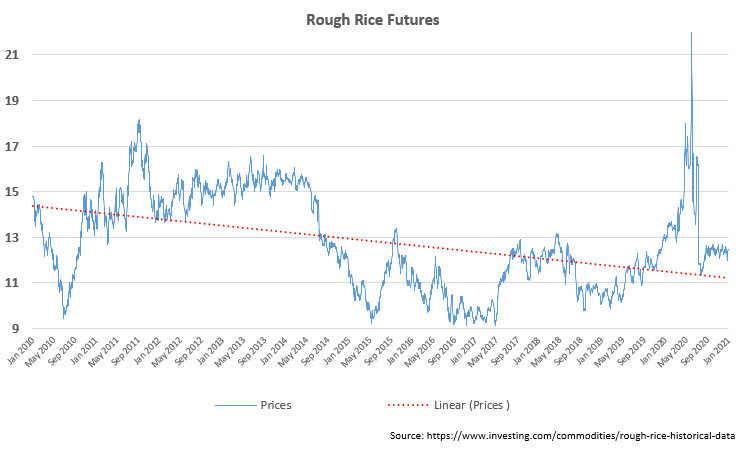

For example, the charts below show rough rice futures prices increasing by nearly 70% between April 2017 and February 2, 2022, incorporating a few peaks and troughs along the way.

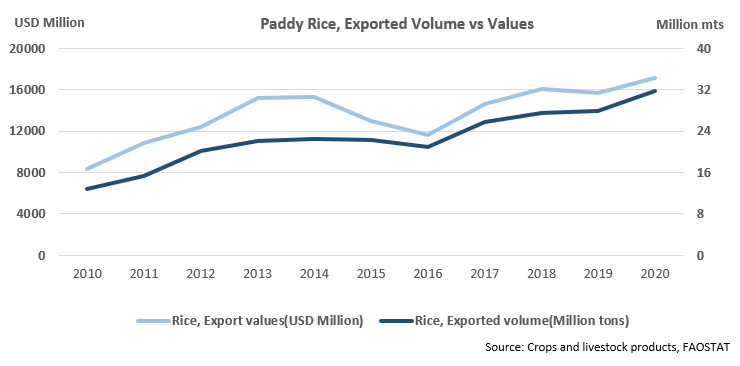

Since 2016, global rough (“paddy”) rice exports/imports (metric tonnes and USD) have increased by approximately half.

Rice importers are paying more to bring much-needed rice inside their borders, as both prices and demand rises.

Rising prices exacerbate potential food scarcity, which, in turn, leads to severe price spikes locally.

Around 768 million people globally faced hunger in 2020, with most food insecure people in low-income countries.

Trade finance can help

As import costs rise, more trade finance is needed, since goods do not cross EMDE borders without it.

In most EMDEs, the trade finance gap is economically significant, notoriously persistent, and growing.

Prior to COVID-19, the supply of cross-border trade finance was already under pressure.

Sharp increases in actual, potential, or perceived financial risk makes commodity trade finance vulnerable, given its short tenors, self-liquidating structure, and dependence on cross-border correspondent banking relationships (CBRs).

As COVID-19 emerged, many correspondent banks, facing greater risk, slowed their financing of trade.

By early 2020, emerging market banks across the world noted that trade finance demand was increasing, while their capacity to meet that demand was falling.

Since then, the frequency of banks indicating CBR stress has more than doubled, reaching 81% (vs. single digits in the prior decade).

Thus, as commodity trade finance needs rise, the supply is falling.

As Pierre Ligneul de Villeneuve, head of commodity trade and structured finance at the International Finance Corporation (IFC), has said: “More commodity finance clients and banks are reaching out to DFIs like IFC, because some banks withdrew their financing lines, and the remaining facilities are almost full.

“It is rare to see such pressure in all three subsectors (energy, metals, and agriculture) at the same time. IFC is playing an increasing role to support trade in emerging markets.”

Multilaterals have supported trade finance during COVID-19. Since March 2020, IFC alone has supported well over $10 billion in trade for EMDEs, $2 billion of which through commodity finance.

But there is more to do.

As Nathalie Louat, director of trade and supply chain finance at IFC, has said: “Even when commodity prices were lower, there was a relative scarcity of trade finance.

“And this scarcity deeply impacts the poorer, smaller markets that most heavily rely on commodity imports, so the need for trade finance in EMDEs will continue to increase.”

Read our latest issue of Trade Finance Talks, Spring 2022