How do we move out of ‘CSR’ and into ‘P&L’? Following the Davos 2020 World Economic Forum, TFG heard from Beata Javorcik at University of Oxford, discussing corporates addressing climate change

The Davos 2020 World Economic Forum and the year preceding it may give the impression of a global corporate sector fully aware of, and internalising, its corporate social responsibilities (CSRs). This is particularly apparent when it comes to the role of private firms in addressing perhaps the biggest challenge facing the world: climate change. Rather than treating CSR as a branch of corporate PR, many companies are now making clear steps in incorporating climate change considerations into their core operational and financial thinking. The phrase: “moving out of CSR and into P&L” captures well the trend.

At the Davos 2020 Forum in January many of the world’s largest companies signed up to the most comprehensive effort yet to account for businesses’ social and environmental impact. This was a new framework, launched at the Forum, which will enable them to report their corporate metrics on subjects such as employment standards and the environment in line with the UN’s Sustainable Development Goals. These metrics, created by the WEF’s International Business Council, are intended to be deployed in corporate accounts from the start of 2021.

No doubt, such international initiatives can boost the private sector efforts to fight the climate change. Their effectiveness will be limited, however, if firms from emerging markets, which are ever-growing climate change contributors, do not sign up. Research in EBRD recipient countries on green governance point to existing problems and potential solutions in this respect.

The latest EBRD Transition Report finds that greenhouse gas emissions in the EBRD regions have fallen substantially since the 1990s, but if the regions’ economies are to fulfill their commitments under the Paris Agreement, those improvements will need to continue. This, in turn, will require further improvements to the green credentials of the regions’ firms. While some firms in the EBRD regions have excellent green management practices, most continue to perform poorly in this regard. Firms with weaker green management practices may be aware of the importance of monitoring their impact on the environment, but lack the organisational structures necessary to set and achieve targets in this area.

Video: TFG interviews EBRD on the latest EBRD Transition Report

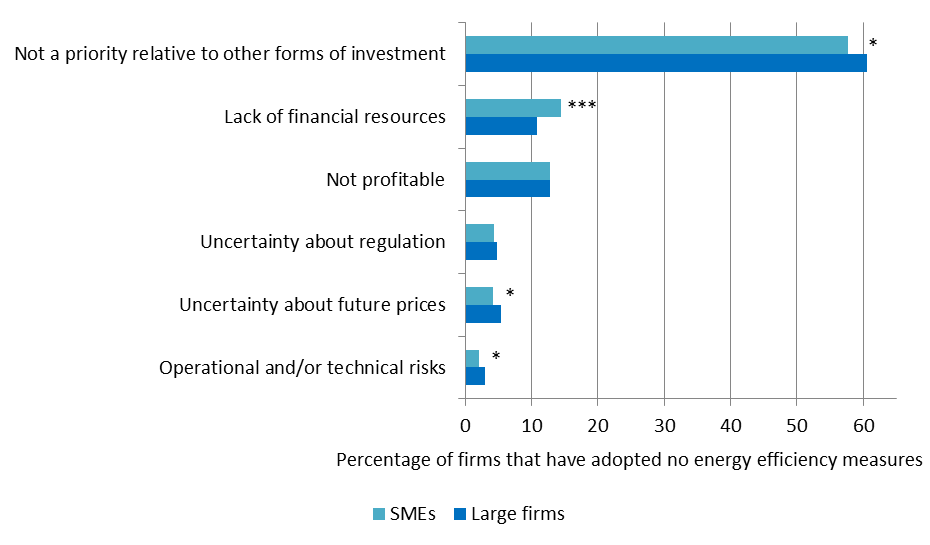

Despite the potential environmental and efficiency benefits of investment aimed at reducing firms’ impact on the environment, there are many firms that refrain from implementing such measures. According to enterprise surveys, more than 60 per cent of respondent firms that have not implemented energy efficiency measures report that this is not a priority relative to other types of investment (see Chart 1). This dwarfs the second and third most cited reasons, which are the lack of financial resources (14 per cent) and the unprofitability of such investment (13 per cent). Interestingly, there is relatively little difference between firms of different sizes.

Chart 1. Reasons for not investing in energy efficiency measures

Source: EBRD Enterprise Surveys and calculations.

Note: * and *** denote statistical significance at the 10 and 1 per cent levels respectively. SMEs have fewer than 100 employees; large firms have 100 or more.

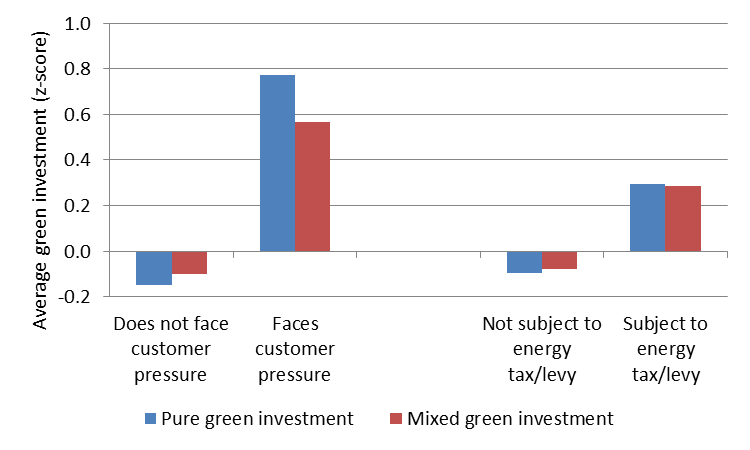

If firms refrain from undertaking pure green investment for the simple reason that managers face more pressing matters in the short term, they may need a nudge to prioritise green investment, particularly if green investment have a positive, but small, net present value. Enterprise surveys suggest that customer pressure and regulations can play such a role. As illustrated in Chart 2, firms are much more likely to undertake investments aimed at improving energy management, generation of green energy and control of air pollution in response to customer expectations and when subject to energy taxes.

Chart 2. Customer pressure and energy taxes/levies both boost green investment

Source: EBRD Enterprise Surveys and calculations.

In conclusion, credit constraints hamper all investment by firms, including investment with environmental benefits. However, when it comes to pure green investment, access to finance is not the main constraint in emerging markets. Thus improving the availability of credit is just one element of the broad policy mix that is necessary to stimulate green investment and improve firms’ green management practices. Governments may also have to compel firms to produce in a more energy efficient manner using environmental standards or other regulations or via subsidies that are contingent on the use of specific green technologies. Targeted green credit lines can also encourage firms to prioritise green investment. However, an important precondition for the success of such interventions is effective enforcement of regulations in a corruption-free environment. Lastly, firms are also known to improve their green credentials in response to pressure from their customers. With this in mind, voluntary environmental standards may help leverage the power of peer pressure and consumer awareness in order to further reduce firms’ environmental footprints.

Now launched! Spring Edition 2020

Trade Finance Global’s latest edition of Trade Finance Talks is now out, taking a deep dive into trade finance in emerging and developing markets.