“There is one issue that will define the contours of this century more dramatically than any other, and that is the urgent threat of a changing climate” – Barack Obama, 2015. TFG’s Ross McKenzie investigates the Economics of Climate Change.

In 2015 as President of the United States, Barack Obama highlighted climate change as the single most urgent threat to humanity, and the economic consequences of such a threat are potentially unlimited.

Three years later in 2018, global energy consumption increased at just below double the average growth rate since 2010. This did result in an increase in solar and wind power, however, all fuel related consumption increased alongside which resulted in a new CO2 emissions increase record of 1.7%.

The growth in demand for electricity was behind much of the energy surge, largely brought on by a growing global requirement for heating and cooling equipment as global temperatures fluctuate more.

In general, the main economic effects of climate change are going to be presented through damage to economic growth in the way of property damage, lost productivity, security threats and extreme weather conditions.

As temperatures and global sea levels rise, how will the global economy adjust to such a different landscape?

Categories

Economically, the simplest way to even begin to consider the ramifications is to split them into categories. First, we have the immediate category. This group is composed of events such as natural disasters which directly and immediately have an impact on economic performance.

Immediate

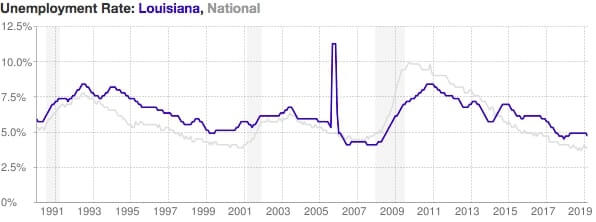

An example of this would be the US’ most destructive natural disaster in history – Hurricane Katrina and it’s economic effect upon New Orleans and Louisiana. Devastatingly, 1,200 people lost their lives as a result of the hurricane.

According to a 2011 report by the National Hurricane Center Katrina caused an estimated $125 billion worth of damage in total. This is a staggering figure for a storm that appeared pretty much unannounced.

But it is not just the horrific loss of houses or business property, the physical and emotional loss members of the workforce can (rightfully so) cause long delays in production etc. So in the short-term, you have over $100 billion worth of damage, and more than a thousand lives lost. However for Katrina survivor-victims, over the long-run they actually recovered well, and some say ended up in an economically better place than if the storm had not hit.

Why? Catastrophe brings about change. Change on a scale that may have never been justified until the disaster, but definitely benefited the economic climate of Louisiana. For example, due to the sheer extent of the damage caused, unemployment – after it’s significantly high initial rise – actually began to fall quite dramatically with construction contracts being put in place to repair the damage. There began many projects that demanded a larger labour force, and those that lost their jobs (or offices) to the storm and floods found work well.

This does not however advocate or in anyway say that Hurricane Katrina was a good thing. It does however highlight the resilience of mankind and their true adaptability.

Natural disasters such as hurricane Katrina can have devastating effects on an economic eco-system. In today’s dynamic and globalised world, if a country which specialises in coffee and 75% of their produce is focused on the making and exporting of coffee, is then hit with record-setting landslides and temperatures which reduce their crops by 30%, what are they supposed to do?

Furthermore, what happens to the global market which demands the coffee this country produces? The result is a shift in global demand consumption patterns, which will reallocate capital, causing mass closures of some industries and mass booms in others.

Take the coffee analogy, for example, in March of 2019 Brazil exported 2,698 60kg bags of Coffee. If you consider each step of the production cycle for coffee, you will see many other industries tie in and may rely heavily on Brazil’s substantial demand for coffee.

When this demand is no longer possible to meet because of climate change-related issues, then the $5.1 billion that was spent on Brazilian coffee in 2018 will be spent in other areas.

Mediocre

After looking at the direct and immediate effects of climate change, we begin to see the larger and more daunting picture. For it is not the immediate threat of climate change that humbles humanity, it is the long-term.

Sea levels and polar ice caps have been the topic of much debate as of late, and for good reason. If you first of all think about the types of dense economic areas that reside next to the world’s oceans you may begin to stumble upon the magnification of this not-so long-term threat.

In the US alone it was found by Dr Rachel Cleetus that within the next 30 years, more than 300,000 US coastal homes worth well over $100 billion would be subject to flooding. They house just over half a million people and contribute £1.5 billion to the property tax base. She poised that, by the end of the century, 2.5 million homes and $1.5 trillion of property is at risk.

New York, London, Hong Kong, Mumbai and Tokyo accumulate well over 40 million people, and are some of the world’s busiest hubs for business, financial services and general human activity. In a move that would have confused our earlier homo sapiens ancestors, we have decided to heavily populate the coasts. This is not something that is hard wired into our instinctive DNA, however it has proved ridiculously desired as coastal house prices soar all around the world.

And that is just one area that will be economically affected – house prices. It is unclear whether house prices will react in a sharp decreasing way once flooding begins to happen, or whether it will take time to ripple through the world’s property markets. But this is the issue – a severe lack of knowledge for people who reside or otherwise invest in those homes will result in the loss of probably their biggest asset, which for them individually will be flattening.

However, when overall house prices generally begin to fall, then we see the real economic dent world-wide. To give you some indication of just how much money is tied up in property on a global scale, in 2017 mankind hit a new record high for the level of investment in property – at £1.62 trillion.

When $1.62 trillion worth of investment faces flooding and just as much in damages, prices will dwindle and there could be a mass increase in the uncertainty surrounding property prices. It may not be the case of Katrina, where in the long run victims were potentially economically better off, as this could result in a deeper recession than we’ve ever seen.

With property prices continually rising over the past 50 years, the amount of investment it has attracted is astonishing. Much of the world’s business investment is done off the back of property investment. Donald Trump and his property empire is a good example of how property investment can redistribute itself into other commercial areas.

£1.62 trillion should rightfully illustrate the severe lack of understanding of the seriousness of this matter. But that figure is directly tied to the global property markets, what one should consider is one city in the world and one alone – this will give us chance to explore more avenues of loss, on a smaller, more comprehendible scale:

New York. With 7.4 million people in the city, and a further 18 million in the metropolitan area is a good example of the extent of mediocre category economic effects of climate change. Rising sea levels for example – NY has experienced at least a foot worth of sea level rise since the beginning of the 20th century, and is set to receive a further 50 inches by the 22nd century. This is literally a rise of just over 4ft – a foot less than the global average height for women.

I would then urge one to broaden their mind onto the city’s global role. The city of New York is the 3rd largest economy in the US behind California and Texas and has a GDP of roughly $1.6 trillion. When such a large, densely populated, economically vital area is ravaged with a rising sea level, rising temperatures and extreme weather conditions then there becomes a significant amount of costs required to rebuild and assist the millions of people effected, and also investments and economic activity that will be forever lost in the city.

When one mentions economic activity, it is important to note the US’ position in the global economy. In 2018, the US exported $2.5 billion worth of goods and had the demand to import $2.4 billion. This, among other statistics such as their GDP (estimated at $21.1 trillion for 2019) place them number two in global economies. If the main coastal cities of the US are affected by rising sea levels and significantly increased temperatures then everything from supply chains to production, to ports, to trading patterns and everything in between will be effected.

Changes in production have already taken effect, with the length of the frost-free season increasing nationally within the US since 1980’s. This has understandably had effects on US agriculture production. (NASA)

What’s more, is it is predicted that by next year (2020), between 75 and 250 million African people are projected to be exposed to an increase in water stress – a result of this would be a reduction of up to 50% of crop yields for some regions. (USGS)

The global ripple effect from mediocre climate change threats such as rising sea levels will potentially be the silent killer of world economies if nothing is done. Yes people can relocate, but that option is not on the table forever and in a world where we are already far too heavily populated, pushing masses of people into even smaller spaces will not result in anything good.

Low-Level

Low-level threats are those that are generations away, two-to-three hundred years into the future after the reality of many highly respected predictions have played out– in line with the prediction or not.

As we have seen above, the immediate and relatively short-term threats pose a significant change of dynamic for economies all around the globe. However, the implications of threats that are predicted to take effect in 300 years are those that will have the real impact on the world’s economy.

In 2200 and beyond, current emission predictions and the general consensus of experts is a rise of about 4-7 degrees which would cause our climate to be almost unrecognisable. Extreme weather conditions like nothing our generation of humanity has seen, and unworkable ocean conditions would play havoc on a globally dependant group of economies such as ours.

Take Japan for example, famously benefiting from a lower valued currency and focusing their economy toward the production for external demand. Much of Japanese income (almost 30% of GDP) is dependent on exporting demand. If ocean conditions and thus, transport risks are too volatile, that is a massive shock to the Japanese exporting community, and the rest of the world that imports from it.

According to a study by Yale Environmental, for millions of years global concentrations of carbon dioxide in the atmosphere held relatively steady somewhere between 260-280 parts per million – until about a century ago. If we think about the economic development of Man in the last century, we come to understand the industrial revolutions role in our current position.

Spring of 2018 reported a CO2 concentration of 410 parts per million, and it continues to rise. Because of this, as little as 20% of the air in the world today is expected to still be here by the turn of the third millennia.

Based on the rapid projections of CO2 emissions, it is not absurd to assume concentrations as high as 1,000 parts-per million in the next couple of centuries. According to studies, this mirrors that of some 50 million years ago when global temperatures were almost 30 degrees higher than pre-industrial levels. These types of temperatures would warrant certain parts on earth uninhabitable, and some even unbearable full-stop.

This type of ecosystem is not one our current economic landscape can survive on, and so almost every single industry would need to transform almost every aspect of their business procedure/ behaviours.

There is a term called Economic Climate Damage, and it is defined as the fractional loss in annual economic output at a given level of warming compared to output in the same economy with no warning.

Based on work collated by Covington and Thamotheram (2015), at around 4 degrees increase we begin to see certain experts predicting a 60% increase in economic climate damage, while some believe it will be nearer to 10%. However contrasting these are, almost all agree by the time temperatures have reached 10 degrees, economic climate damage will be at 100%. This means the fractional loss of economic output is absolute.

The economic ramifications of such temperatures are unfathomable, and to contemplate a basis upon which economic relations and activities could prosper is a tall task.

We spoke earlier about global sea levels and the rise of the next century. Instead if we look further down the line to about the year 2400, sea levels could be as much as 50 feet higher due to the melting of Antarctic ice sheets and polar caps.

With shores 50 feet higher and temperatures sometimes rendering people indoors, the economic implications mentioned above increase ten-fold. In terms of the survival of basic human life, the need for mass relocation would be chaotic. The redevelopment of trading patterns and supply chains would essentially need to be started from scratch, as we would be facing a totally different landscape.

Economic Indicators

At this point in the article, you will now understand that the ranking of the categories is not a reference to the severity but the time frame in which they will take effect. Economically, all of the above effects will contribute toward massively different practises. With increases in weather volatility, temperatures and sea levels the scarcity of land will rise also. With this comes inflation when it is paired with a general reduction in productivity.

Energy costs will rise and contribute to the aforementioned inflation. As temperatures rise, the increase in energy consumption that we are already seeing will increase even more resulting in a higher demand for energy. With a lower overall output of the global economy but a higher demand for such a universally crucial element such as energy, comes shockingly high prices.

With regard to unemployment levels, there are two potential outcomes. Due to the relocation and damages that are inevitable, one could assume that construction, planning and overall economic demand could contribute to a plentiful job market much like the aftermath of Katrina, but this wouldn’t last long. There is also the contrasting argument for mass unemployment when companies shut down due to the closures of certain industries, ports, and other landscape changes.

Lastly, GDP levels will suffer greatly. Although, much like unemployment the initial reactions to extreme weather and a changed climate may be positive – finding new markets or different approaches for current ones. However, once these never-before-seen weather conditions are normalised, and dangerous temperatures fill the atmosphere, many may not see the point in repairing damaged stock.

When this happens, GDP would take a sharp downward turn and this is not just because of lack of repair. With temperatures rising, comes increased risk of food security, risk of disease spreading and multiple other working conditions related risks. All of these stresses are burdened on the labour force, which will indefinitely struggle at this point.

All in all, Climate change holds very little for economic prosper. In the future, global markets and economic dynamics will be forever changed by the way the climate changes. There will be a demand for technologies that combat these extreme weather conditions, and also a likely increase in the demand for medical supplies as natural disasters increase.

It must be acknowledged, in the immediate aftermath of these global warming related disasters, humanity has bounced back well and in some cases even resulted in a better economic position than they first had.

However climate change is a long game, one which will not lose. It is therefore our job to minimise our effect as much as we can – humankind has not shown a particularly empathetic history, and one shouldn’t expect that of us now. But If human’s have done one thing consistently, its look out for their own interests and the above should point out how much the effects of a changing climate will have on our economies, our money and eventually our lives.