The gas giants: LNG, carbon, biomass

- Europe’s gas market remains vulnerable to volatility as global LNG dynamics, weather shocks, and geopolitical risks continue to influence prices.

- Political uncertainty around the EU Emissions Trading System (ETS) has pressured carbon markets, but strengthening the policy and reinvesting revenues could support industrial decarbonisation.

- Torrefied biomass pellets are gaining attention as a lower-carbon coal alternative, though supply growth and higher production costs remain key challenges.

What forces guide the key commodity markets of liquid natural gas (LNG), carbon, and biomass?

Turbulence returns to European gas – just a blip?

By Natasha Fielding, Editorial Manager: European Natural Gas, LNG, and Biomass, Argus Media

Since the 2022 energy crisis, when Europe’s sudden loss of most Russian gas turned global gas markets upside down, a turning point has been permanently on the horizon. The massive buildout of global liquefied natural gas (LNG) export capacity, it was prophesied, would eventually bring down global gas prices, calm volatility, and possibly even tip gas markets into oversupply.

It seemed as if this new era might arrive ahead of this winter, and the feeling lingered into December 2025 when prices kept falling. Unexpectedly strong global LNG supply growth and weak demand in Asia appeared to have allowed Europe to get away with entering the winter with its lowest underground gas stocks since 2022.

That was, until about the second week of January 2026, when a price rally at Europe’s benchmark Title Transfer Facility (TTF) gas hub began, which culminated in the Argus front-month index breaching €40 per megawatt hour (MWh) twice for the first time in nearly 10 months.

At least three things were to blame.

- First, cold weather forced households to crank up their heating, triggering a rapid draw on underground storage, and forecasts were pointing to another cold snap in mid-February.

- Second, a severe storm in the US sent domestic gas prices soaring and briefly curbed US LNG exports.

- And third, escalating Iran-US tensions raised the risk of a disruption to the key Strait of Hormuz shipping channel, through which all Qatari LNG supply must pass.

Prices have since fallen again, as some of those risks faded. Was this return to volatility an outlier, the consequence of several unusual events happening to coincide? Or are episodes of price turmoil an integral part of today’s European gas market? There are a few reasons to doubt that volatility will go away for good anytime soon.

The TTF is now a global price index thanks to LNG’s growing importance in Europe. For this reason, the European gas market price feels the ripple effects of goings-on in the global LNG markets in a way that it never used to, whether that’s an active US hurricane season or strikes at liquefaction plants on the other side of the world.

While LNG is now a key source of flexibility for Europe’s gas market, it tends to lag. The gap between price signals emerging and the supply of LNG in Europe can constitute weeks or even months.

Additionally, Europe is growing ever more dependent on its gas-fired power stations to balance out intermittent renewables, which is adding to variability and unpredictability in gas markets. In general, renewables are pushing the role of natural gas to the margins, but we still need to be able to ramp up gas-fired power generation on those dark winter days when the sun doesn’t peek through the clouds and wind doesn’t blow.

A final reason to pause before declaring the era of volatility over: while Western Europe already phased out Russian gas in 2022, southeastern Europe still relies on it. About 5% of Europe’s gas is still piped from Russia under the Black Sea. A full Russian gas and LNG ban will come into effect in October 2027, which will force some dramatic supply changes in the landlocked countries like Hungary and Slovakia that still utilise lots of Russian gas.

By mid-February 2026, tranquillity appeared to have settled over Europe’s gas markets. Will that last? If underground gas storage levels are anything to judge by, then we are not yet out of the woods. Underground stores may enter this April at their lowest since 2018, creating a big restocking challenge ahead of next winter.

Don’t blink: Carbon markets are under pressure, but the EU ETS should stay firm

By Erisa Senerdem, Global Lead Carbon, Argus Media

Europe’s Emissions Trading System (EU ETS) is facing one of the most delicate political moments in its two-decade history. In recent weeks, a swirl of lobbying, mixed political messages, and media speculation has sent carbon prices sliding and triggered a wave of nervous commentary across the bloc. But as the pressure mounts, one point must remain clear: this is no time for Europe to back down.

At the heart of the storm is the upcoming ETS review, due this summer. The benchmark front‑year European Union (EU) ETS allowance price dropped nearly 6% on 5 February after rumours circulated that the European Commission was considering weakening the system. Officials quickly dismissed the reports as a “mix‑up,” but the damage was already done. Markets were once more reminded of just how politically exposed the ETS can be.

The industry’s current anxiety is rooted in broader economic challenges the ETS did not create: manufacturers are struggling with volatile energy prices, trade uncertainty, and geopolitical shocks. Carbon emissions prices account for only a portion of these pressures. Yet the ETS, being an easily controllable policy instrument, has become a more direct target than global energy markets or macroeconomic headwinds.

The political reaction has been swift and contradictory. German Chancellor Friedrich Merz triggered a sharp fall in carbon prices when he suggested the ETS should perhaps be postponed – only to reverse his comments a day later, calling the ETS “the right, effective instrument” that has helped Europe grow economically without increasing emissions. French President Emmanuel Macron called for “concrete” measures to ease the ETS burden; Belgium’s Bart De Wever and the Czech Republic’s Andrej Babiš have echoed similar concerns.

Though such calls are rooted in good intentions, they are likely to cause confusion and doubt surrounding the ETS, harm its credibility and achievements, and undermine investors’ confidence in decarbonisation of heavy industry in the long run.

Europe’s emissions from power generation have halved over the past decade, a direct result of the successful delivery of the EU ETS and related policies. It has not always been a smooth ride and has come at high costs for fossil-fuelled generators and consumers. But at the same time, the policy has pushed companies and governments alike to think outside the box and find effective ways to decarbonise. Now the EU is gradually phasing in the ETS to key hard-to-abate heavy industries such as steel, aluminium, fertilisers, and cement.

Today’s environment is challenging to operate in, and rising carbon bills only add to the pressure European industry is facing. But this is no time for the continent to retreatfrom its emissions and broader climate policies and let go of what it has already achieved. The EU should continue to strengthen its decarbonisation path and extend its leadership worldwide. Despite all the challenges, there is a constructive path forward, one that strengthens rather than weakens Europe’s climate and industrial policy.

First, member states must use ETS revenues to support industrial decarbonisation. European Commission President Ursula von der Leyen revealed in Antwerp that although the ETS has generated more than €260 billion since 2005, less than 5% is reinvested into industrial transformation. That is a policy failure, not a flaw in the ETS itself. Recycling these revenues into clean technologies, electrification, energy efficiency, and industrial-scale innovation would directly address industry concerns.

Second, Europe must stand firmly behind the Carbon Border Adjustment Mechanism (CBAM). The mechanism is aimed at preserving European heavy industries’ competitiveness – as they increasingly pay more for their emissions – by forcing goods produced in non-EU countries to pay the same price for their products’ embedded emissions. This creates a level playing field for all goods that enter the EU market from outside the bloc.

The commission has already combined the above two instruments in a recent proposal to protect CBAM-affected exporting sectors through direct subsidies funded from national member states’ CBAM revenues (currently under consideration by the European Parliament and Council).

Companies will also be more likely to invest in areas with strong and stable policy signals, only reinforcing the importance of the EU’s standing by its carbon and climate policies.

Europe has the right tools. What it needs now is political calm and strategic clarity. Diluting the ETS would undermine investment, weaken Europe’s credibility and stall the transition industries must make to stay globally competitive. Strengthening CBAM and reinvesting ETS revenues offers a far smarter and more sustainable path.

Faced with economic headwinds, Europe must hold its nerve. The ETS is not the problem – it is part of the solution. The real risk is not pressing ahead, but losing momentum now, just as the rest of the world accelerates.

Biomass fuel evolution: Torrefied pellets making headways across industries

By Hannah Adler, Senior Reporter: Biomass, Argus Media

Torrefied pellets have become a focal point for heavy industries and power generators seeking practical ways to replace coal with renewable energy without breaking the bank.

Pellets are small, dense cylinders of compressed biomass material used as fuel. Companies have been thermally treating – or torrefying – them for over a decade to make them burn at temperatures closer to coal. And as more industries commit to reducing emissions, it is starting to become a serious market to watch.

Torrefied pellets have calorific values of 4,300-5,500 kcal/kg compared to around 4,000 kcal/kg for untreated white pellets (conventional wood pellets). They’re also more water-resistant and grind more easily than white pellets, can be handled similarly to coal and used in coal-fired boilers without major modifications.

Interest levels in torrefied pellets differ around the world. Japan has so far emerged as the strongest new demand centre. Japanese coal-fired utilities prefer them over traditional wood pellets, as boilers require no retrofitting and ports have limited space. In pulverised-coal boilers, torrefied pellets can account for approximately 50-30% of the fuel mix, compared with just 5-10% for conventional wood pellets. Some utilities in northern Japan have already begun or plan to start burning torrefied wood pellets with coal in thermal-fired plants.

Demand growth for torrefied pellets in Europe will likely be slower, as utilities have already retrofitted most coal-fired power plants across the continent to burn wood pellets. European Union (EU) research project SECTOR pointed out that the torrefied pellets’ “potential end-user markets are…small to medium scale heat and combined heat and power (CHP)”, but so far, there has been no actual implementation.

Hard-to-abate sectors, like steel, cement, chemicals, and sustainable aviation fuels (SAF), are also considering using torrefied pellets to decarbonise and reduce reliance on fossil fuels. Steel producer ArcelorMittal’s Torero project in Belgium burns torrefied biomass in its blast furnace; last year in Japan, steelmaker Kobe Steel (Kobelco) announced a trial to partially substitute coal with torrefied pellets in blast furnaces.

But the supply of torrefied pellets may struggle to keep pace with demand. Global capacity to thermally convert solid biomass – including torrefied pellets, charcoal, and biochar – currently amounts to around 609,000 tonnes/ year (t/y) and may grow to around 1.7 million t/yr this year and 13.8 million t/yr by the end of 2030.

Several thermal treatment production projects have recently come online or are planned across Asia, North America and Europe over the next decade:

- In Asia, Idemitsu began commercial operations at its 120,000 t/yr torrefied pellet plant in Vietnam in October last year and is targeting at least 3 million t/yr in the 2030s.

- Kobelco signed a letter of intent in 2025 to build a torrefied pellet facility in Malaysia this year, starting at 300,000 t/yr.

- In Europe, Finnish firm Taaleri runs a 60,000 t/yr torrefied biomass plant in Joensuu.

- In the US, engineering firm TSI launched a 3 tonnes/ hour (t/h) demonstration torrefaction plant last year.

- Australia’s Foresta is developing a torrefied pellet and pine‑chemical facility in New Zealand.

Price may also be a hurdle for the rollout of torrefied pellets. They remain more expensive to produce than coal, and more expensive to buy than conventional biomass, particularly since 2022 (when the cost of fibre, energy, and labour all rose). And while certain countries may encourage biomass adoption, private investors must shoulder most of the risk because no governments are offering direct financial support to companies looking to make or buy torrefied pellets.

Taken together, the future growth of the torrefied pellet sector will depend on how quickly supply can scale and whether enough off-takers emerge to encourage technology providers, producers, and their financial backers to invest in new sites, build commercial-scale plants, and secure feedstock.

Noble only in name: Sulphur and sulphuric acid

- Sulphur, once treated as a waste by-product of oil and gas refining, has become a high-value commodity.

- Rising sulphur prices have pushed up costs across downstream industries, increasing pressure on farmers and potentially affecting the wider global food supply chain.

- Sulphuric acid has seen a tightening global supply and higher prices after China announced a temporary 50% cut in exports amid soaring domestic sulphur costs.

What forces guide the key commodity markets of sulphur and sulphuric acid?

Sulphur price spike drives cost increases, from food supply chains to industrial processes

By Maria Mosquera, Editor Sulphur Products, Argus Media

Raw material price bull runs raise prices from the root of the supply chain. Sulphur prices are a case in point.

Sulphur is a by-product of oil and gas refining, which used to be viewed as a waste stream to be evacuated. However, today it is a commodity in its own right, with producers looking to maximise margin on sales.

The phosphate fertiliser industry is the largest consumer of sulphur, so demand has traditionally been seasonal and tied to fertiliser application periods in major consuming markets.

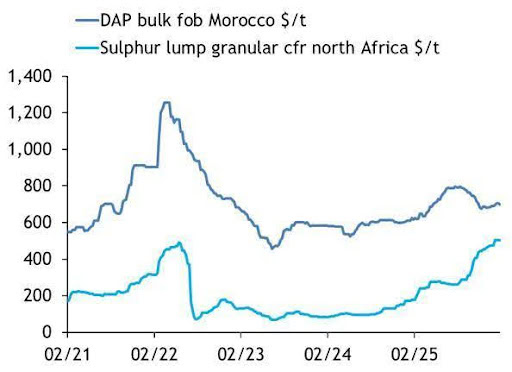

North Africa delivered sulphur raw material price compared to the phosphate fertiliser diammonium phosphate (DAP). Morocco’s export price chart reveals a correlation over a longer time frame.

Source: Argus Sulphur and Phosphate price reporting service

The energy transition has had a two-fold impact on sulphur. On the one hand, supply growth has slowed as new oil and gas refining projects no longer attract the same level of investment. On the demand side, the transition to electric vehicles and the batteries needed for this industry has created demand growth for sulphur, converted to sulphuric acid, and needed for the purification of metal ores like copper and nickel for use in the downstream industry. This sector has grown quickly thanks to government subsidies and political moves toward lower emissions.

Geopolitical factors have also had an impact on sulphur supply, with Russia a large exporter of the product, and the introduction of sanctions following the onset of the Russia-Ukraine conflict marginalising this supply.

Outside of the former Soviet Union, much of the supply of sulphur is consolidated in the Middle East; Canada also supplies significant volumes to the international market.

Compared with the downstream products it supplies (such as phosphate fertilisers), sulphur prices have reached historic highs. Those producers have grown pressured to increase downstream prices because of the rising costs of raw materials. Knock-on impacts of these rising costs could impact macro-level industries like caprolactam, nylon fibres, water purification, and pharmaceuticals; but rising fertiliser prices would likely result in direct pressure on farmers, as increased costs add pressure to the global food chain.

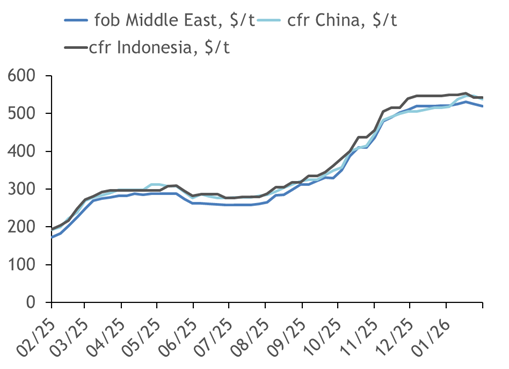

The graph below tracks sulphur price evolution, 2025 to early 2026, from major suppliers in the Middle East to key markets in China and Indonesia:

Source: Argus Sulphur price reporting service

Sulphuric acid: The ‘King of Chemicals’

By Jasmine Antunes, Senior Reporter, Sulphur and Sulphuric Acid, Argus Media

Most sulphur is burnt into sulphuric acid, with sulphur as a bulk product being easier to transport and store for large consumers of sulphuric acid.

Sulphuric acid is the most widely traded and used chemical in the world, often referred to as the “King of Chemicals”. It is also hazardous, requiring strict handling and transport. Most sulphuric acid is produced by burning sulphur for downstream use, but it is also produced or involuntarily as a by‑product of copper, nickel, and zinc smelting. While sulphuric acid is closely linked to sulphur, it has its own market dynamics and trades as a standalone commodity.

Most sulphuric acid is used as a raw material for fertiliser production, but consumption is growing in the metals industry, notably the battery metals sector.

The supply of smelter acid is largely concentrated in northeastern Asia; following a rapid rise in copper smelter capacity, China has emerged as the leading exporter of sulphuric acid. The commodity sees strong demand from the usual sulphur‑importing regions (China, Morocco, Brazil, India), as well as to support Chile’s copper industry.

With the significant rise in sulphur prices over the past year, consumers who have sulphur-burning capacity have, at times, opted to buy more sulphuric acid instead of sulphur. This has contributed to the recent increase in sulphuric acid prices.

Smelters have been faced with a sharp decline in treatment and refining charges (TC/RCs) through 2025, stemming from tight global copper concentrate supply, creating more pressure on smelter margins. In China, for instance, smelters have relied on their sulphuric acid sales, both at home and abroad, to bolster margins.

But in January 2026, it was announced that China would reduce sulphuric acid exports between January and April by 50%, following a steep increase in domestic sulphur prices that inflated fertiliser production costs. The reduction in sulphuric acid export availability from China over this period is tightening global supply and driving up prices.