Elucidating the dilemma faced by bankers in stressed economies by exploring feasible options in case of trade credit default, using India’s Buyers’ Credit market as reference.

Buyers’ Credit – Importers’ Elixir

As per WTO estimates, 80-90% of global trade is financed by short term funding primarily being trade credit and insurance/guarantees. Every form of funding has an interest cost associated with it. Developing economies have high inflation costs and thus consequently have high-interest rates. It is in such economies that trade credits are actively used as a panacea for reducing working capital costs.

In India, the average lending rate for cash borrowings is in the range of 7-13% depending on the credit and risk rating of the borrower. Keeping everything else constant the same borrower can undertake trade credit financing at the rate of 3-4%. Thus trade credit financing reduces interest cost by half. One of the most prominent trade credit product used in the Indian market is buyers’ credit. Buyers’ credit is a trade credit product used by importers to avail financing for payments towards executed trade transactions. As per India’s central bank, i.e. Reserve Bank of India (RBI), 93% of cross border trade credit in India is in the form of bank-intermediated buyers’ credit.

The Product

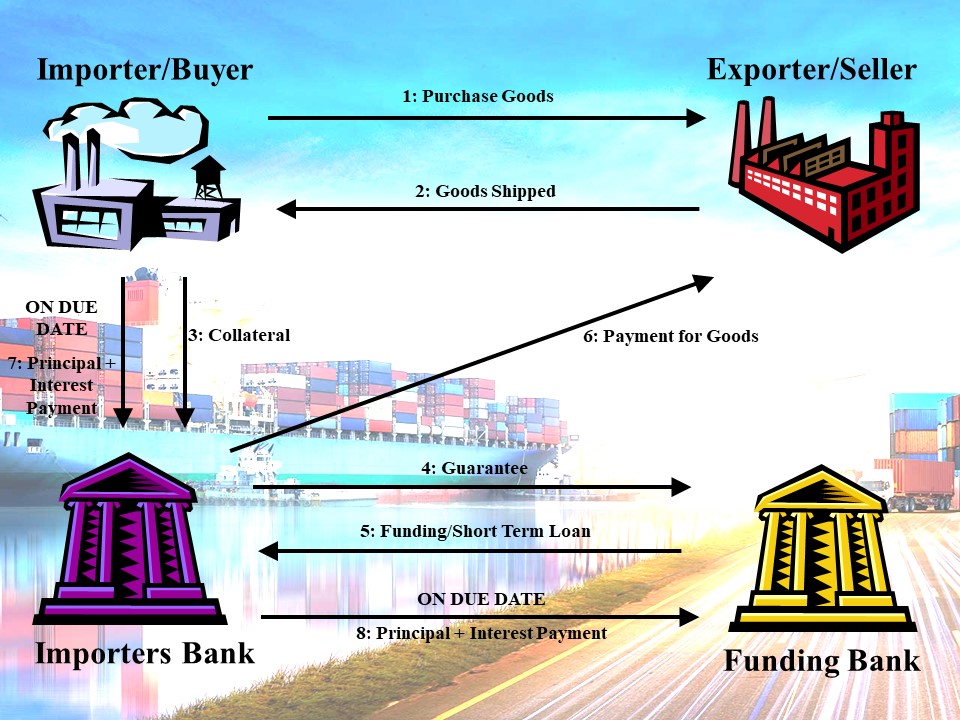

Every buyers’ credit has an underlying transaction. The underlying transaction can be a Letter of Credit, collection document etc., i.e. any trade instrument wherein an importer/buyer has to make a payment to the seller in another country. When the payment for the underlying transaction has to be made by the buyer, a loan is availed in foreign currency from a bank or financial institution, to make the payment in question. This loan is called buyers’ credit.

Buyers’ credit is a straight forward product. There are three (3) parties involved in the transaction – importer/buyer/borrower, borrowers’ bank and funding bank. On the basis of a guarantee issued by the borrowers’ bank, on behalf of the borrower, a foreign-based bank funds the borrower through borrowers’ bank. On the due date/maturity of the funding/loan, the borrowers’ bank makes payment to funding bank along with interest.

The credit risk for the funding bank would be on the borrowers’ bank issuing the guarantee. The permissible funding is up to one (1) year for working capital, with chances of over-financing. In 2013, RBI brought about an amendment to the buyers’ credit maturity, which implied that instead of one (1) year, buyers’ credit maturity was not to exceed the operating cycle for working capital transactions. This curtailed, to a certain extent, unchecked over-financing. However, the definition of the operating cycle was still at the discretion of the lender. With an everlasting pressure on banks to lend more in the growing economy, the banks were willing to fund on inflated and elongated operating cycles.

Buyers’ Credit Scam

With the shocking revelation from one of India’s premier public sector banks in May 2018, having been defrauded of $1.4 billion by a diamond merchant, RBI immediately discontinued buyers’ credit, the defrauding instrument. However, in early 2019, under pressure from anaemic markets, RBI allowed buyers’ credit and the phoenix arose albeit in a new form. Instead of the borrowers’ bank as in the earlier version, the new form encompassed the foreign bank undertaking credit risk on the importer i.e. the buyer, with the funding being secured by a standby letter of credit (SBLC) issued by the borrowers’ bank. The new method wasn’t different in substance from the earlier one, except for the fact that the foreign bank was lending directly to the borrower.

Operating Cycle in Shrinking Economy

Short term trade transactions are inherently aimed towards optimizing working capital operating cycles, according to this article. An operating cycle refers to the period from putting cash into operations until realizing the cash. The objective is to realize cash at the earliest to provide more rotations and improve liquidity. Operating cycle is inherently a function of inventory holding and accounts receivable holding.

There is a direct correlation between economic stress and receivable holding levels. During periods of economic stress, liquidity is a challenge and payments get delayed. This, in turn, elongates the receivable holding period and consequently the operating cycle. The other cause for operating cycle elongation is the inventory level holdings. With market liquidity shrinking, there is less disposable income with the end consumer who has a higher propensity to save and a reduced need for purchasing, leading to high inventory holdings.

In the current global pandemic scenario, when everything has come to a standstill, entities are struggling with the realization of payments and achieving sales targets. In a supply chain analogy, the creditor is trying to realize its payment at the earliest while the debtor is trying to delay making the payment. This turns into a cyclic catch-22 situation, which, more than often, requires external impetus to get the cycle moving.

The Bankers Dilemma

Buyers’ credit as mentioned earlier is backed by a guarantee. The foreign bank funds the borrower on the basis of SBLC provided by the domestic bank. Domestic bank for the purpose of issuing the SBLC may undertake suitable collateral depending on the risk valuations of both the transaction and the borrower. The collateral itself, most of the times, is overvalued and its value shrinks further in low liquidity market scenarios.

For existing buyers’ credit, the liability on the due date has to be extinguished using funds from the borrower. The borrower, however, due to the credit crunch is unable to pay the domestic bank on the due date. The banker at this juncture has two options:

- Devolve the account and honour the SBLC by making payment to the foreign bank and try recovering from the borrower later; or

- Rollover the buyers’ credit and postpone the due payment from the borrower.

In the first option, due to non-payment by the borrower, the domestic bank would have to pay and would be out of funds. The probability of the banker recovering the funds is extremely slim as the borrower would use its available funds to make purchase payments. In the event the account is not standardized within ninety (90) days, the domestic bank would have to categorize the account as stressed.

Non-Performing Asset

A stressed asset/account is classified as a bad loan or a Non-Performing Asset (NPA) if the principal or interest remains overdue for a continuous period of more than ninety (90) days. Once an asset becomes NPA, the lender needs to start provisioning for the asset. The capital conversion has been a monumental concern for Indian banks since the subprime crisis and the severe capital requirements as per BASEL – III guidelines. Among all this, there is an unsaid endeavour by bankers to conserve capital and prevent any provisioning that may be required on account of NPAs.

ARTICLE: Basel III – What is it and what will it mean for alternative finance? A Basel III Guide for Dummies

The provisioning requirement for the first year is 15% on the overdue amount and increases year on year as a function of available collateral. Additionally, there is an opportunity cost. The bank could have used this capital to fund another transaction amounting to 135% of the overdue value and would have earned fee and income on the same. All in all, this scenario is negative for the bank.

For a banker staring at an NPA, the second option looks like an obvious choice. Rolling over the buyers’ credit for a short term would provide an opportunity to the borrower to make the payment on a future due date and also for the banker to defer capital freeze. This being said, as per RBI guidelines, the bankers can rollover the buyers’ credit only for a period within the operating cycle.

The pertinent question that follows is – who decides the operating cycle now, especially in a scenario where there is no historic record to adjust and measure the severity? If the banker follows the existing operating cycle tenor, then rollover would not be possible. Even if the banker extends the operating cycle, a logical explanation for arriving at the revised operating cycle tenor cannot be fathomed and would be subject to audit. The paradox gets compounded for multiple transactions of the same borrower, as the default amount can run into billions.

Regulators Push

The banker walks a tight rope with little flexibility in terms of discretionary decision making. It is here that the role of the regulator as a facilitator emerges. Banks globally are facing credit challenges and with deteriorating asset quality, bad loans are poised to increase. China is the latest to acknowledge the same. “Asset quality at smaller banks will also be under pressure this year, and credit risks in some institutions will continue to accumulate,”, according to a statement sent by China’s Banking and Insurance Regulatory Commission (CBIRC) to Reuters.

That being said, an impetus is required from the banking regulators in such testing times. In recent times, there have been subtle hints of alleviation of lacunae from central banks and banking regulators. Moreover, regulators have gone a step ahead with relief packages under the ongoing pandemic. Most economies have allowed deferment of mortgages/loan payments. Such exemplary relief measures instill confidence in the economy as a whole and avert the banker from making unqualified decisions which may have macro implications in the longer term.

Considering the Indian context, on March 27, 2020, RBI Governor Shaktikanta Das said,

“In respect of all accounts for which lending institutions decide to grant moratorium or deferment, and which were standard as on March 1, 2020, the 90-day NPA norm shall exclude the moratorium period, i.e., there would be an asset classification standstill for all such accounts from March 1, 2020, to May 31, 2020,“.

Technology to the Rescue

The emergence of advanced analytics is one of the biggest disruptions in financial services. As per a recent McKinsey Global Institute study, the annual potential value of artificial intelligence in banking is as much as 2.5% to 5.2% of revenues or $200 billion to $300 billion annually. Maturing technologies like Internet of Things (IoT), Artificial Intelligence (AI), Machine Learning (ML) and Blockchain/Distributed Ledger Technology (DLT), to name a few, harness enormous computing power to provide insights and results that are eye-opening. DLT is turning out to be a key technology, supporting digital data recordings for trade finance. AI-based compliance tools assist with transaction monitoring and sanction screenings. AI and ML along with analytics can drastically increase risk identification and mapping for banks. Advanced analytics simulates millions of scenarios to find patterns at different levels.

Early warning signals’ models can be developed using machine learning based on time series and trends that are determined using macroeconomics and market data. Furthermore, these models are self-evolving, growing on latest market data. A well developed AI network can provide accurate inventory and receivable holding levels for each borrower at any given point in time. By leveraging technology for insights, a banker can make well-informed decisions, in compliance with audit and ethics, which are in the best interest of the bank.

For our banker, the dilemma of stretching the operating cycle for trade credits is best addressed through analytics and technology, which can be used to predict collections and probability of trade credit defaults. The banker can arrive at the optimum operating cycle period, factoring in the global scenario and, as a result, taking a conclusive call to either extend buyers’ credit or declare the account as stressed.

This article was written by a member of TFG’s 2020 International Trade Professionals Programme. Find out more here.

Disclaimer: The views that have been expressed on this page are that of the author, which may or may not be in line with their company, Trade Finance Global or London Institute of Banking and Finance’s view.

Type a message