Estimated reading time: 6 minutes

International trade operates on financing and debt. Without lending and borrowing, corporates would not be able to function, and countries would be unable to develop or grow. Yet, many industry experts and experts see the rising debt levels across the developing world as a cause for concern.

According to a Bank of Canada and Bank of England report, in 2021, global government debt stood at 98.3% debt-to-GDP. Holding this level of debt for a prolonged period of time creates numerous problems, especially once an unexpected shock hits the market.

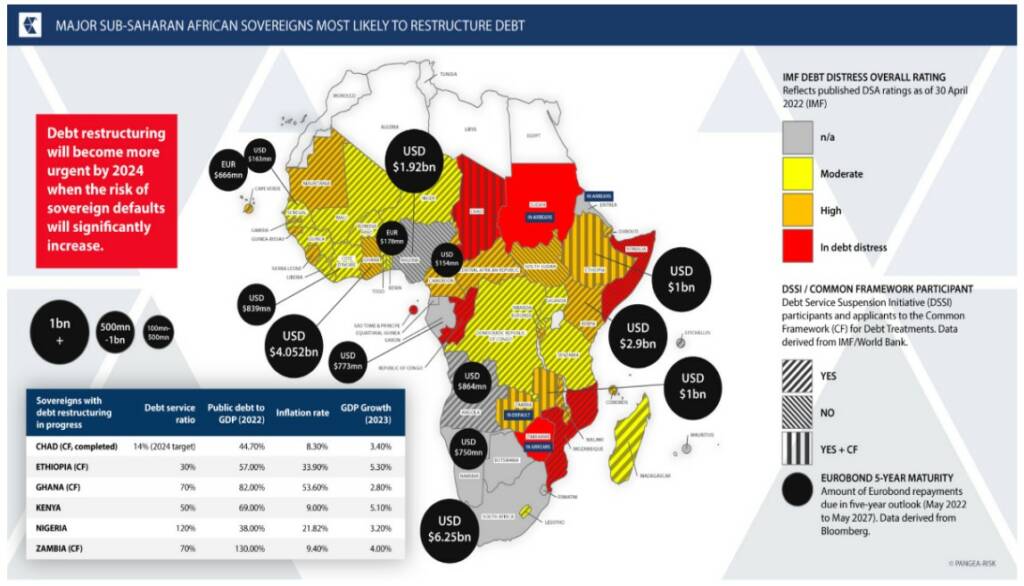

Pangea-Risk and Acre Impact Capital’s whitepaper, “The Politics of African Debt Restructuring”, reports that the African continent is especially vulnerable to debt-related shocks, as private and public debt increased to more than $700 billion from 2000-2020.

However, the specifics of African sovereign debt are incredibly nuanced and require a deep dive into country-specific situations and multilateral relationships. To get a better understanding of this subject, Trade Finance Global’s (TFG) Deepesh Patel sat down with Robert Besseling, CEO of Pangea-Risk at ExCred International in London.

A looming expiration date

The accumulation of over $700 billion of debt over the past 20 years has created an uneasy environment for many analysts. The IMF stated that 22 low-income African countries are in or at risk of debt distress. Many of the loans are due to be serviced in the next two years, creating some fear of further market turmoil.

Besseling said, “From 2024 onwards, we’ve got some really big Eurobond capital repayments that are due, and even more so in the four-year outlook.”

However, these developments are not dire, as some African countries, such as Kenya, Ghana, and Angola, have successfully restricted their debt in recent years. According to Besseling, 2023 is the year to focus on further debt restructuring.

Besseling said countries need to “retreat their debt naturally, not just restructure with a haircut…our white paper argues that debt can be reprofiled, it can be swapped, it can be treated in different ways.”

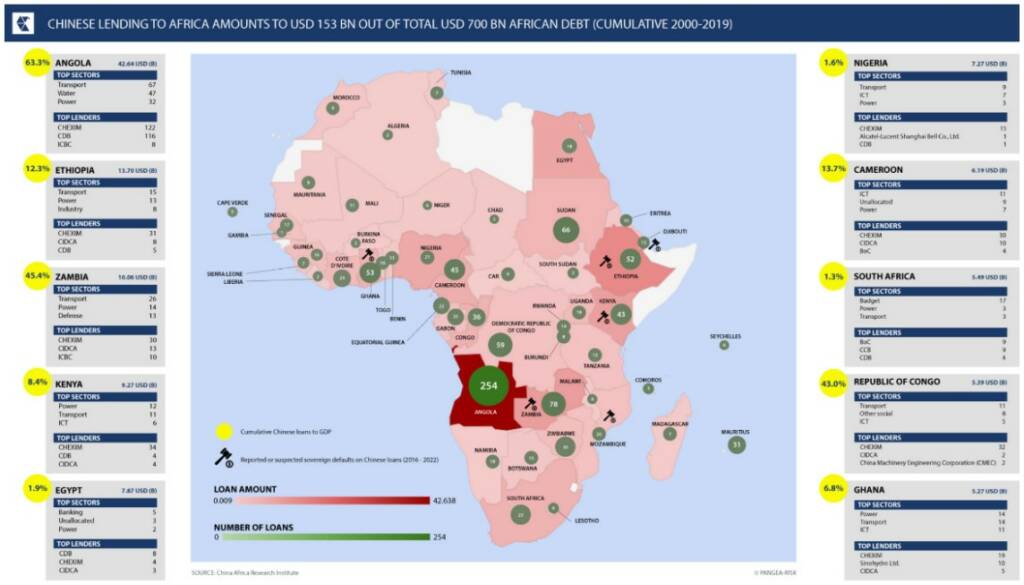

One of the most common misconceptions surrounding the African debt situation is that there is a ‘Chinese debt trap’. This is a phrase one commonly hears from television commentators, from politicians and academics. But by looking at the numbers closely, it becomes apparent that there is not an overwhelming Chinese debt trap.

Out of the $700 billion debt in Africa, $150 billion of it comes from China. While a large number, it only represents roughly 21% of total debt. Besseling pointed out that over one-third of the $150 billion came from Angolan pre-export finance facilities for crude oil.

Simply stated, most of Africa is not exposed to Chinese debt. Besseling said, “Five or six African countries are heavily exposed to China. That’s only 10% of the African continent.”

Additionally, China has shown flexibility in restructuring loans or providing debt relief. The Pangea-Risk and Acre Impact Capital whitepaper says, “between 2000 and 2019, China … cancelled at least $3.4 billion of debt in Africa”. In the same period, China restructured or refinanced about $15 billion of debt in Africa. There were no asset seizures, and China has not used legal recourses to compel repayments.”

Though the “Chinese debt trap” may not be as prevalent or fatal as some might think, 2023 will still be an important year to restructure African debt before the large debt obligations are due.

There have been some efforts by multilateral institutions to help the African debt issue. However, none of them proved to be successful. A “Common Framework” was created with the G20, IMF and World Bank, looking to treat the Paris Club concessions and the Chinese debt trap.

Besseling said this excludes “Eurobond holders, domestic bondholders, commercial lenders, ECAs and banks.”

Besseling believes that there needs to be a different solution to debt restructuring. “Multilaterals at the moment are offering a multilateral approach to debt treatment, and there is no precedent of success for that.”

African climate finance and political instability

According to multiple studies, Africa is the most vulnerable continent to climate change. Besseling said, “It would make sense that the bulk of climate finance should go to Africa.”

But in reality, roughly 11% of global climate finance goes to the African continent, most of which is financed by concessional lenders and multilateral development banks. According to Besseling, very little private sector money is invested in Africa.

African Development Bank research shows a $100 billion annual financing gap for critical infrastructure in Africa, such as electric grids, water supply and sanitation, and transportation.

Why is this the case?

Besseling believes, “It’s because of the fear of African countries defaulting on their sovereign debt and high political risk.”

The private sector is particularly concerned with perceived political, economic and social instability. Countries that have had recent contentious elections or military interventions are highly unlikely to receive private investment.

The African continent needs private investment to counter the climate crisis, but lenders are more hesitant than ever. Besseling notes that the Pangea-Risk and Acre Impact Capital whitepaper focuses on this conundrum.

“Our White Paper argues that there should be debt treatment on domestic debt, sometimes also on Chinese debt or concessional debt. And if we follow that road, then we can put more African countries on a trajectory in which they will treat their debt in 2023, make it more sustainable, more affordable, avoid defaults from 2024 onwards.”

Besseling believes that once African countries properly restructure their debt and avoid a potential default, private investment will increase. As debt burdens become more sustainable and affordable, their country-risk premium will decrease in tandem.

“I think it’s increasingly important to start looking at African debt from a data perspective rather than from the narrative that is currently circulating.” By looking at African debt through a data lens, one can see a sustainable future for Africa.

Key findings

After analysing the data, the Pangea-Risk and Acre Impact Capital whitepaper summarised six key findings.

- Debt transparency, responsible monetary and fiscal policy and stable institutions are important criteria for debt treatment.

- IMF needs to play an important role as a lender of last resort and policy anchor.

- Credit ratings have restricted African countries’ access to private capital.

- The “Common Framework” is not a successful debt restructuring program for Africa.

- Chinese creditors will be impacted the most by debt defaults and restructurings.

- African governments are looking to prioritise domestic debt solutions to help internal stakeholders.

Read “The Politics of African Debt Restructuring” to learn more about country-specific cases and the detailed takeaways.