In the commodities super cycle that has emerged out of the COVID-19 pandemic, few resources have seen as much volatility as liquified natural gas (LNG).

From record lows to record highs in less than 18 months, LNG’s ups and downs are perhaps rivalled only by crude oil, whose 300% plunge to -$40 a barrel in April 2020 is one for the history books, and one for future economics students to ponder.

But unlike oil’s flash crash, LNG’s roller coaster has been a much more sustained affair, taking it from a pandemic low of around $2 per million British thermal units (mmBtu) in May 2020, to $34.1 mmBtu today – an increase of more than 1,600%.

What has been driving this unprecedented volatility in LNG, how long will it last, and how is the industry preparing itself for the future?

LNG, oversupply, and its bounce back from the pandemic lows

According to a 2020 study by McKinsey & Company, LNG was expected to enter a period of low prices and oversupply in 2020 and 2021, as growth in new production projects outstripped growth in demand.

That dynamic was then rocked into overdrive by the COVID-19 pandemic, which precipitated a collapse in demand as rolling lockdowns made their way around the world’s major economies.

This year, after demand bounced back from the low baseline of the pandemic, LNG has struggled to keep up, as inventories remain critically tight both in Europe and Asia.

Demand has also been lent a helping hand by the cold Northern Hemisphere winter of 2020.

But despite the plain sailing weather-wise, LNG continues to be troubled by production and storage issues.

Coal shortages in China have led not only to power outages in one of the world’s largest markets, but also to greater competition for energy between Asia and Europe.

Richard Bowler, head of LNG trading and portfolio operations at Eni Global Energy Markets, said this dynamic has opened up a new front – a kind of continental storage wars – in the global battle for LNG.

“Over the course of the last three or four months, as Europe has failed to sufficiently fill its storages, we’re now seeing a battle between Europe and the East for who can command, who can afford to stock up their energy reserves,” he said.

A resurgence of COVID-19 both in China and Europe has also led to further lockdowns and sporadic supply chain disruptions, coupled with labour market distortions and rampant inflation.

Against this backdrop, volatility is still the recurring theme for LNG, but so too is uncertainty and ambiguity, particularly when we consider the shift in investor sentiment away from fossil fuels and towards green energy and renewables.

Rosario Sgarioto, head of LNG trading at SOCAR Trading, said that one of the main challenges now facing the LNG industry is the difficulty of predicting how demand will evolve, which is intrinsically tied to energy policy in individual markets.

“We know that China is the biggest participant and can become a market maker – they can effectively move the market significantly,” he said.

“And we have certainly tested that more than a few times. But the ability of these big countries to buy more or less gas and to formulate that demand forecast is strongly driven by policy, and policy has created a great degree of uncertainty in the marketplace.

“All these elements combined together are creating the perfect cocktail to create these huge imbalances, as we’re seeing today.”

Uncertainty and energy transition

In June this year, a study by BloombergNEF found that the global LNG market is likely to be oversupplied until 2025.

Significantly, the study found that US liquefaction capacity could rise by more than half, overtaking Australia’s by 2024.

And while structural global LNG demand could rise by 14% by 2025 – driven by Europe, China, South and Southeast Asia – demand in traditional markets such as Japan, South Korea, and Taiwan is expected to flatline.

Moreover, pressure is mounting on the LNG industry – and the energy sector in general – to lower its carbon emissions, creating what the study calls an “unclear” investment and demand outlook “beyond 2030”.

However, while recognising the shift in sentiment towards fossil fuels, traders such as SOCAR’s Sgarioto believe that LNG has plenty of staying power over the next few decades.

“There’s been a lot of talk as to what’s the remaining life of the gas industry,” he said.

“Are we in a short circuit scenario whereby in 10, 15, or 20 years’ time, the gas industry will disappear simply because everyone has to become green?

“I think the situation is a lot more complex than that.”

Sgarioto’s points to the difficulty of coordinating national energy policies on a global scale, particularly with regard to timeframes and emissions reduction targets.

India, for example, has said it cannot deliver on net zero until 2070, and China typically maintains its distance on climate issues, not even bothering to turn up at COP26 in Glasgow last month – “a strong political message”, as Sgarioto put it.

“If there is no harmony across nations as to how they’re going to implement the green policies going forward, I think it’s just going to create more confusion and uncertainty, and how is gas going to play within this?” said Sgarioto.

“Whether we like it or not, gas is still going to be here, and signals of this are being given by the big amount of long-term contracting activity that we have seen recently.”

For example, only last month China signed its largest ever long-term LNG contract – via state-owned Sinopec – to purchase 4 million tonnes annually for 20 years from US-based Venture Global LNG.

Likewise, in July this year South Korea’s state-owned Korea Gas Corp signed a 20-year LNG supply agreement with Qatar Petroleum to purchase 2 million tonnes per year.

And in October this year, Qatar Terminal Limited (QTL), a subsidiary of Qatar Petroleum, signed a 25-year storage deal with the UK’s National Grid Grain LNG.

As Sgarioto concludes, energy superpowers such as China may have other priorities on their mind when it comes to climate change.

“For the little that we know about China, I don’t think that China is going to commit to definitive energy transition timelines and targets at the detriment of its own domestic policies, and at the detriment of making sure that the domestic economy is robust in growth and GDP,” he said.

A niche for LNG – the dark horse of fossil fuels

Other LNG professionals point out that, even if decarbonisation of the energy sector were to accelerate, reducing LNG consumption would be of minor importance compared to that of coal and oil.

Jonathan Westby, senior vice president at JERA Global Markets, said that in such a scenario, LNG will be recognised as the greenest of the fossil fuels, and will be prioritised accordingly.

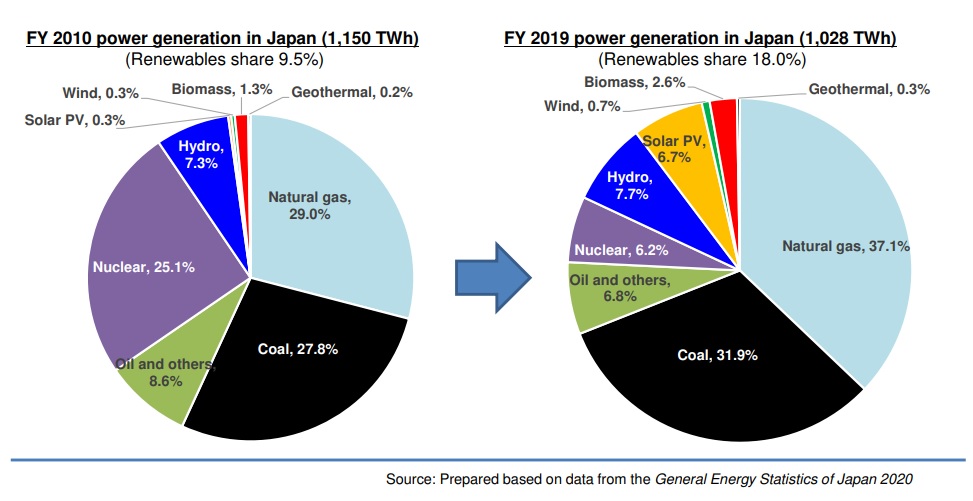

From JERA’s base in Japan, Westby points out that the Japanese government has projected that, in 2030, gas will still account for 20% of the country’s power generation mix.

Granted, that may be lower than its 37.1% share in 2019, but it is nonetheless an essential piece of the energy puzzle in one of the world’s largest markets.

“There is uncertainty as we build out renewables, and as the aging coal plants and aging gas plants combine with the nuclear situation in Japan, that creates a lot of ambiguity about the supply-demand balance on a month-to-month, season-to-season basis,” said Westby.

“And therefore, we’re likely to see demand fluctuations, where we go from periods where there’s huge demand and a lot of stress in the market, to periods where that demand disappears.

“So, therefore, at JERA we think the way to deal with this is through developing more agile procurement policies, and the long-term model is needed, and it definitely is needed to underpin future investment in the gas market.

“But equally, companies need to be able to develop trading capabilities, trading skill sets in order to manage the uncertainties that are coming their way.”

With oversupply and decarbonisation the main headwinds now facing the industry, the evolution of LNG from here will be fascinating to watch.

Listen to the podcast version here

Read our latest issue of Trade Finance Talks, Spring 2022