A new report has found that UK exports could take until 2023 to return to pre-pandemic levels, leaving Britain playing catch-up to other G7 economies such as Germany.

In its latest Global Trade Report, trade credit insurer Euler Hermes forecasts that UK exports will rise by £55 billion (5.6%) in volume in 2022, but will remain below pre-pandemic levels until 2023.

The report also forecasts that next year’s growth will come on top of an expected £18 billion increase in 2021, although these gains will be offset by a £100 billion trade loss in 2020.

Among the UK’s biggest winners, Euler expects the UK’s services (£30 billion) and automotive manufacturing (£3.4 billion) sectors to see the strongest growth, driven by rising exports to the US, Germany, and Ireland.

Ana Boata, head of economic research at Euler Hermes, said: “The UK’s export growth will be welcomed by beleaguered British businesses, but Brexit’s stifling effects will continue to stymy what should have been an even healthier recovery next year.

“Currently, 20% of current delays in suppliers’ delivery times could be explained by Brexit, with the rest attributable to global bottlenecks.

“Those hoping 2022 is the year exporters see out the disruption wreaked by COVID-19 will be disappointed – we don’t anticipate trade will recover to its pre-pandemic levels until 2023 at the earliest.”

The global outlook

Among its more positive findings, Euler forecasts that global trade volume will grow by 5.4% in 2022 and 4% in 2023.

However, the report also warned that global supply chain disruption is likely to remain high until the second half of 2022, exacerbated by a tug-of-war between China, the US, and Europe over inputs.

When it comes to inputs from China, Euler found that Europe is losing that tug-of-war against the US, and that proposed solutions such as reshoring remain “more talk than walk”.

And with renewed COVID-19 outbreaks around the world, combined with China’s continued zero-COVID-19 policy, this dynamic is likely to continue, albeit with added demand and logistical volatility during Chinese New Year 2022.

Françoise Huang, senior economist for Asia-Pacific at Euler Hermes, said: “The US will register record-high trade deficits of around $1.3 trillion in 2022-2023, mirrored by a record-high trade surplus in China ($760 billion on average).

“Meanwhile, the Eurozone will also see a higher-than-average surplus of around $330 billion.”

Supply and demand

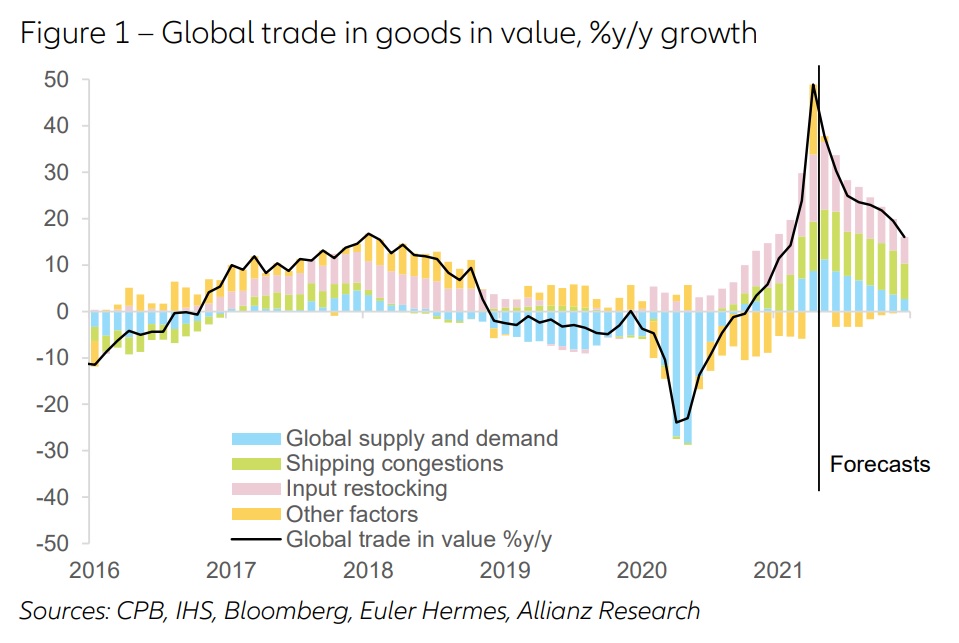

After a strong performance since H2 2020, the report found that global goods trade contracted in Q3 2021, especially in advanced and emerging economies.

However, Euler’s research also found that advanced economies are suffering more from supply chain bottlenecks than from trouble with demand.

For example, production shortfalls were found to be the cause of 75% of the current contraction in global trade volume, with the rest explained by transport delays.

Protectionism also reached a record high in 2021, and is expected to remain elevated, mainly in the form of non-tariff trade barriers (e.g. subsidies, industrial policies).

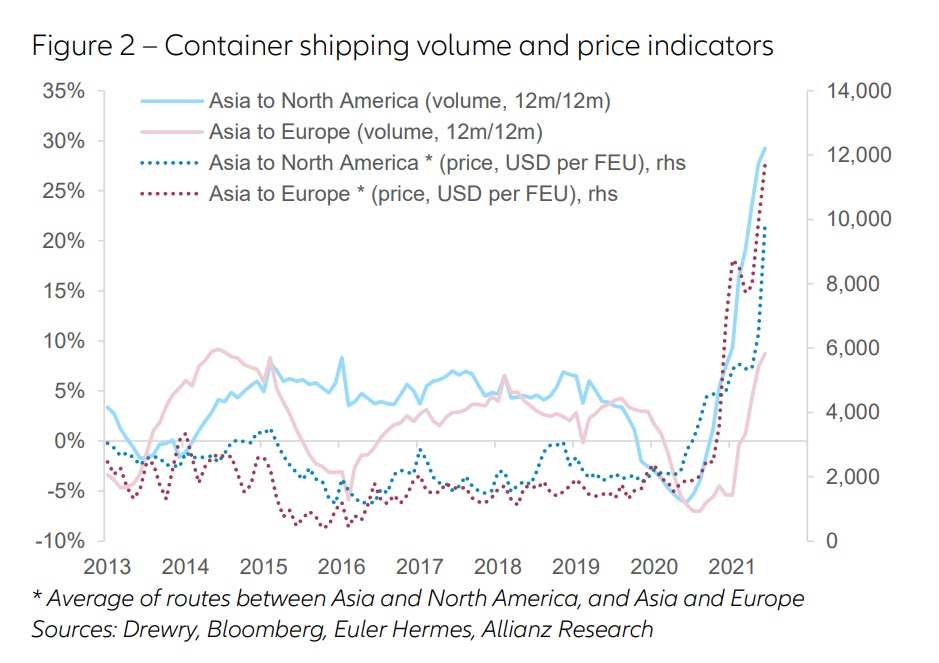

Solving logistics issues

Looking ahead, Euler believes that rapidly growing orders for new transportation capacity (6.4% of the existing fleet) should turn operational towards the end of 2022.

This will also coincide with increased spending on port infrastructure in the US, which should significantly ease global shipping bottlenecks.

Europe is more at risk compared to the US when it comes to the heavy reliance on intermediate inputs from abroad, the report found.

Without production capacity increases and investments in port infrastructure, the normalisation of supply bottlenecks in Europe could be delayed beyond 2022, if demand remains above supply capacity.

Euler also found that, in such a scenario, the household equipment, consumer electronics, automotive, and machinery and equipment sectors are most vulnerable to input shortages.

Ano Kuhanathan, senior sector advisor at Euler Hermes, said: “China is a key downside risk for Europe.

“We estimate that a 10% drop in EU imports from China could be a drag of more than -6% on the metal sector, more than -3% on the automotive sector (incl. transport equipment), and more than -1% on computer and electronics.”

The winners

While there is a risk of a double-dip in Q1 2022, Euler expects a normalisation of international trade flows in volume from H2 2022, driven by three factors:

- A cooling down of consumer spending on durable goods, given their longer replacement cycle and the shift towards more sustainable consumption behaviors

- Less acute input shortages as inventories have returned to or even exceeded pre-crisis levels in most sectors, and capex has increased (mainly in the US)

- Reduced shipping congestions (global orders for new container ships have reached record highs over the past few months, amounting to 6.4% of the existing fleet) and the planned $17 billion spending on port infrastructure in the US

Euler estimates that the energy, electronics, and machinery & equipment sectors should continue to outperform in 2022.

But the main export winner globally in 2023 should be automotive, thanks to the backlog of work and lower capital expenditure in 2021.

At the regional level, Asia-Pacific should continue to be the main export winner in the coming few years, with over $3 trillion in export gains in 2021-2023.