Estimated reading time: 5 minutes

“Life is really simple, but we insist on making it complicated”

Confucius

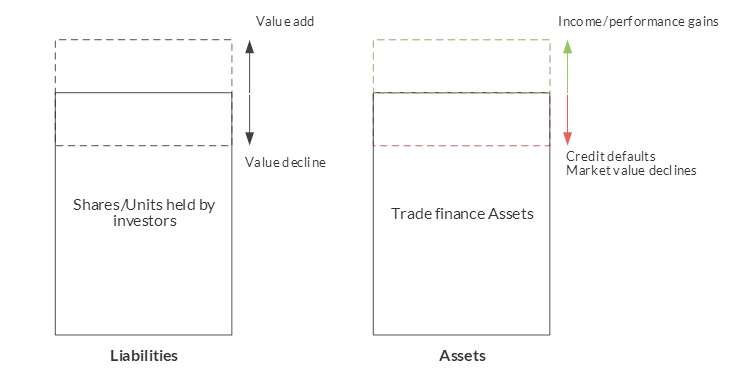

A typical fund structure uses proceeds from shareholder subscriptions to invest in a diverse pool of assets. A fund generally cannot default if it has no debt obligations but rather will experience changes in its total return or net asset value available to fund shareholders (the investors).

Example balance sheet of a traditional trade finance fund

Source: Fitch Ratings

Fitch rates Trade Finance Funds under its bond fund criteria. A bond fund rating gives investors an informed opinion on the likelihood they may experience losses in their investment. This opinion is based on Fitch’s assessment of the credit and market risks inherent in the pool of assets and is represented on two distinct rating scales.

Bond fund Credit Quality Ratings provide an opinion as to the overall credit profile and vulnerability to losses as a result of defaults within a fixed-income fund. These ratings are denoted with an ‘f’ suffix to provide clear differentiation from credit ratings assigned to debt instruments.

Bond fund Market Risk Sensitivity Ratings, expressed on a scale of ‘S1’ (very low sensitivity to market risk) to ‘S6’ (very high sensitivity to market risk), provide Fitch’s opinion as to the sensitivity of a portfolio’s total return or net asset value to changes in interest rate, credit spread and currency risks, considering the effects of leverage or hedging, where applicable.

What investors want to know about bond fund ratings

| Consideration | Bond Funds Ratings |

| Rating Scale(s) | ‘AAA’ to ‘D’ and ‘S1’ to ‘S6’ |

| Rating Suffix | f |

| Summary Rating Definition | A fund’s overall credit profile and vulnerability to losses as a result of defaults (Fund Credit Quality Rating) and fund’s relative sensitivity to changes in interest rate, credit spread and currency risks (Fund Market Risk Sensitivity Rating). |

| Does Rating Address Credit Risk? | Yes (via Fund Credit Quality Rating) |

| Does Rating Address Market Risk? | Yes (via Fund Market Risk Sensitivity Rating) |

| Does Rating Address Liquidity/Redemption Risk? | No |

| Typical Rating Range | Full rating spectrum |

| Credit Risk Scoring Approach | Weighted average rating factor |

| Credit Risk Scoring Time Horizon | Full time horizon, in increments ranging from 90 days to three-plus years. |

| Market Risk Scoring Approach | Interest rate duration plus risk-adjusted spread duration, adjusted for unhedged currency exposure and leverage. |

| Consideration of Asset Manager Capabilities | Yes |

| Applicable Regulatory Frameworks | No specific regulation, but may be subject to broader mutual fund regulations, such as the UCITs or AIFM directives in Europe. |

Trade finance funds have many attributes akin to traditional bond funds. However, certain features are unique and led to additional analytical considerations being introduced to Fitch’s Bond Fund Rating Criteria. Specifically, the use of trade credit insurance, exposure to unrated subsidiaries of rated entities and investments in structured notes backed by trade finance assets are now addressed in our criteria.

Summary of criteria introduced for trade finance funds

| Trade Finance Fund Feature | Fitch’s Criteria |

| Use of Trade Credit Insurance | For a given exposure covered by trade credit insurance, Fitch will recognise the protection provided by an insurer (via an Insurer Financial Strength rating) to determine the exposure’s credit rating factor, subject to a qualitative review of policy terms and other conditions that can affect the enforceability of the insurance contract. For the insured portion of an exposure Fitch will add the expected timing for a claim pay-out to the maturity date to reflect the additional market risk sensitivity of the insured exposure. |

| Exposure to Unrated Subsidiaries of Rated Entities | Notch down three notches from the parent rating, provided the parent is rated by an external credit assessment institution, the subsidiary is at least 75% owned by the parent and the parent and subsidiary have shared branding. |

| Investment in Structured Notes Backed by Trade Finance Assets | Look through the structure to the underlying trade finance assets/obligors, subject to satisfactory review of documentation addressing whether the economic gains and losses of the underlying assets are effectively transferred to the fund through the note (i.e. the note cannot default, but rather can only experience changes in value equivalent to the net asset value of the assets backing the transaction). |

The Asian Development Bank estimates that the global gap in trade finance is $1.7 trillion. This represents the amount of trade finance that has been requested by importers and exporters but rejected.

The very large trade finance funding gap has created an opportunity for the growing number of institutional investors drawn to the asset class. Trade finance funds are seen as a vehicle that can provide access to this wider group of investors, but education on the risks faced by investing in these funds and ‘keeping it simple’ are critical.