Estimated reading time: 7 minutes

Dubai’s undeniable growth in trade, logistics and the financing of international commerce has made it one of the most desirable trade destinations in the world. This is why I invested more time with members of the ITFA Middle East committee in 2022.

Given the strong regional appetite for advanced technologies, we established the Middle East Tradetech Adoption Group to drive collaborative work on the digital negotiable instruments (DNI) Initiative, the TFD Initiative and other advanced innovations.

During the MENA conference panel, industry leaders shared the progress achieved on the DNI Initiative, i.e., aiming to adopt MLETR in order to digitise negotiable instruments across transport, logistics and banking.

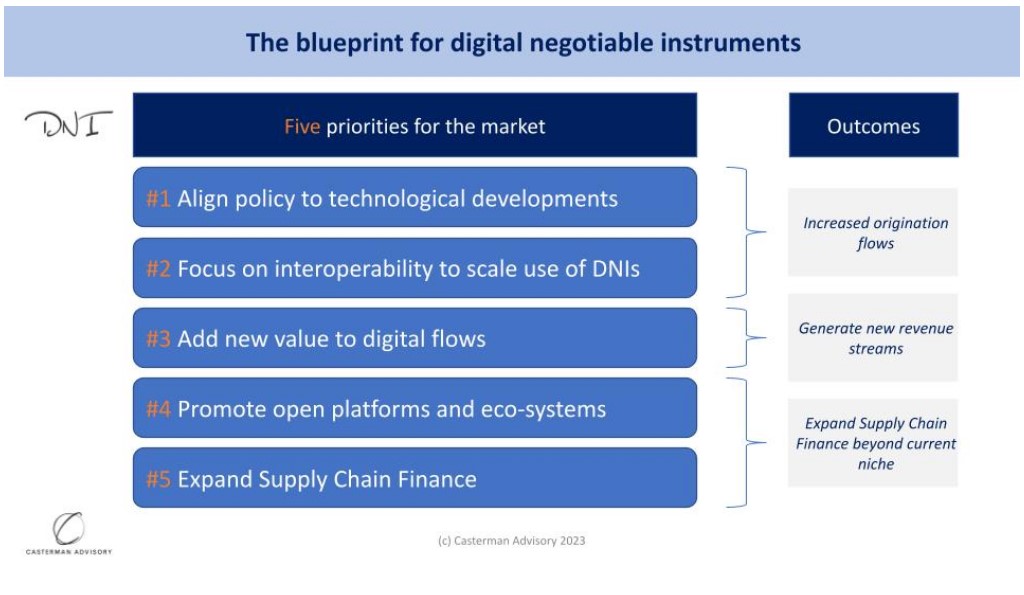

On stage, members of the new tradetech group (as listed in the above image) reported on market dynamics related to MLETR and their recent pilot transactions. We debated the blueprint for digital negotiable instruments and shared five priorities.

1. Align policy to technological developments

DNIs require adapting national laws to deal with new technologies, aiming at upgrading existing logistics, trade and trade finance processes. Middle Eastern policymakers have promptly embraced MLETR since its publication in 2017 and delivered two of the initial jurisdictions – Bahrain (2019) and ADGM (2021) – which are ready to embrace the use – and enforce the legality – of electronic transferable records.

Amr El Haddad, head of working capital solutions CEEMEA, Kyriba said, “With the fragility of supply chains, inflation, and the geopolitical risks, world trade has never been more exposed, and subsequently, the need for more and better technology has never been clearer.”

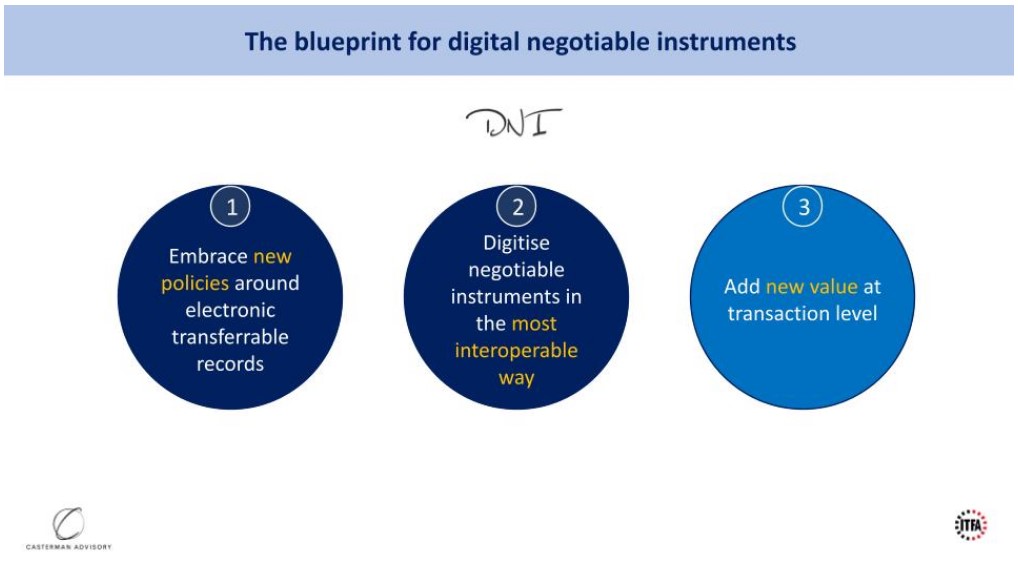

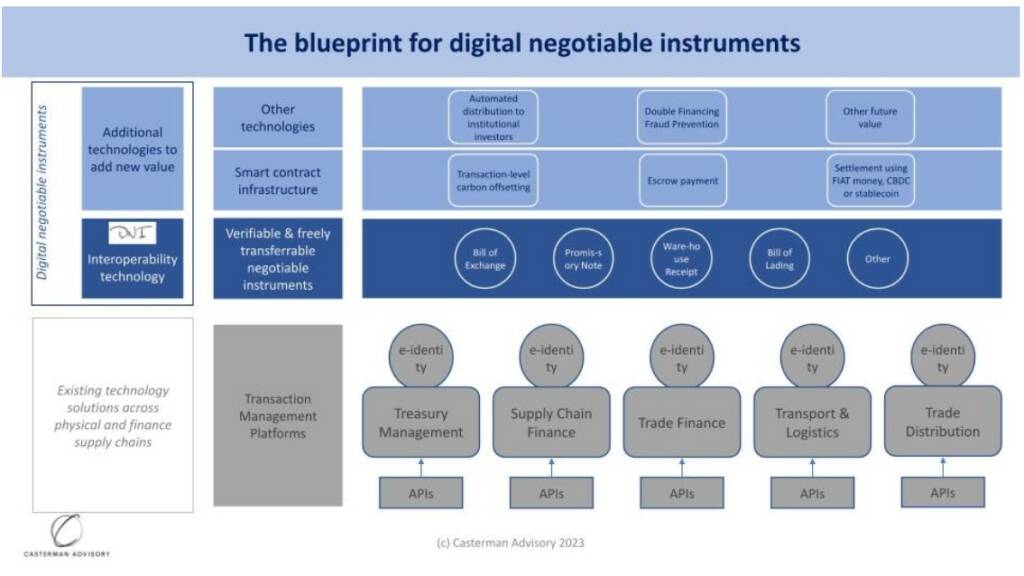

As illustrated in the below chart, the priorities are

- To align national laws with MLETR to ensure electronic negotiable instruments are legally enforceable

- To implement interoperable technologies

- Once those two steps are completed, adding new value may be prioritised.

Vishnu Purohit, group head of trade product management, Emirates NBD, said, “We piloted the DNI Initiative and validated that the additional MLETR technology is pretty simple to use. The impact on business practices is minimal, which is a major benefit.”

2. Focus on interoperability to scale the use of the new practice

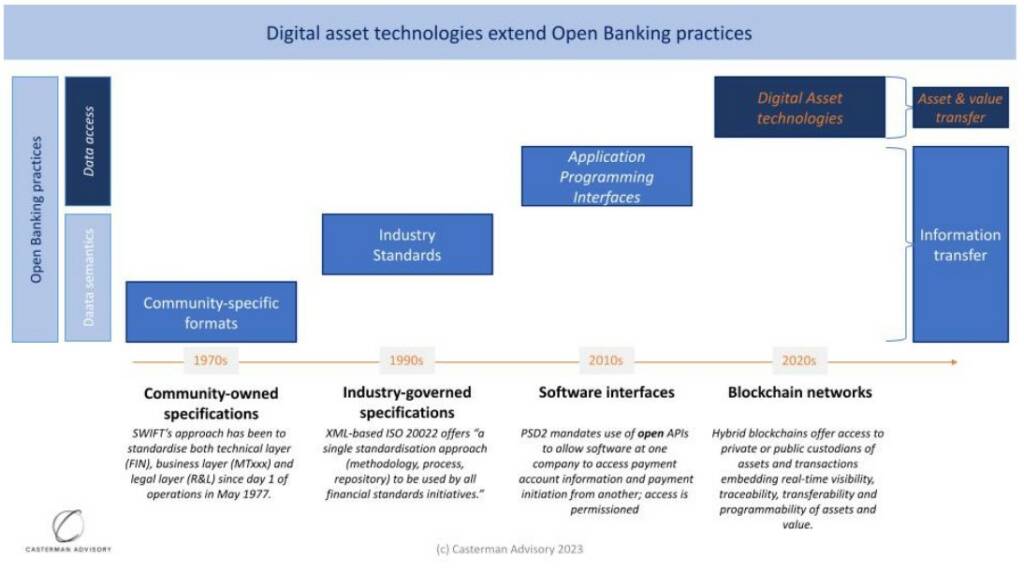

The emergence of distributed ledger technology (DLT) and “digital assets” extend Open Banking practices with “asset and value transfer”. This capability is particularly suited to achieve the level of interoperability required for title documents such as negotiable instruments. In other words, cloud platforms and APIs are not sufficient on their own.

A member of the Middle East Tradetech Adoption group said, “We witness great appetite from various jurisdictions to embrace advanced technologies such as DLT, as policymakers want to help the market benefit from new digital options. MLETR is no exception and everyone will benefit.”

Embracing interoperable technologies, as proposed by DNI Initiative’s dDOC specifications, enables the market to scale the use of MLETR-compatible instruments before more value can be added.

3. Add new value to digital flows

As the adoption of e-negotiable instruments scales, the next opportunity for the market is to add more value to those enforceable electronic records.

Four examples include:

- Automated securitisation for the sale of assets to institutional investors

- Programmable transaction-level carbon offsetting

- Escrow payment and instant settlement

- Double financing fraud prevention and more to be developed by the market.

Those features are critical to extending further benefits such as increasing balance sheet velocity, achieving net zero, and mitigating credit, operational and fraud risks, as proposed by the below chart.

Sean Bowey, head of products, global trade & receivables finance, SABB said, “We are witnessing strong appetite from the Saudi policymakers to embrace MLETR, and have established a continuous dialogue on the way forward, with the support of UNCITRAL.”

4. Promote open platforms and eco-systems

Treasury management systems, supply chain finance, traditional trade finance, transport & logistics and trade distribution platforms are specialised software solutions which have proven – and will continue to prove – their value.

However, one typical issue with most of them is that they operate as closed ecosystems. Closed ecosystems worked in the previous eras, but trade is trending towards an open ecosystem.

André Casterman, ITFA & DNI Initiative, said, “DLT is a 21st-century innovation that needs to be embraced with a 21st-century open banking mindset; that’s where most trade-focused consortia have failed so far (not only the bankrupt ones).”

Interoperability comes in different forms, and in the area of DNIs, platforms that embed the DNI Initiative’s dDOC specifications become focused on the instrument level.

This means the trust is embedded in the electronic record that represents the negotiable instrument (with the associated verifiable token written on a public blockchain).

This also means each party can use separate software solutions and channels. With such a level of interoperability, the issue of closed ecosystems will finally be solved.

As indicated in dark blue on the above chart, the interoperable negotiable instruments represent payment obligations such as bills of exchange (BoE), bills of lading (BL), and promissory notes and can navigate from one platform to another as self-contained and verifiable “digital assets” (as per DNI Initiative’s dDOC specifications).

The light blue layers outline additional features that can be operated either on-chain, such as automated transaction-level carbon offsetting, with an escrow payment, and on-chain settlement. They can also be operated on the basis of dedicated technologies/legal schemes for automated repackaging, fraud prevention and other types of value-added processing.

5. Expand Supply Chain Finance

Corporate clients active at the international level love the BoE used under English common law, as it provides extended credit from a seller to a buyer across multiple jurisdictions.

The most common use case for a BoE is when a seller operates across multiple jurisdictions. Given the long experience of the corporate market with this instrument, it provides a comfortable solution.

Other supply chain finance programmes, like Irrevocable Payment Undertakings (IPUs), require additional paperwork. BoEs simplify the process, as there is no need for additional documentation for buyers to review. Additionally, BoEs are not characterised as bank debt, unlike IPUs, which have accounting implications. In other words, the IPUs present a risk of re-classification, whereas the BoE shields corporates from such risk.

Vishnu Purohit said, “Digital Bill of Exchange auto-embedded in a supply chain payable workflow can potentially replace proprietary payment service agreements.”