In a world of shrinking supply chains and digital connectivity, the concept of identity is continuously evolving. Is digital identity going to be the panacea to the age-old problem of MSME (micro, small, and medium enterprises) access to trade finance?

What is Identity?

The Oxford English dictionary defines identity as “the fact of being who or what a person or thing is” and has its origins dating back to around the 16th century from the Latin word Idem meaning “The same”. However, in the financial world, recognizing an individual is a fundamental requirement both from a risk and fraud prevention perspective with the significant effort being spent on the KYC/CDD (Know Your Customer)/(Customer Due Diligence).

According to the Financial Action Task Force’s (FATF) Digital Identity Guidelines, identity is a complex topic with many meanings. For financial services, one should restrict the definition to the official identity and not mix it with the broader concepts of social and personal identity.

Taxonomy of Identification

Individual’s Identity

While the concept of identity for an individual is synonymous with an ID (Identification Document), a physical document, which in most countries ranges from passport to driving license or other government-issued documents. To trace back in history, the first documented version of a passport was instituted by King Henry V of England in 1414 and has ever since been a critical document that identifies an individual in an international location. It remained so for the next 500 years and only since the advent of the internet in the late 1980’s did these physical IDs started getting digitized and moved towards truly digital IDs.

Though moving from physical to digitized ID did help bring in marginal efficiencies, a giant leap is being witnessed by moving to digital IDs. While developed nations had the advantage of digitizing their records, emerging markets leapfrogged with the help of digital IDs.

Corporate’s Identity

Similar to the concept of individual identity, it is important to establish the identity of a corporation. The most used identity is LEI – Legal Entity Identifier which is accredited by the Global Legal Entity Identifier Foundation (GLEIF).

After the 2008 financial crisis, the G20 developed the LEI system to provide the ability to financial institutions to uniquely identify organizations and track their financial transactions across different jurisdictions. The LEI is a 20-character, alphanumeric code based on the ISO17442 standard and helps in answering the question of “who is who” and “who owns whom”.

What is Digital Identity?

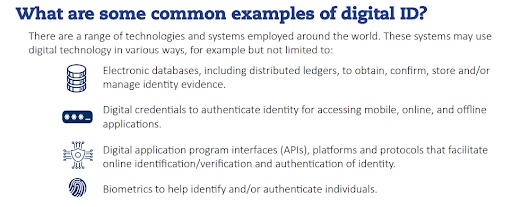

According to FATF Guidance on digital ID, Digital ID is the use of technology in asserting and providing identity. This definition further elaborates that not all the elements of a digital ID system are necessarily digital. Some elements of identity proofing and enrolment component can be either digital or physical or a combination, but binding, credentialing, authentication, and portability/federation (where applicable) must be digital.

The need for Digital Identity in trade finance

Lack of identity creates a big obstacle to accessing financial services. This is especially true in trade finance where the buyer and seller are in different countries and relying on their local financial institutions for working capital requirements. Along with the KYC/CDD related requirements, Anti-money Laundering (AML) and Combating the Financing of Terrorism (CTF) are potential areas where banks need to focus since non-adherence can lead to heavy fines and reputational loss. Digital IDs can help significantly reduce the turnaround time for a bank to complete their KYC process.

Financing Gap for MSMEs

Today, global trade faces a $3.4 trillion financing gap. This figure has skyrocketed due to the pandemic-related disruption across the global economy. This gap is exacerbated for MSMEs with an almost 45% rejection rate for trade finance. As per many reports from WTO and ICC, the international trade is dominated by large players and only 10% of the trade comes from organizations with 0 to 9 employees. Another study by IFC and World Bank’s research unit in the developing economies identified that the finance gap from the formal MSMEs is $5.2 trillion, almost 19% of the gross domestic product (GDP) of those economies.

One of the biggest hindrances that MSMEs face in accessing the trade finance from banks is due to the high cost of conducting KYC in absence of a uniquely identifiable source for their identity. The ADB Trade finance gap survey indicates that almost 1 in 5 of MSME get their KYC/AML rejected by banks. This problem increases in emerging markets and radical solutions such as digital identity networks can bridge the gap.

Who is driving the adoption of digital IDs?

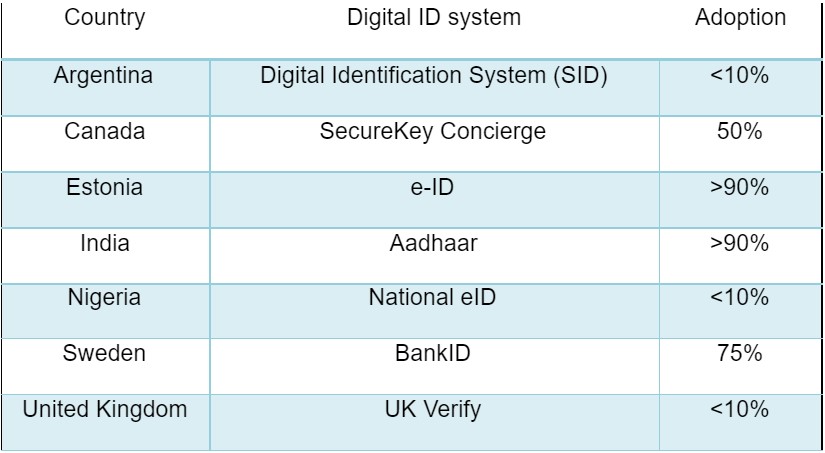

- Governments: Around the globe, governments are driving the agenda of digital identity. With help from initiatives like the Identification for Development (ID4D), member states of the United Nations (UN) have adopted Sustainable Development Goal (SDG) Target 16.9: “to provide legal identity for all, including birth registration by 2030”. Apart from UN, several individual countries are also rolling out their own digital ID initiatives. These are summarized in the following table.

- Banks: Financial institutions can help in driving the digital ID adoption through policy changes that mandate their use by clients. With more clients using digital IDs, the identity framework will grow stronger in the market and thereby bring down the cost of adoption by the third-party service providers. A successful example of a bank driving digital ID adoption is BankID Norway, a very popular mobile application in the Nordics.

- Fintech: With the advent of fintech in supply chain financing, there are several players who are directly or indirectly solving the problem of verifying the identity of a buyer/seller. The advantage that fintechs have over banks is greater access to data. In the industry, this concept is called the “thin credit file” – where one does not have enough credit information. Compare this to a situation where in countries like India, China, and the USA, where large number of SMEs operate on platforms like Flipkart, Alibaba, and Amazon. These portals have vast amount of information and linkage on the buyer/seller profile. When combined with financial information data, this is a gold mine of information to perform credit worthiness and KYC checks. Fintech and financial institution collaboration will be key to the success of profiling clients and creating their “behavioral” identity. Fintech also operate as an intermediary between the buyer and supplier through blockchain-based solutions and eliminating the need of intermediaries.

Opportunities and Benefits of Digital Identity

The major benefit of a digital identity for MSMEs, especially in the emerging markets, is that it helps improve financial inclusion, bridging the trade finance gap. It will also reduce the KYC/CDD costs for the financial institutions which in turn helps corporates receive better credit terms. Other benefits include the reduction in human errors for document checking during the KYC process as well as better linkage of entities across the supply chain system during AML checks.

Banks can provide a better product offering clients based on their dynamic identity rather than the static identity. It also brings in transparency for clients who know when and what information is being shared with the banks. And finally, convenience, as digital identity helps connect the buyers, suppliers, and other third parties with ease and efficiency.

Challenges with a Digital Identity

Even though the benefits of technological solutions are helping to reduce the cost for banks to engage with MSMEs, there are still several challenges.

- Fragmentation of current initiatives: Multiple initiatives aimed across geographies and lifecycle of the trade creates a challenging environment for any critical mass to form where all the parties can take advantage of the digital identity.

- Lack of Interoperability: Emergence of different platforms involving exporting and importing parties, banks, shipping agencies, customs duty etc. and these are not interoperable leading to a fragmented adoption that lacks scale.

- Digital Islands: The fragmentation of initiatives has created digital islands. A lack of interconnectedness across different solutions has created a major bottleneck with some exporters dealing with dozens of platforms.

- Technology Risks: With more and more dependence on technology, the inherent risks such as cyber risk and machine errors must be considered. For MSMEs this would be an additional financial burden. Given that authentication is required over the internet, it does involve requisite measures for identity proofing.

- Cost of Adaptation: MSMEs need to have a separate budget carved out for technology adaptation and at times the lack of trade-as-a-service plug-and-play solutions creates an entry barrier for MSMEs.

- Harmonized Corporate Digital IDs: Given the complexity of corporate digital IDs to deal with the ownership structures and lack of uniform global solution, an additional challenge exists as companies exchange data across borders.

Conclusion

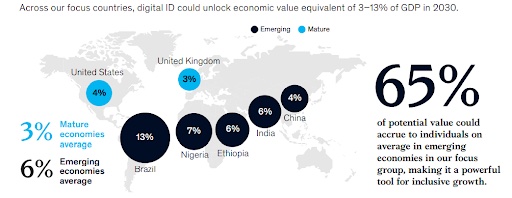

Digital identity is changing the trade landscape. Whether it takes the form of the LEI or other digital identification networks, digital identities are here to stay. This will help bridge the trade finance gap providing underserved MSMEs in emerging markets better access to finance by improving efficiency in banking operations and compliance functions. The next few years will see various ecosystems building and merging towards the large ones and fueled by the growing Fintech and government initiatives like the ID4D with the potential of unlocking economic value equivalent of 3-13% of GDP by 2030.