We heard from Bolero’s Jacco de Jong at the BCR Supply Chain forum in London. Bolero has a vision for trade digitisation. Bolero is about connecting parties, banks and networks in trade, established from an EU initiative by Swift and TT Club. From a supply chain perspective, Bolero has a web-based platform with a legal framework and standards which provides e-Presentation, eBills of Lading, guarantees and supply chain, connecting the physical supply chain with the financial supply chain.

How does SCF work in terms of digitalisation?

Supply chain finance helps large corporates work with their suppliers to offer better financing terms to their suppliers. Typically, buyers have long payment terms, and speeding up the working capital cycle for suppliers helps make their processes more efficient.

How does it work in practice?

- A buyer such as Nike would upload approved purchase orders into an electronic system multiple times a day, notifying suppliers that these have been uploaded

- The supplier ships the goods and produces an invoice and advanced shipment notice which matches with the purchase order (PO)

- The system automatically matches this invoice against the purchase order through AI and logic matching processes

- When the supplier uploads this information, they can also request for financing on these goods, which automatically goes to a bank or financier, which then uses criteria to accept and provide financing to the supplier

This process, known as reverse factoring, helps finance smaller suppliers of numerous sizes.

However, matching a P.O. with an invoice is key to advancing payment making it easier for suppliers to get paid even before they ship their goods to their buyers. From a purchase order perspective, advancing finance at this level is much more attractive for a supplier rather than at the invoice factoring level. Financing could happen at the point at which goods are loaded onto a ship or have left the suppliers warehouse. This is where using a Bill of Lading (BOL) as security to provide pre-export finance could come in handy. Electronic Bills of Lading (eBOLs) can be used as a pledge to a bank, proving to a bank that there is security and title of the goods to a bank, both of which help reduce default risks from a bank’s perspective.

eBOLs is key to digitalisation, and largely not accepted in Europe and the US. That said, the acceptance of eBOLs in Asia and Australia is wide, so the adoption in other markets is key, and implementation through local law is key. The ICC is also shifting and revising it’s international rules around UCP600 and URDG guidelines which will help accelerate the adoption of eBOLs into local law.

Because POs can be changed over time, it’s often challenging to finance against this, therefore if the PO is not revocable, commercial disputes could arise if the contract is cancelled or the order is changed, and financing is provided on the basis of that PO.

The reconciliation of POs with invoices is one of the biggest challenges when it comes to advancing payment on POs rather than invoices. Systems such as Bolero use data matching and AI, as well as over 14 years of data to help expand the functionality and accuracy of Me-PO.

The journey to digitalisation is hard, however. Collaboration and partnerships with banks, KYC software products, and this takes time. As change continues, the move to paperless and appetite to digitalise will continue to accelerate and companies will need to work together to achieve this.

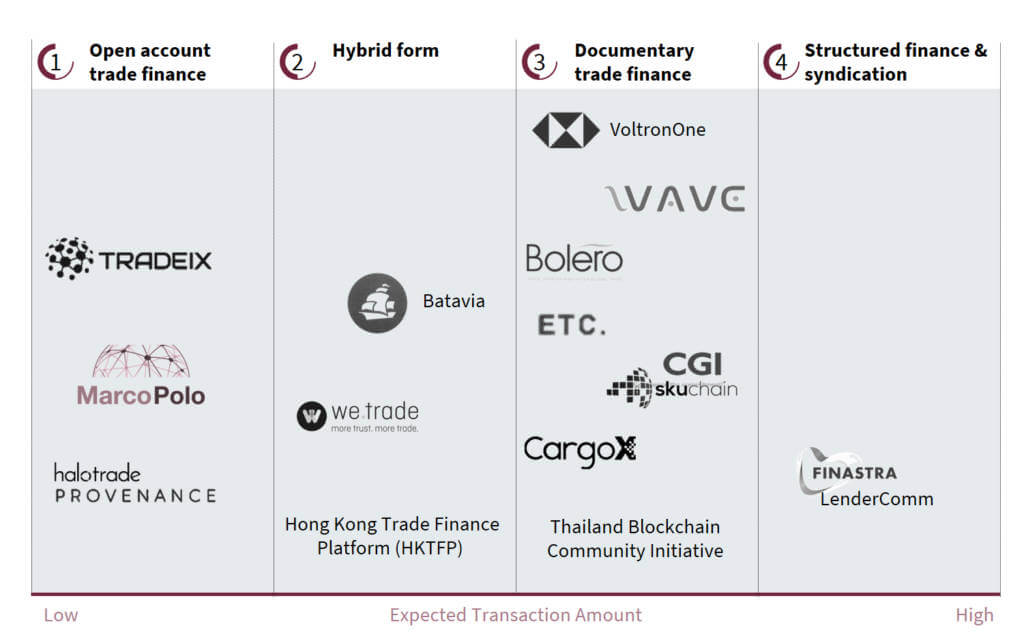

Who are the big players in digitisation of trade and supply chain finance?

We found a schematic of the big new entrants here:

Find out more about Supply Chain Finance and what Trade Finance Global can do to help assist your SCF needs here.