-

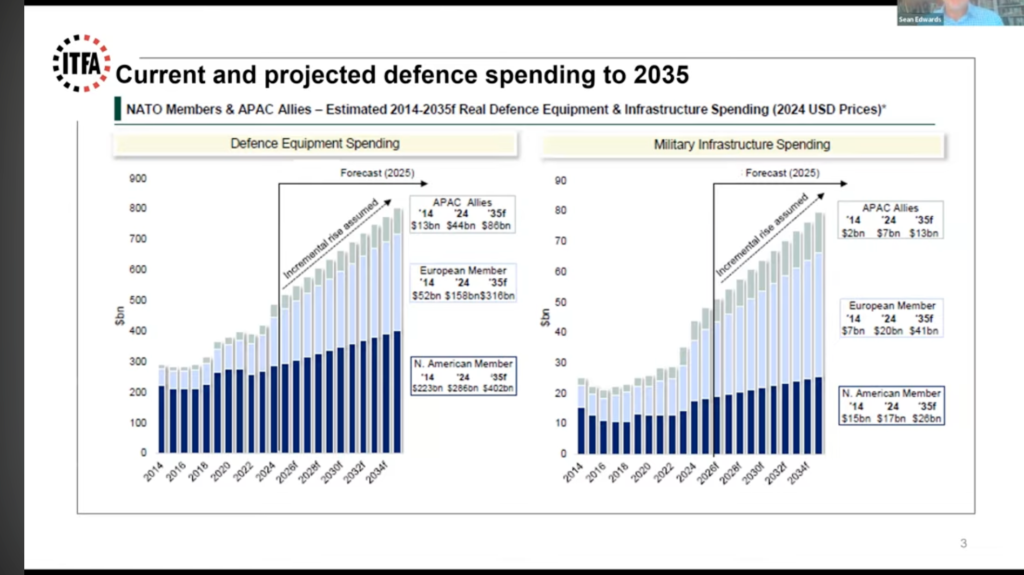

European nations are projected to increase annual spending on defence equipment by over 500% between 2014 and 2035 to reach a total of $316 billion.

-

The traditional procurement model led by ‘prime’ contractors is being challenged by specialized tech start-ups that require earlier access to liquidity than standard supply chain finance provides.

-

To bolster regional resilience, the European Commission is prioritizing keeping defence spending within Europe, often requiring non-European suppliers to localise their operations.

By 2035, European states will spend $316 billion annually on defence equipment, marking an over 500% increase from 2014 levels, according to projections by the International Trade and Forfeiting Association (ITFA).

Defence production across Europe is already strained due to the war in Ukraine. A ramp-up of the proposed scale is unprecedented, and Europe requires a rapid and radical transformation of infrastructure, inventory, and technology.

In the second episode of ITFA’s webinar series on Funding European Security, Sean Edwards, Chairman of ITFA, hosted Tom Dunn, Chairman at Orbian; Katherine Earl, Head of Trade and Working Capital Sales at Citibank; Steve Jackman, Principal at Efficio; and Vincent Giboin, Global Trade Sales Lead: Industrials, Defence & Natural Resources at Santander Corporate and Investment Banking (CIB).

They discussed the role of trade, supply chain finance (SCF), and innovative financing solutions in scaling Europe’s defence capacity.

Supply chains for peace and war

Defence spending, as a system, is highly capital-intensive and politically sensitive, requiring secrecy around supply chain contracts. For decades, Western governments have relied on ‘primes’ as a procurement strategy.

‘Primes’, also known as prime defence contractors, are major military providers with a direct contractual relationship with governments, including Lockheed Martin, BAE Systems, Boeing, and Northrop Grumman.

Primes are brokered between tier 2 and tier 3 suppliers, usually small and medium-sized enterprises (SMEs) and governments, picking up financial and supply chain slack, and taking on responsibility for increasing capacity.

But this system has significant risks. The first is that a concentrated distribution setup can undermine supply chain resilience.

The second, more crucial aspect is that secrecy leads to a lack of visibility over tier 2 and tier 3 suppliers, where tier 3 suppliers may have contracts with a huge variety of tier 2 and, in turn, tier 1.

When crunch time comes, if everyone has to ramp up production at the same time, tier 3 capacity becomes constrained; tier 3 cannot fulfil all tier 2 orders, which, ultimately, impacts tier 1 output.

Jackman said this has put companies onto a “charm offensive,” each vying to ensure they are the company that suppliers maintain relations with, if and when supply disruptions occur.

However, new technology is shifting this procurement hierarchy. Growing markets, including drones, technology, and ammunition, have led to an increase in SME specialists with contracts directly with governments, explained Gilboin.

According to Earl, this is particularly true for specialised tech industries, including in cyber security and artificial intelligence (AI), where industry start-ups have accelerated development faster than conglomerates.

These start-ups, though scaling quickly, lack the balance sheet and liquidity capacity of primes, which is a problem given lengthy government procurement cycles.

Earl noted that the drawn-out process and delays in government decision-making, coupled with changing political priorities that mirror election cycles, leave little room for companies to make long-term plans, let alone scale them effectively across the supply chain.

Beyond asking governments to make long-term commitments to their defence procurement cycles, building supply-chain resilience into the procurement process relies on access to financing.

“We have a supply chain that has effectively been developed in peacetime for peacetime. We are now not in peacetime,” said Jackman, pointing to how the changing geopolitical landscape means existing systems for defence supply chains are no longer effective.

Innovative financing strategies for defence

Shifting supply chain demands, driven by geopolitics, mean the European Union (EU) must come up with innovative strategies that aid the current climate’s needs.

SCF, a cash flow solution that unlocks working capital, enables suppliers with weaker credit ratings to leverage their customers’ stronger credit ratings.

“However, supply chain financing only really kicks in once manufacturing has been completed and invoices have been issued,” explained Earl.

Scaling rapidly, particularly in wartime, requires access to liquidity earlier in the process. For Earl, there are three other financing products suitable for defence contractors:

- Purchase order financing, which provides liquidity access where companies manufacture goods before they can issue invoices, perhaps due to stringent testing requirements or security protocols.

- Inventory financing, which can enable suppliers to stockpile materials, including chips and rare-earth minerals, to avoid supply chain disruptions.

- Capital expenditure (CapEx), a necessary part of infrastructure upgrading, as companies may require new factories, tools, software, and technologies to meet changing supply chain demands.

Multilateral development banks (MDBs) also play a crucial role in enabling risk-sharing, particularly through partnerships with banks to enable blended finance agreements.

The European Investment Bank (EIB) recently signed an agreement which combined EIB-backing with bank distribution capacity, enabling institutions to channel liquidity across the defence ecosystem.

Export credit agencies (ECAs) are also moving away from transaction-by-transaction support. Giboin explained that ECAs have shifted toward a guarantee of receivables, combined with bank financing, extended across multiple suppliers and contracts. This funds an ecosystem, rather than providing individual transaction-based support.

“Blended defence is not a ‘nice to have’. It’s the only way to crowd in private liquidity and reach scale,” added Giboin.

It’s not just MDBs and ECAs that are enabling a transformation in defence financing. Increasingly, independent SCF providers, such as Orbian, operate as a point of integration to maximise available funding sources.

These providers can offer financing directly to SMEs, overcoming the administrative constraints and lower credit ratings that often prevent large banks from participating.

Earl noted that non-bank investors tend to seek higher yields than multinational corporations offer, and are therefore willing to take on the high-risk, high-reward nature of SME defence companies.

How to keep the money in Europe

The Trump administration’s tariffs have sent a clear message to European suppliers: do not rely on the US anymore.

Correspondingly, many European nations are looking to direct supply chain spending into Europe.

According to Jackman, sourcing activity has become increasingly sophisticated. Historically, sourcing relied on running a competition within regulation and finding a winning supplier. In contrast, now, there is greater pre-configured engagement with suppliers to end up with the supply chain you need – not just a winning bidder.

For instance, Ukraine builds supply chains to meet demands. Ukraine’s drone supply chain has become so efficient that it isn’t merely sustaining Ukraine at war; it is now exporting drones. This is enabled through low warehouse stocks that enable quick turnarounds for technological innovations and software updates. Resource inventories, in turn, remain high to meet production demands.

In 2025, the European Commission produced a White Paper on defence readiness by 2030, which centred on keeping defence spending ‘in Europe’.

But even where non-European companies are contracted, in particular with South Korean suppliers, Earl emphasised that they are increasingly required to localise in Europe to ensure that the money they spend supports the economy at home.

By using their SME networks to broker prime-SME contracts within Europe, financing platforms can help facilitate defence contracts that require a set percentage of spending to be regional or local, explained Dunn.

Additionally, in a phenomenon coined ‘patriotic capital’, private investors, from individuals to private equity corporates, are looking to invest in defence spending for patriotic, nationalist, and security reasons. However, the capital structures vary hugely across Europe.

Big banks have a critical role to play, too. Global banks that operate across multiple jurisdictions have access to data that suppliers lack, and can determine who else tier 3 is supplying.

Earl highlighted how governments, including those within Europe, are reaching out to banks to find out what can be seen from their data.

—

Scaling up defence supply chains, although may seem necessary for many governments, comes at a cost. Banks and sovereign wealth funds moving toward defence spending means they are shifting away from environmental, social, and governance (ESG) mandates.

ITFA’s projections show that defence spending will steadily increase until 2035 – a year that coincides with many sustainability mandates and carbon-neutral targets.