Trade Finance Global caught up with the Head of Macroeconomic Research, Ana Boata at Euler Hermes last month at The Institute of Export & International Trade’s World Trade Summit. A very interesting macroeconomic view on how households, retail and economic growth has changed in 2019 due to trade wars, Brexit and business uncertainty.

Featuring: Ana Boata, Head of Macroeconomic Research, Euler Hermes

Host: Deepesh Patel, Editor, Trade Finance Global

Deepesh Patel: We have a deal, so what?

Ana Boata: We have argued for a long time that another extension of Article 50 was likely before Oct 31st. And here we are! And we think Article 50 might be again extended before Jan 31st. While having a Brexit deal which has been approved “in principle” by the House of Commons is positive, the procedures to get it fully ratified are likely to be longer than one expects. Indeed, the Brexit bill will be sent to the House of Lords after the general elections and we think this is likely to ask for a series of amendments as 85% of them are pro-EU. Implementation risks to the current version of the deal remain high given the complexity of the dual custom union system in Northern Ireland. In addition, to the change in regime of the trade in goods as custom checks will be set up, financial services would lose the passporting rights. Hence, we would not expect the effective Brexit to happen before the start of 2022. But beyond the Brexit deal what we see most important will be the outcome of the next general elections on Dec 12th. The polls show a very fragmented political landscape and a weak governing coalition as likely. The probability of views switching in the opposite direction (including a second Brexit referendum) after the elections is not negligible as most of MPs are in favor of a Brexit deal which targets a custom union with the EU – something very different from the current version. Hence, the probability of a very soft Brexit/ no Brexit is how higher (30% instead of 10%) while the one of a no deal decreased from 40% to 10%. Our baseline scenario (60%) remains a delivery of Brexit at the latest end of 2020. The lower uncertainty around Brexit is good news as it will help business confidence stabilize while helping investment to bottom-out after two years of contraction. Overall, we estimate the cost of Brexit at more than -0.3pp per year for the UK and around -0.2pp for the Eurozone.

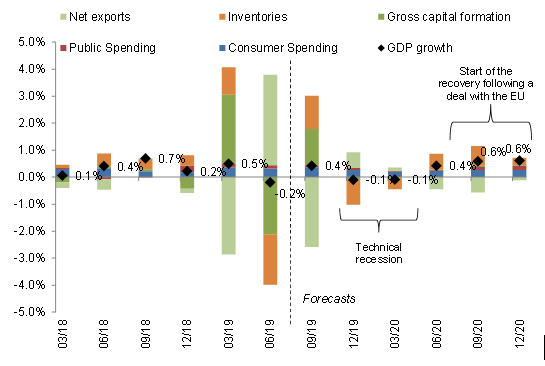

The companies continue to bear the brunt of Brexit

While UK companies suffered from lower margins (-3pp) since the referendum due to higher input prices, accelerating wages due to labor shortages and higher costs related to contingency stockpiling, Brexit will remain a drag until Q1 2020. Q3 GDP data confirmed the downward trend in company prices in order to get rid of the precautionary stocks done since the start of the year to prepare for a no deal Brexit. Overall, GDP grew by +0.3% qoq, -0.1pp below our forecast. Exports in volume have rebounded strongly +5.2% qoq as export prices fell by -4.4% qoq, the strongest decrease since the 2000s. As a consequence, stocks have continued to decrease (-0.9pp to real GDP growth). Overall, net exports have contributed by a strong +1.2pp to real GDP growth as import growth was not as spectacular as in Q1 (+0.8% qoq). As expected households have also purchased goods as a preparation to a no-deal Brexit (+0.4% qoq) while companies have put on hold their investment plans (+0% qoq for business investment). Going forward, we expect two quarters of negative growth (-0.1% q/q) in Q4 2019 and Q1 2020 on the back of frontloading activities due to preparations for a no-deal Brexit.