Clothes

- Global fashion supply chains rely heavily on low-cost labour in countries like Bangladesh and Vietnam, making these economies highly vulnerable to external demand shocks and disruptions.

- Efforts to improve labour conditions, such as higher wages and stricter regulations, can unintentionally lead to factory closures, unemployment, and increased automation.

- Long-term resilience in the garment industry depends on local solutions like economic diversification and better access to finance for suppliers, rather than solely on pressure from international retailers.

“What you don’t know is that that sweater is not just blue, it’s not turquoise, it’s not lapis, it’s actually cerulean.”

Miranda Priestly’s impassioned speech on the complexity of fashion, in the cult classic movie The Devil Wears Prada, is an iconic description of the garment industry’s intricate sourcing system, which, in Priestly’s words, “represents millions of dollars and countless jobs.”

In a world where supply chains mostly hum by unnoticed unless there is a major disruption, few people stop to think of how their steak got on their dinner plate or how many hands a diamond passed through before being set in their engagement ring. In recent years, the fashion supply chain has stood out as a notable exception to this.

With countless scandals about exploitative labour practices, often in South-East Asia, and the subsequent effort by major retailers to show sustainable practices, responsible supply chain management became a major focus of the industry.

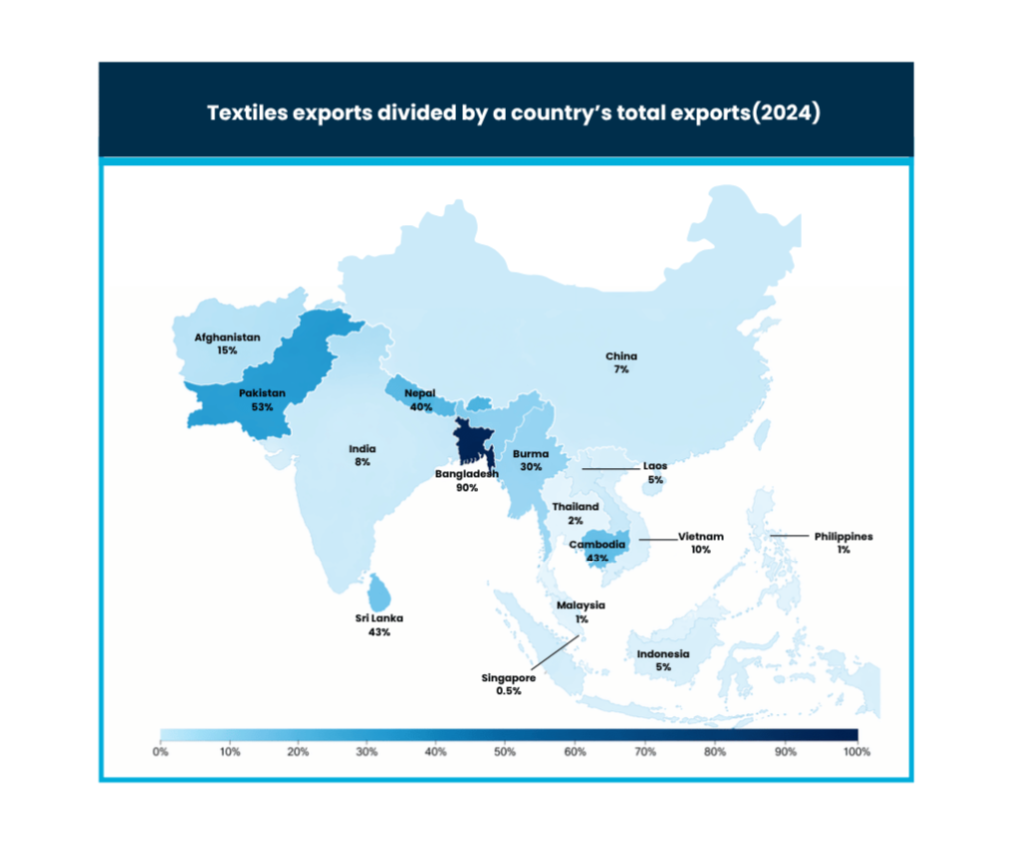

Much like coffee – the subject of last month’s column – the fashion industry’s market is thousands of miles away from the vast majority of producers in downstream supply chains. Besides China, the world’s largest garment exporters are Bangladesh, Vietnam, and India, where textiles are processed, dyed, and transformed into trendy closet staples.

A threadbare model

In 2024, garment exports made up a staggering 90% of Bangladesh’s total exports, accounting for over one-tenth of its GDP. Five million Bangladeshis are employed directly by the garment industry; in some villages, one clothing factory can employ almost all of the working-age population, rendering local economies entirely dependent on the business of one Western retailer.

Bangladesh’s main export market is in Europe, while Vietnam, the world’s third-largest exporter, has a stronger relationship with the US – the destination of over a third of its clothing exports – and East Asia.

Vietnam, which has recently become a major player in global supply chains, has been shifting focus towards technology exports, but garments still make up about 10% of its total exports. Pakistan, Nepal, and Cambodia are less central to global textile supply chains, but garment exports are crucial for their domestic economies.

Countries’ dependence on textile exports. Source: OEC data, 2024

Predictably, this makes their economies vastly vulnerable to economic downturns thousands of miles away. When Australian clothing retail group Mosaic Brands shut down in 2024 due to low demand and a difficult economic environment, it left 23 Bangladeshi companies without payment. The companies, which were owed a total of $30 million, employed over 40,000 people, many of whom were fired once orders from Mosaic stopped.

Long invoice payment terms of 120 days or more meant suppliers were not paid for months’ worth of orders once the Australian company entered administration; many feared needing to shut down completely, according to an ABC report.

When the problem is global in scale, the effect is even greater. During the pandemic, European and American retailers cancelled orders at the last minute, forcing hundreds of factories to close and leaving thousands of workers unemployed and owed past wages.

The disruption caused by the conflict in the Middle East could have a similar, if reduced, effect. In early March, several garment shipments were unable to leave Bangladesh’s largest airport due to the closure of airspace over the Middle East.

While most clothes exports are transported via sea, a further disruption of maritime routes, along with the rising cost of freight and insurance, could make that route impracticable too, leading to stuck shipments and cancelled orders.

Although Bangladesh’s economy has been boosted by the fashion industry so far, its sluggish growth and the increasing vulnerability of the sector mean it is time for a change. In 2023, a United Nations (UN) report found that Bangladesh had an “urgent need” for economic diversification to build resilience. Since 2016, non-garment exports have increased by over 80%, partly thanks to funding by the World Bank Group to support firms that invest in diversified sectors like plastics, electronics, and car parts. Upcoming trade talks with Thailand, Indonesia, and Japan could also see Bangladesh strengthen trade relationships in non-garment sectors.

Behind the seams

Besides its macro vulnerabilities, the fashion industry in South-East Asia has been plagued by scandals surrounding labour conditions. Workers in the Bangladeshi garment industry usually make just over minimum wage, which was recently raised to $104 a month – far below the national living wage of about $460 a month.

Rising inflation and shrinking margins driven down by local competition for contracts are making it harder and harder for workers to make enough money to stay afloat.

Child labour and forced labour have also been persistent issues across the region’s garment export industry, exacerbated by the informal and precarious nature of work contracts that make it hard for governments or watchdogs to verify whether fair labour practices are in place.

In Vietnam, almost half of all child labourers in the textile industry are under 15 and 96% of them are girls, according to the US Bureau of International Labor Affairs. In Bangladesh, a survey found that over a third of employees in the garment sector were working more than 60 hours a week, the legal limit, and that child labour was still present in subcontracted factories.

On 24 April 2013, a building in Bangladesh, housing several garment factories that supplied major global retailers, collapsed, killing 1,133 workers and injuring over 2,600. The Rana Plaza disaster made headlines around the world, partly due to its tragic avoidability – workers had noticed cracks in the building the previous day and had been assured it was safe to come to work – but also because it represented a critical failure in the way fashion supply chains operated until that point.

The disaster prompted international fashion houses to reevaluate their supply chains. The Accord on Fire and Building Safety in Bangladesh, an independent agreement between brands and trade unions made in the aftermath of the disaster, was signed by almost 200 clothing and retail giants, including H&M and John Lewis.

58 major retailers made a commitment to pay their factories’ workers a living wage, but over ten years on, the vast majority of these pledges remain unmet, according to watchdog Fashion Checker.

In a bid to show supply chain transparency, many high street retailers began publishing their Tier-1 supplier list; however, many of these lists do not go into detail on the specific suppliers and their subcontractors, which companies themselves are often unaware of.

The widespread use of subcontractors at every stage and the rapid change in demand led by the rise of fast fashion and microtrends make it difficult to nail down a single supply chain for one item, let alone an entire fashion house. Pledges that vow to monitor individual suppliers and factories can only go so far if companies barely have oversight on their own supply chains; verifying that those promises are being kept is even harder for independent observers.

Patchwork solutions

Besides the practical difficulties in supply chain monitoring, the push for ethical supply chain management may, in fact, be backfiring. Raising salaries – whether through a state-mandated minimum wage or through the promotion of a voluntary ‘living wage’ pledge – seems like an easy fix.

However, the resulting price rises could simply push retailers out of the country entirely and towards suppliers in competing countries. For economies that so heavily rely on garment exports, like Bangladesh, this would be catastrophic, making the state reluctant to raise minimum wages.

Hundreds of small factories, which already operate with thin margins and intense domestic competition, would be forced to close, increasing unemployment across the country and hitting small and medium-sized enterprises (SMEs) the hardest. In Indonesia, an effort to improve working conditions and raise the minimum wage in the industry led to unemployment rising by up to 36%.

Regulations and voluntary standards on working conditions lead to a similar story. The brand-enforced building standards enacted after the Rana Plaza disaster raised costs for factories, often to an unbearable level. The standards, enacted in 2013, led to a 33.3% decrease in garment factories in the country by 2016.

A lesser-known implication of rising wages is automation – and the consequent loss of women’s financial independence. Between 60 and 80% of Bangladesh’s garment workers are women; women also dominate Pakistan and Sri Lanka’s clothing export industries.

In Bangladesh, the growth of the garment industry in the 1980s – and of women’s role in it – led to rapid developments in gender equality, as women working outside the house and existing in public spaces became normalised. Girls living near garment factories have lower rates of child marriage, higher education rates, and tend to have children later – all crucial markers of gender equality.

If wages were to rise, factories would likely cut their workforce to maintain their thinning margins, which could worsen conditions and hours for the remaining workers. A higher cost of labour could also accelerate the push towards automation – already embraced in China and, increasingly, in Vietnam.

When factories in Bangladesh buy heavy machinery, they almost always recruit men to operate it (even when there is little need for physical labour), shifting the garment industry from an instrument of female empowerment to one of discrimination.

A stitch in time

Homegrown solutions are likely to be far more effective at resolving both countries’ vulnerability to supply chain shocks and labour conditions in suppliers themselves.

To improve working conditions and wages, the solution often comes down to financing. In 2021, for example, the International Finance Corporation (IFC) made a $23 million investment in a Bangladeshi textile dyeing company to help build a new, technologically advanced factory.

Working directly with suppliers – the much-feared ‘deep tier’ of global fashion supply chains – is often much more effective than forcing change through global retailers all the way at the end of the supply chain. Financing gives suppliers the funds they need to improve working conditions and building safety.

Access to credit can also make the industry as a whole more resilient and less vulnerable to a cash crunch when global transport is disrupted; this is all the more crucial for smaller garment manufacturers, which often have the thinnest margins and are forced to accept long payment terms by their multinational buyers.

—

From Miranda Priestly’s high fashion to London and Tokyo’s high streets, clothing dominates global supply chains. For the major garment exporters in South East Asia, this has meant a boost in exports and economic development – but often at the cost of vulnerability and labour exploitation.

International initiatives to create ethical supply chains have removed some of those issues, but can hurt smaller producers and don’t protect countries against demand shocks and transport disruptions. The real game-changer for resilient and ethical supply chains will be homegrown solutions – often in the form of trade finance to encourage SMEs to enter the export market or support garment suppliers to promote better working conditions.

Coffee

- Coffee is a globally traded commodity with a complex supply chain linking smallholder farmers in developing countries to consumers in wealthier regions.

- Environmental pressures, including climate change, deforestation regulations, and biodiversity loss, are increasingly threatening coffee production and distribution.

- Significant human rights concerns, such as child labour and exploitative working conditions, highlight the need for greater transparency and ethical standards in the industry.

As early mornings and late evenings are spent ensuring the financing of global trade, this commodity stands out as an addictive enabler.

Coffee, sometimes poured with care and semi-skimmed milk, and sometimes drunk like water, plain and quick, is the world’s most traded tropical product.

With consumption exceeding 2.25 billion cups daily, worldwide coffee exports reached $51.2 billion in 2024, making the drink one of the most highly demanded agricultural products in the world.

The process of the bean reaching the cup goes beyond pressing a button on an espresso machine. It starts with smallholder farmers, mainly in countries such as Brazil, Vietnam, and Colombia, who grow and harvest coffee cherries. After picking, cherries are processed to extract and dry the beans.

Exporters then sell the beans, often through traders or cooperatives, on international markets. Importers and roasters in consuming countries purchase the beans, roast and package them, then distribute them through channels like retailers and cafés.

Almost 90% of coffee is grown in developing economies and is exported primarily to North America, Europe, and East Asia, making the delicacy emblematic of the global North-South dependency.

Thereby, the brewing threats to the caffeinated supply chains pose a concern both to emerging market economies and to coffee addicts everywhere.

The ‘black gold’

Coffee’s story spans continents and centuries, carrying with it rich histories and often-overlooked origins. A ritual-bound delicacy in Italy – sipped at precise hours and in prescribed forms, a mystical teller of fortune in Turkish tradition, a vanilla-laced venti oat indulgence in the US, a narcotic in Canary Wharf that keeps eyes open across the long working hours: coffee culture is almost as complex as the popular commodity’s supply chains.

Coffee’s roots can be traced back to an ancient tale, all the way to the Ethiopian highlands in 700 A.D. In the folklore, Kaldi, a goatherder, notices his goats experience an intense burst of energy after eating certain red berries.

Growing curious, Kaldi consumes the same berries, finding himself fueled by this inexplicable energy. His discovery leads him to a local monastery, where monks begin using the berries to concoct a drink that helps them stay awake over late-night prayers.

From there, the rumours about this mystical berry spread across the Arabian Peninsula, where coffee began to be cultivated and traded.

More official accounts trace coffee back to 15th-century Yemen, where it gained popularity and spread across the region, particularly to Iran, Egypt, Syria, and Türkiye, prompting public coffee houses and the sale of coffee.

However, on par with the folklore, Ethiopia is largely credited for the origin of coffee, especially as the homeland of coffee arabica. Deemed ‘black gold’, coffee is cherished in Ethiopia, accounting for 37% of the country’s total exports, with the primary destination being Europe.

But, beginning with Ethiopia, climate change, increased regulation – particularly surrounding environmental, social, and governance (ESG) initiatives, infrastructural problems, and crucially, the human costs of coffee production, are putting a growing strain on global coffee supply chains.

Deforestation, conservation, and climate change

According to the European Parliament, the European Union’s (EU) general consumption accounts for 10% of global deforestation. In 2023, the EU announced its Deforestation Regulation (EUDR), designed to cut EU consumption-driven deforestation by 29% by 2030, and save 72,000 hectares of forest every year, starting from 2030.

For coffee, this regulation requires the full traceability of the harvested cherries upon their arrival to the EU, which is particularly difficult for countries like Ethiopia, where there are highly fragmented supply chains, with an abundance of microholders.

The Regulation’s implementation was delayed first to 2025, and then to 2026, and to 2027 for small enterprises. This was largely because many companies weren’t ready to comply: producing countries found the rules too complex and costly, and raised concerns about insufficient traceability systems and uneven technological capabilities.

Biodiversity considerations also create growing concern for the black gold. In Latin America, which accounts for around 60% of the global coffee supply, the majority of the continent’s coffee-growing spots happen to be biodiversity hotspots. Certain coffee cultivation practices (such as the use of agrochemicals and soil conservation practices) can have dire impacts for biodiversity conservation – putting coffee production at odds with its environment.

Climate change also poses a critical threat to the supply chains bringing the bitter fuel to artisanal cafes. In a 2022 study that simulated emission scenarios modelling projections up to 2050 on coffee, cashew, and avocado plantation crops, coffee was found to be the most vulnerable. The study revealed that the negative implications of climate change were particularly dire for all the main producing regions of the commodity.

Climate-related issues also couple with poor infrastructure in causing supply chain disruptions. For instance, in 2019, excessive rainfall in Indonesia strained access to the Trans Sulawesi Railway, leading to rising bean prices.

The human cost of coffee supply chains

This year’s Thompson Reuters Institute’s Global Trade Report identified ESG standards as growing in importance for importers, referring to them as largely embedded in global trade. While the ‘E’ in ESG is often front and centre, labour rights and human rights violations associated with global supply chains cannot be overlooked.

Over the last two decades, systemic human rights abuses have been recorded across the coffee industry, particularly by multinational coffee companies.

According to International Labour Organisation statistics, the coffee industry ranks fourth among industries associated with child labour, particularly in Guatemala, Nicaragua, Uganda, and Mexico. In fact, in a 2012 survey across 372 workers in Guatemala, 98.9% reported there were minors working on the last coffee plantation they worked on, with over 87% reporting that there were children between the ages of eight and 13.

Investigations have also revealed slavery-like conditions on plantations linked to Nestlé’s supply chains, especially in Brazil, the world’s largest exporter of coffee. The workers in these cases were often trafficked to work for little to no pay, drinking water alongside animals, and overall working under dehumanising conditions.

These problems amplify the need for transparency across the deepest tiers of coffee supply chains. Although this might cause difficulty for certain suppliers and perhaps put a strain on the supply chains, the environmental and human costs are simply too high to ignore.

What can be done?

When it comes to the biodiversity implications of coffee production, Ethiopia, the ancient coffee connoisseur, has figured it out. Ethiopian coffee bases itself on the ‘agroforestry system’, which integrates coffee plants with native trees, utilising the land sustainably and supporting conservation. It’s a deep-rooted practice that deliberately incorporates crop production systems with existing vegetation.

However, this system poses challenges to the EUDR’s definitions of deforestation – again, a stringent regulation difficult to follow across production as fragmented as that of Ethiopian coffee. Regulation demands much-needed traceability, while potentially threatening the livelihoods of smallholder farmers dependent on coffee exports.

Under these circumstances, an expansion of EUDR’s understanding of deforestation, as well as localised frameworks that are more easily adapted to particular regions, could be beneficial.

The use of cooperatives for exporting coffee is also a way to safeguard farmers. Coffee cooperatives, member-owned organisations made up of smallholder farmers, help farmers pool their resources, guaranteeing a fair price for their crop. This results in increased transparency and traceability of production, while improving market access for the farmers.

Regarding the unacceptable human cost of coffee production, the increased supply chain visibility, vigilant upholding of labour rights, and growing emphasis on ESG standards are integral.

Technology can also play a role in increasing transparency and traceability across supply chains – ideally with countries creating the regulation taking on the responsibility to bring the relevant technology to the deepest tiers of their supply chains.

—

Caffeine keeps us awake, alert, and aware. But more importantly, it’s a true delicacy that can be the marker of a good conversation, a relaxed morning, or a needed excuse to waste time.

If we want to keep sipping on overly-priced oat flat whites, then it’s time to start paying attention to where the beans come from.

Bananas

-

The banana industry is a significant driver of global trade worth $15.3 billion, yet it remains vulnerable due to a lack of genetic variety that leaves the dominant Cavendish variety at risk of extinction from fungal disease.

-

Logistical challenges such as port congestion and aging refrigerated container fleets can lead to rapid spoilage, as even a four-hour delay in refrigeration can cause entire shipments to ripen prematurely and become unsellable.

-

Climate change poses an existential threat to production, with rising temperatures and extreme weather expected to cause a 60% reduction in suitable land for export in Latin America by 2080.

In 1954, a war was waged in a small Latin American country over control of a crucial resource. A democratically elected socialist president, Jacob Arbenz, had taken a stand against an American commodities giant, seizing control of production and redistributing land to the people.

The US administration, fearing loss of control over the resource and a hit to the economy and under pressure from the multinational firm, had the CIA invade the country and overthrow Arbenz, returning control of the country’s commodities back in American hands. The small country was Guatemala; the commodity, however, wasn’t oil or a precious mineral, but bananas.

The elongated berry (genetically, bananas are in the same class as strawberries) is responsible for $15.3 billion of global trade – as much as apples and oranges put together – and is growing rapidly, clocking a 6% year-on-year increase in 2025.

Bananas are the most exported fruit in the world, forming the backbone of the export economies of countries like Ecuador, Guatemala, and Ethiopia and providing much-needed income for smallholder farmers. Banana trees provide shade crucial for the cultivation of many key export crops, while leaves are used as biodegradable plates, cups, and cooking utensils for regional dishes.

Despite its sweet taste and cheerful yellow exterior, the fruit carries a turbulent history, one of agricultural colonisation and economic upheaval. Disease, environmental challenges, and supply chain disruption leave the industry on an unstable footing.

Strong skin, weak genes

Bananas and their savoury variety, plantain, have been a staple food in Central America, East Asia, and Africa for centuries. Across the world, 400 million people get between 15 and 27% of their daily calories from the fruit: in Uganda, the fruit is such a staple that the word for banana – matooke – also means food. Bananas provide 11% of Ecuador’s export revenue and are Guatemala’s biggest export.

Despite their hardy exterior, bananas are one of the most vulnerable commodities around. The fruit’s seedlessness means there is very little genetic variety, leaving the fruit at a high risk of being wiped out by disease.

In the 1940s, the Gros Michel banana, then the most common and beloved variety, was struck by Fusarium Wilt TR1, a fungal disease which shriveled banana leaves, killing the plant. Despite efforts to contain it – with farmers burning their groves and moving to new land in an attempt to break free of the pest – the epidemic spread around the world. Within a few years, the Gros Michel banana was extinct, its taste only preserved by some types of artificial food flavouring.

The current most popular variety, the Cavendish banana, could meet a similar end. A different variation of Fusarium Wilt, TR4, decimated plantations in Peru and Venezuela last year, and could keep spreading, wiping out the billion-dollar industry in months. Attempts to find a Fusarium Wilt-resistant plant that is as tasty, fast-growing, and long-lasting as the Cavendish have been fruitless. For now, the world has placed all its bananas in one genetic basket, and the consequences may soon be devastating.

Banana boats

Bananas are grown year-round and harvested while still unripe, making it possible to transport the fruit on ships – a much cheaper option than air freight, which is how fruits like strawberries and mangoes must be transported. When they arrive at their final destination, the fruits are sprayed with ethylene gas, which initiates the ripening process. Once ripe, they are transported to their final location and sold in supermarkets around the world.

However, the tight timelines mean that, unlike other commodities transported by ship, bananas are far more susceptible to delays and supply chain disruptions. Ship diversions, bottlenecks, and holdups at customs, normally a pricey inconvenience, can cause entire shipments of bananas to rot.

Because timelines are so tight, even minor delays can cause nationwide shortages. In March 2025, tropical storms in the South Pacific delayed ships carrying the golden fruit, causing a UK-wide ‘banana famine’ that left many supermarkets without stock.

Delays in refrigeration of just four hours – for example due to port congestion or issues with refrigerated containers – can cause the fruit to ripen too early, making it unsellable to most major retailers. Shortages in refrigerated containers caused by an aging fleet and rising temperatures lead to further delays and raise transport costs.

Last year, Maersk launched a new technology that would enable bananas to ripen in transit, cutting down on warehouse costs and waiting times. However, the solution is not yet used at scale, and might exacerbate the effect of delays in inland transport.

No weather for bananas

While banana plants thrive in warm weather, temperature rises caused by climate change are instead placing much of global production in jeopardy. In Latin America, climate change will cause a 60% reduction in the area suitable for export production by 2080. Climate change-related natural disasters like hurricanes and floods can wipe away plantations, while excessive rainfall leads to the humid conditions where TR4 and other fungal plant diseases thrive.

While rising temperatures may enable growth in some areas which are now too cold, like southern Brazil, the massive loss of land area in Central America, Brazil, and India will still cause a net loss in production acres by 2050. Unless yields rise significantly, this could spell the beginning of the end for the fruit – and those who grow it.

Banana production itself is hardly climate-friendly. Because of the plant’s susceptibility to disease – which, again, grows with climate disruption – farmers are relying more and more on fertilisers and pesticides. Many of these products are made with fossil fuels, and even more are toxic to humans – especially in the massive quantities required to stave off fungi and other parasites from plantations.

These chemicals seep into groundwater and pollute the air, leading to increased rates of nearly all disease, from learning disabilities in local children to cancers and nervous system damage for plantation workers.

An increased focus on fairtrade and organic bananas may reduce the environmental impact, but often at the cost of higher prices and a more volatile crop, vulnerable to disease and low yields.

—

While the era of banana republics may be over, the fruit is facing its biggest challenge yet. Disease and climate change are threatening production itself, while fragile supply chains are making it harder and harder for producers to get bananas to their final destination intact.

The effect of this goes far beyond commodity prices and futures contracts. Bananas are a crucial production of smallholder and collective farms in the Caribbean and East Africa, forming both a staple of local diets and a much-needed source of foreign income. The transport issues faced by the fruit, let alone its existential threats, could put millions of livelihoods in jeopardy.

At each end of a shipping contract or trade finance transaction lies a tangible commodity – one that sellers rely on to survive and buyers could not imagine life without. Seeing exports as more than numbers on a spreadsheet helps us put oft-overused phrases like “sourcing issues” and “supply chain disruptions” into real terms, and appreciate the impact they have on people and resources around the world.