Estimated reading time: 10 minutes

ONE.

However, there is a common miss-conception that four or five multiple banks must be involved to manage letter of credit transactions.

These multiple banks include credit issuing banks, advising banks, negotiating banks, confirming banks, and reimbursing banks.

What is less understood is that these “banks” are functions, not necessarily physical banks.

The trade finance functions these banks perform in a transaction can be done by separate banking institutions or by one bank under UCP 600 guidelines (Uniform Customs and Practice for Documentary Credits, ICC Publication 600).

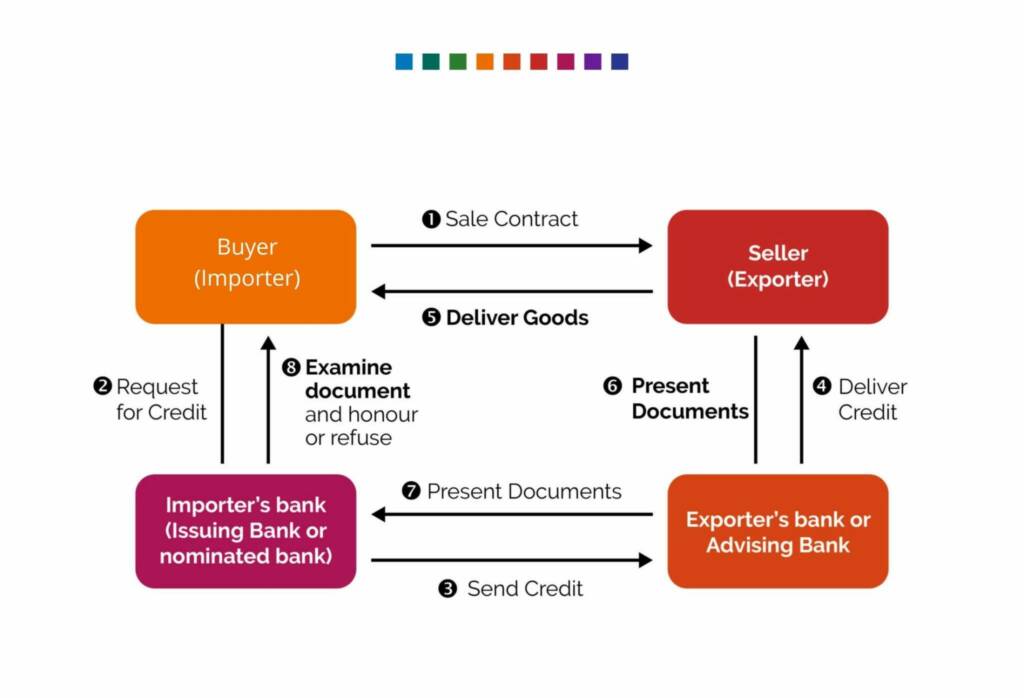

First, a quick review of the documentary letter of credit participants and processes to put this discussion into context.

The documentary letter of credit

Documentary letters of credit are used in international trade as the most secure method for purchasing a seller’s goods.

A buyer applies to a commercial bank to substitute the bank’s credit for his own and for the bank to issue a documentary letter of credit to the seller through the seller’s advising bank for the purchase. The seller then ships the goods and presents the transport documents required in the credit to the negotiating bank for negotiation of the documents for payment.

The entire process is managed by the banking community with guidelines called the Uniform Customs and Practice for Documentary Credits (UCP), published by the International Chamber of Commerce in Paris (first published in 1933).

The UCP is a set of 39 Articles or rules for the issuance and management of documentary letters of credit and is used by bankers and commercial parties in more than 175 countries for trade finance guidelines.

Some 15% of international trade uses letters of credit, totalling over $1 trillion each year in trade volume.

Defined functions in the UCP include:

- Trade finance is defined as a documentary letter of credit or documentary collection payment method; usually through banking channels, but not required by the UCP.

- The applicant is the person or company who has requested the letter of credit to be issued; this will normally be the buyer.

- The beneficiary is the person or company who will be paid under the letter of credit; this will normally be the seller. UCP 600 Article 2 defines the beneficiary as “the party in whose favour a credit is issued”.

- The issuing bank is the bank that issues the credit, usually following a request from an applicant.

- The nominated bank is a bank mentioned within the letter of credit at which the credit is available. In this respect, UCP 600 Article 2 reads: “Nominated bank means the bank with which the credit is available or any bank in the case of a credit available with any bank”.

- The advising bank is the bank that will inform the beneficiary of the credit, send the original credit to the beneficiary or their nominated bank, and provide the beneficiary or their nominated bank with any amendments to the letter of credit.

- Confirmation is an undertaking from a bank other than the issuing bank to pay the beneficiary for a complying presentation, allowing the beneficiary to further reduce payment risk, although confirmation is usually at an extra cost.

- A confirming bank is a bank other than the issuing bank that adds its confirmation to a credit upon the issuing bank’s authorization or request.

- A complying presentation is a set of documents that meet the requirements of the letter of credit and all of the rules relating to letters of credit.

- An examination is done by a negotiating and/or issuing bank to determine if the presented documents exactly comply with the terms and conditions of the credit.

The traditional letter of credit process

A buyer (importer) has a bank issue a letter of credit to its seller (exporter) as a method of payment. The exporter accepts the credit from an advising bank and ships the goods.

The seller complies with the documents called for in the credit’s terms and conditions from various sources and presents them to a negotiating bank for examination and payment.

These documents normally include a transport document (bill of lading and the like), invoice, packing list, certificate of insurance, certificate of origin, inspection certificate, fumigation, and phytosanitary certificates.

When and if the presented documents meet the terms and conditions of the letter of credit, it becomes a complying presentation and the issuing bank’s conditional promise to pay (independent of the buyer) is honoured.

If the documents do not comply, the letter of credit reverts to a documentary collection as the payment method and the buyer must provide the payment outside of the bank’s obligation.

This process is based on physical paper documents compiled by the exporter and moved, usually by courier, from his location to the negotiating bank. Then, by courier again, to the confirming or issuing bank for a second examination for compliance and payment.

Documentary letters of credit were issued via telex starting in 1953. The Society for Worldwide Interbank Financial Telecommunication (SWIFT) began operations in 1977 as a more secure telex service between banks.

Today, over 90% plus of all documentary letters of credit are issued in SWIFT MT700 message format. However, the original documents required for negotiation and payment are paper and must still be couriered or posted between the banks.

However . . . there are a few challenges (snags).

Key challenges

The biggest challenges for letter of credit use are payment time, discrepancies, and costs.

Payment time

Globally, the average time for payment of a sight (to be paid upon presentation) letter of credit from the bill of lading date is 24 days.

This time is made up of three main elements:

- resubmitting discrepant documents;

- courier time moving paper documents around the plant; and

- examination time up to five days for the negotiating and five days for the issuing bank in the chain.

Discrepancies

Globally, only 63% of all presentations comply with their letter of credit terms and conditions. (ICC 2018 Survey).

Non-complying presentations revert to documentary collections and are not supported with the issuing or confirming bank’s promise to pay.

Costs

Each bank involved in a transaction collects bank service fees.

These fees include issuing fees, advising fees, confirming fees, reimbursing fees, discrepancy fees, negotiating fees, discounting fees, wire fees, copy fees, and courier handling fees – to name the main ones.

Traditionally the buyer pays its in-country bank, custom, and port fees while the seller pays its in-country bank advising and shipping fees.

However . . . there are a few solutions to (un-snag) these challenges.

Combatting letter of credit challenges

The seller can require the letter of credit to be issued under UCP600 and eUCP Version 2.0

Which are; the International Chamber of Commerce Uniform Customs and Practice for Documentary Credits (UCP 600) and the Supplement for Electronic Presentation (“eUCPv2.0”), in effect 1 July 2019.

The eUCPv2.0 allows for electronic record presentation of the negotiable document set in lieu of paper documents.

The highlights include of the digital supplement include:

1. Allows presentation of electronic records alone or in combination with paper documents.

2. Documents may be presented as an electronic record (example, PDF format).

3. Place for presentation means an electronic address in addition to a physical address.

4. Sign and the like shall include an electronic signature.

5. Any requirement for the presentation of one or more originals or copies of an electronic record is satisfied by the presentation of one electronic record.

Documentary letters of credit issued under UCP 600 and eUCPv2.0 guidelines allow presenters to submit the negotiable document sets online via the Internet. The presenter may also re-submit individual discrepant documents online.

This capability eliminates delays involved with couriering documents to negotiating banks and then onto issuing banks.

Eliminate discrepant documents by using cloud multitasking between the seller and the various sources of original documents

Sellers must compile transport documents from various sources, including:

- a chamber of commerce for a certificate of origin,

- an insurance company for an insurance certificate,

- a port’s services for phytosanitary and fumigation certificates,

- an SGS for an inspection certificate, and

- a freight forwarder for the transport document that it receives from a carrier.

All of these documents must comply with the letter of credit’s terms and conditions, including any amendments.

The “back and forth”, “draft submit”, “review, redraft, and resubmit”, is prone to inducing content errors and uses up a lot of the standard 21 days allowed in most credits to prepare and submit negotiable document sets.

These errors come from transposed keyboard entries, second language misunderstandings, and not having the same source document version or latest amendment.

However, by using the cloud and giving third-party sources access to the original and amended version of the letter of credit and transport documents online in real-time, it is possible to review each document against a credit’s final terms while it is being composed, and prior to submitting the final as the original.

Under eUCPv2.0 guidelines the electronic records so produced are acceptable as “originals” and “copies”, and do not have to be printed and then couriered to the seller to be compiled before presentation.

They can be downloaded by the presenter as PDF electronic records and compiled into a negotiable document set.

Presentation to the issuing bank directly. The seller can send the negotiable documents directly to the issuing bank for examination and negotiation

Under UCP 600 the presenter has the option of making the document presentation directly to any bank when the credit is freely negotiable, this includes the issuing bank.

Sending the paper negotiable documents directly to the issuing bank would reduce payment time by as much as ten days.

Sending electronic negotiable documents instead of traditional paper directly to the issuing bank could reduce payment time from the world average of 24 days to 48 hours by eliminating couriers and multiple handing by advising, negotiating, confirming, and reimbursing banks.

Lower the cost of service fees by reducing the number of banks charging fees; and the time cost of money by reducing the time to payment

The transaction cost for the seller can be reduced by sending the required documents directly to the issuing bank for negotiation and payment, eliminating a separate negotiation bank and courier fees.

The cost of goods sold is reduced by the seller not having to include these fees in the cost of the product and services.

The time cost of money is reduced by reducing the time to payment.

The average value of a documentary letter of credit fluctuates around $400,000 (ICC Survey). Assuming a 0.5% monthly cost of money, reducing 24 days to 48 hours could save over $1000 per transaction.

Summary

Today’s trade finance environment for documentary letters of credit is complex, requiring many dozens of documents and hundreds of interactions; time-consuming, requiring weeks and months to make a settlement; expensive, from multiple bank fees and the cost of money; and archaic, relying on telex (70-year-old technology) and paper (much older) and couriers (think pony express).

ICC publications UCP 600 and eUCPv2.0 provide the guidelines for changing this environment.

However, it is asking too much of the banking community to adopt these guidelines and drastically reduce their own revenues.

The internet light at the end of the tunnel is going to have to be switched on by the world trading community of importers, exporters, freight forwarders, carriers, and service providers to push modernity.

The first eUCP Version 1.0 guidelines were published in April 2002 (18 years ago); the latest eUCp Version 2.0 guidelines were published in July 2019. It could be another 18 years . . . or maybe not.

Check out TFG’s complete letter of credit guide here.