Confidence, demand and energy shock waves, writes Ana Boata, Global Head of Economic Research at Allianz Trade. Allianz Trade is the new name for trade credit insurer Euler Hermes, which became part of the Allianz SE group in 2018.

Exporter expectations for 2022

Allianz Trade, the world leader in trade credit insurance, decided to check the pulse of companies in the United States, China, the United Kingdom, France, Italy and Germany.

The company carried out two surveys – one before the start of the invasion of Ukraine and one after, involving nearly 3,000 corporates.

Russia-Ukraine conflict brings headwinds to global economic recovery

The invasion of Ukraine has brought back significant headwinds to the global economic recovery.

Before diving into the results of our Allianz Trade Global Survey, let’s take a look at our economic outlook.

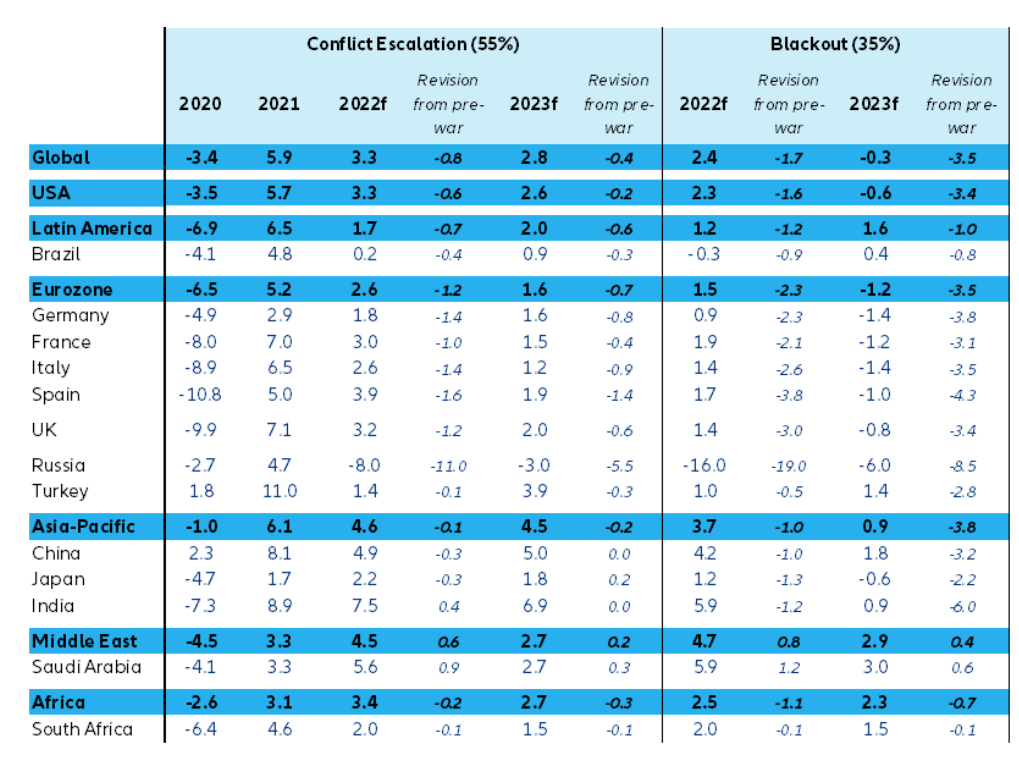

Following the invasion of Ukraine, we have cut our forecast for global GDP growth to +3.3% in 2022 and +2.8% in 2023 (compared to +5.9% in 2021), down by -0.8pp and -0.4pp, respectively. Almost two-thirds of our downward revision is due to confidence and supply-chain shocks, with the remainder due to higher commodity prices.

Global inflation will also prove higher and stickier (6% in 2022, revised up by +1.9pp) because of higher energy prices and longer-than-expected supply-chain disruptions, which will contribute to price pressures in equal measure.

While current negotiations between Ukraine and Russia could provide a path towards a ceasefire, further escalation cannot be excluded, resulting in even harsher sanctions and counter-sanctions (including on energy supply).

In such an adverse scenario, global inflation would soar to 7% this year while growth would decline to +2.5% before the global economy enters into a recession 2023 (-0.3%).

Additionally, we expect global trade growth to moderate by at least -2pp in 2022 to +4% in volume terms, just below its long-term average.

Confidence and demand shocks will result in a loss of $480 billion in exports to Russia and Eurozone countries in 2022.

However, net exporters of commodities in the Middle East and Latin America could benefit from higher commodity prices and potential substitution effects away from Russia.

In terms of trade costs, sustained higher oil prices could lead to a new record high in freight rates in Q2 (+40% vs previous peak).

Furthermore, the COVID-19 outbreaks in China and the zero-COVID policy will extend supply-chain bottlenecks and keep suppliers’ delivery times elevated.

After the invasion of Ukraine, the share of respondents expecting an increase in their export turnover dropped from 94% to 78%

Last year was an exceptional one for exporters: Overall, 7 out of 10 declare they recorded higher-than-expected export performance.

The U.S. and Germany saw especially strong performance, with 75% and 76% of corporates saying they achieved higher-than-expected exports, respectively.

Nonetheless, exporters did have to adapt to a new normal in trade in a context of lingering lockdowns and transport bottlenecks.

How? In the US, where companies were most disrupted by supply shocks, this entailed increasing inventories (48%), finding new suppliers (45%) and targeting new export markets (43%) to boost growth.

Over a third of exporters in France, Italy and the UK say they also relied on finding new suppliers to cope with supply-chain disruptions, while 39% of German exporters say they focused on new export markets, mostly those close to home such as France and Spain.

Barely out of the COVID-19 crisis, and now facing the economic shockwaves of the invasion of Ukraine on global trade, what do exporters expect for 2022?

Before the invasion of Ukraine, companies seemed to think that 2022 would bring them even more opportunities than 2021: overall, 94% of businesses were expecting an increase in their export turnover, with the most optimistic companies in France and Italy (97%).

Most exporters were planning to expand their businesses to new markets in 2022 (79%), especially Chinese and American firms (92% and 84%, respectively).

But the military aggression in Ukraine and the massive sanctions imposed against the Russian economy changed the story.

Françoise Huang, Senior Economist for Global Trade and APAC at Allianz Trade said: “Unsurprisingly, the conflict rattled these expectations: the share of respondents expecting an increase in their export turnover dropped from 94% to 78% (-16 pp). In Italy and France, where companies were the most optimistic, 29% (+26 pp) and 23% (+20 pp) of firms expect a decrease of their export turnover in 2022, respectively.

“Even if Russia and Ukraine are not key final markets for European exporters, the war situation is affecting global trade through indirect effects (supply chains, raw material, energy), weighing on export opportunities for firms”.

Energy prices have always been a major concern for exporters (and even more since the invasion of Ukraine)

The “grand reopening” of the global economy in 2021 was a rollercoaster ride for companies as global supply-chain disruptions sent transportation costs and energy prices surging to record highs.

Indeed, the companies we surveyed said that the top five risks that affected export growth in 2021 were uncertainty about demand due to COVID-19 (40%), high energy prices (35%), labour shortages and costs (35%), transportation costs (33%) and input shortages (30%).

Will 2022 bring some respite?

Even before the invasion of Ukraine, companies were not entirely convinced.

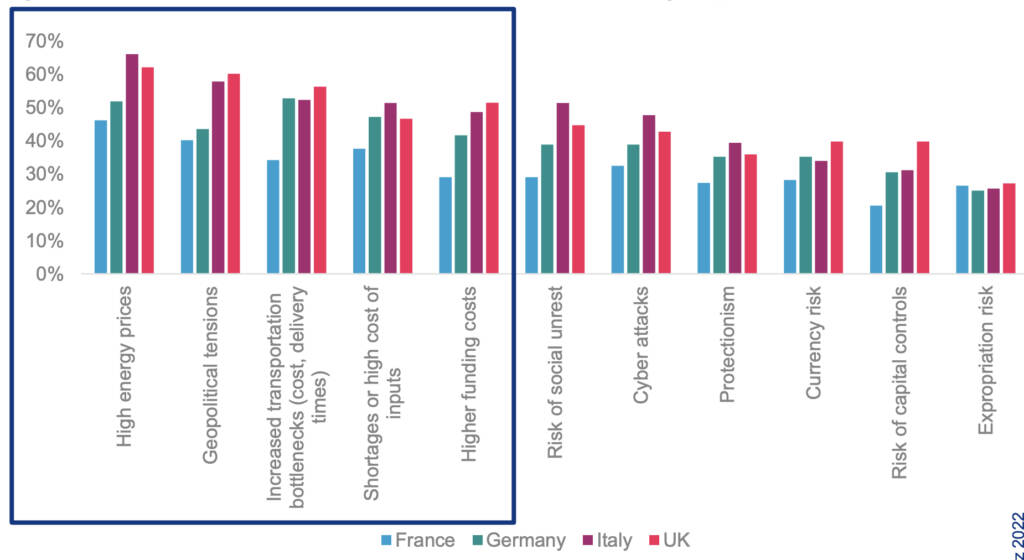

Energy prices were already by far the top concern, with 72% of companies saying they expected them to remain a challenge in 2022, and over a third expecting them to become more of a challenge this year.

The share of exporters expecting energy prices to become more of a challenge in 2022 is highest in Italy (46%), followed by the US (38%) and France (37%).

Since the invasion of Ukraine, high energy prices have become even more of a concern for European exporters.

Ano Kuhanathan, Head of Corporate Research at Allianz Trade, said: “The share of European corporates that expect high energy prices to become more of a challenge has increased from 37% to 56%, with most worried in countries with the highest dependency on imports of gas: Italy (66% compared to 46% pre-conflict), the UK (62% compared to 47% pre-conflict) and Germany (52% against 34% pre-conflict). The fact that France has the lowest share of companies concerned by high energy prices (46% vs. 37% pre-conflict) likely reflects the implementation of the government’s “Resilience Plan” that takes into account the cost of the energy bill for most corporates”.

More than half of respondents in Europe now expect non-payment risk to increase in the next six to twelve months

Exporters’ exposure to non-payment risk seems to have increased of late: Our survey shows that overall, non-payment issues had a moderate or significant impact on export activity over the past 12 months for nearly 60% of firms, with the highest shares in France (66%), China (65%) and the U.S. (58%).

Moreover, despite the strong economic rebound in 2021, cash hoarding in many corporates and a solid recovery in global trade, 50% of our respondents declare that payment times got longer in 2021, especially in France (62% of firms). Interestingly, among firms that have undertaken digitalisation – which we would expect to smoothen transactions – 58% of respondents still reported longer payment times.

Non-payment risk will besides remain an issue for exporters in 2022: before the invasion of Ukraine, nearly 1 exporter out of 3 expected payment terms and non-payment risk to increase. Following the invasion and the consequent impact on the global economy, more than half of respondents in Europe now expect non-payment risk to increase in the next six to twelve months.

Similarly, over 40% of European exporters now expect payment terms to lengthen after the conflict broke out.

International strategy: Exporters foster local production and self-financing

For all the concerns about the beginning of the end of globalisation, the COVID-19 crisis did not spark a wave of reshoring in 2021.

But most companies in our survey (79%) still prefer to produce on home ground, ranging from 74% in the UK to 89% in China.

How will companies fund their ambitions in 2022? Before the invasion of Ukraine, cash flows were the top source of financing for more than half of exporters (53%), followed by bank loans (49%) and credit from suppliers (36%).

The share of exporters planning to use cash was highest in the UK (64%), followed by the US (57%) and China (54%).

Following the invasion of Ukraine, 44% of European exporters say they will seek more investment for international development than previously planned, probably in an aim to diversify markets rather than retreat from or downsize export ambitions in the wake of the conflict.

However, 15% of corporates don’t plan to invest or will reduce their investment plans due to the conflict.

State support: From lifesaver to corporate morphine?

Our survey reveals that a majority of exporting firms (54%) received some form of state support over the last 12 months, especially in China (70%) and Italy (60%).

Additionally, two-thirds of respondents confirm that this support in part helped their business survive the crisis.

About a quarter of respondents report that they were also able to invest in new production capacities and diversify suppliers as a result, while about 20% say they were able to reduce payment times to suppliers.

How can governments support companies further?

As many economies are struggling with skilled labour shortages in Europe, 44% of firms in France, 45% in Germany and 53% in Italy call for their governments to implement upskilling labour policies.

Moreover, unsurprisingly, after a few years of somewhat protectionist US policies and a year into Brexit, almost half of US and UK firms want their governments to deliver new free trade agreements.

While the worst of the pandemic appears to be behind us, around 50% of European exporters say additional state support in the form of more state-guaranteed loans and direct subsidies would help their business better withstand the impact of the conflict.

In fact, even before the start of the conflict, over 30% of all firms surveyed expected state support to fund their activities in 2022. Financial state support seems to have become a “new normal” for some firms.

Read our latest issue of Trade Finance Talks, May 2022