Money laundering has become more visible in global trade over the past few years, and several organizations are trying to identify and prevent it. The 2019 amendment to the Trade Finance Principles paper outlines the use of demand guarantees and highlights several compliance practices that banks can arm themselves with for this fight against financial crime.

Introduction

Over the last few years, there has been an increasing focus on identifying and preventing money laundering activities in global trade. To assist, the Wolfsberg Group, the International Chamber of Commerce (ICC), and the Bankers Association for Finance and Trade (BAFT) have joined forces to raise the level and standardize the practice of financial crime compliance activities within the trade finance industry. The fruitful cooperation resulted in the 2017 publication of the Trade Finance Principles paper and its 2019 amendment.

The Trade Finance Principles paper outlines the role of financial institutions in the management of two key processes. The first is to address the risks of financial crime associated with trade finance activities and the second is to aid in compliance with national and regional sanctions and with the United Nation’s (UN) non-proliferation of weapons of mass destruction (NPWMD) requirements. These trade finance principles apply to all banks regardless of size and do not require a bank to have significant electronic systems to apply them. These principles are the basis of what was always considered to be good banking practices for combating trade-based money laundering.

The 2019 amendment and its application to demand guarantees transactions is the focus of this article.

What are Demand Guarantees

Guarantees are instruments issued by banks and used by a beneficiary to secure compensation in case of contractual non-performance by the bank’s customer (the applicant). A demand guarantee may be used to provide compensation to (a) a buyer if the seller does not provide goods of the agreed quality by the set deadline, or (b) a seller if the buyer fails to make regular payment under a sales contract. Demand guarantees are different from documentary credits, which represent performance-related payment instruments (i.e., once a seller has performed their obligations and presented the required documentation, payment can be made through the documentary credit). Guarantees can be used in support of many types of financing or other commercial prospects. It should, therefore, be recognized that guarantees are not always issued in relation to trade finance activities (i.e., they are not related to the movement of goods, imports, or exports).

There are two forms of guarantees depending on agreements between the contracting parties of a commercial relationship: direct guarantees and indirect guarantees. The use of either usually depends on the nature of the underlying transaction and the agreement between the applicant and beneficiary.

Direct Guarantees

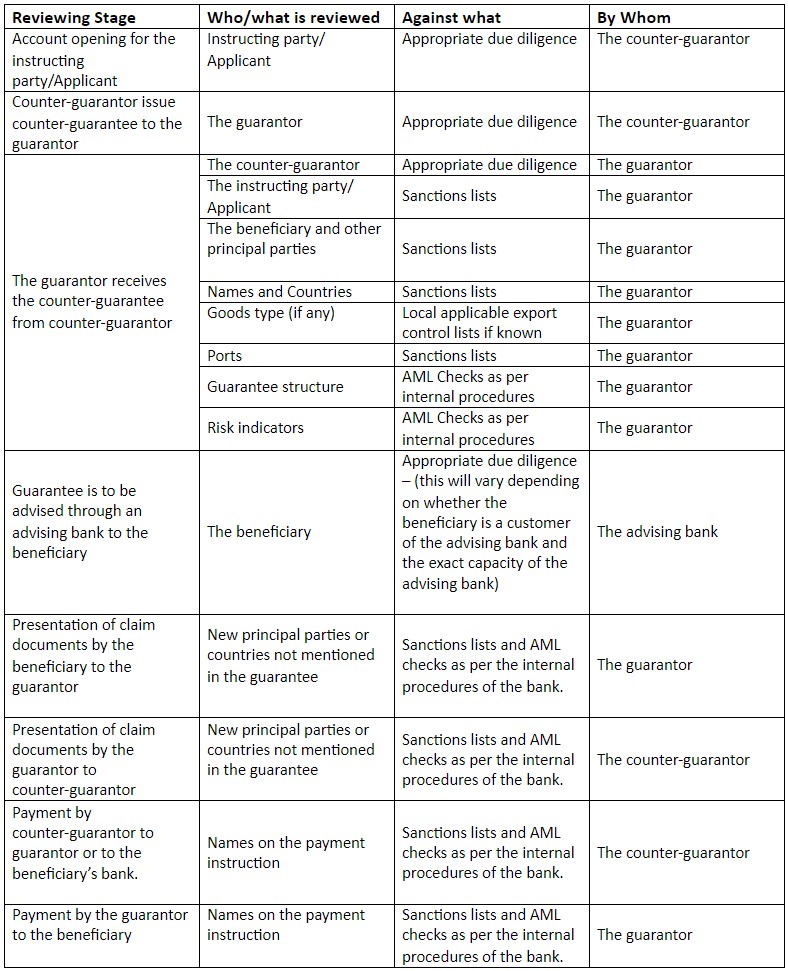

A guarantee is considered direct when a client asks their bank to issue it directly in favour of the beneficiary without the existence of an intermediary bank. Figure 1 shows a direct guarantee structure.

Each line on the diagram represents an independent commercial and legal relationship. The guarantee issued by the guarantor is independent of the underlying relationship between the applicant and beneficiary that prompted the issuance of the guarantee. A demand guarantee is also independent of the instructions relationship under which the applicant requested the guarantor to issue the guarantee in favour of the beneficiary. A guarantee is subject only to its terms, which may be expressly stipulated in the guarantee or incorporated by reference (e.g., ICC rules). Thus, no defence arising under the underlying transaction or the applicant-guarantor relationship can be asserted by the guarantor to avoid the payment of the guarantee.

Before the issuance of a guarantee, the contract terms are usually agreed upon between applicant and beneficiary. The applicant then communicates details of the required guarantee to the bank by filing an application to issue the guarantee. Under a direct guarantee, the beneficiary shall present a demand directly to the guarantor, who will check the demand for compliance with the terms and conditions of the demand guarantee. If it complies, the guarantor will pay the beneficiary the amount demanded. Direct guarantees are perceived to be less expensive for the applicant as it only involves one bank. However, direct guarantees typically involve various risks for the beneficiary in cross-border business, including the guarantee being subject to foreign country law, in addition to country and political risks.

Indirect Guarantees

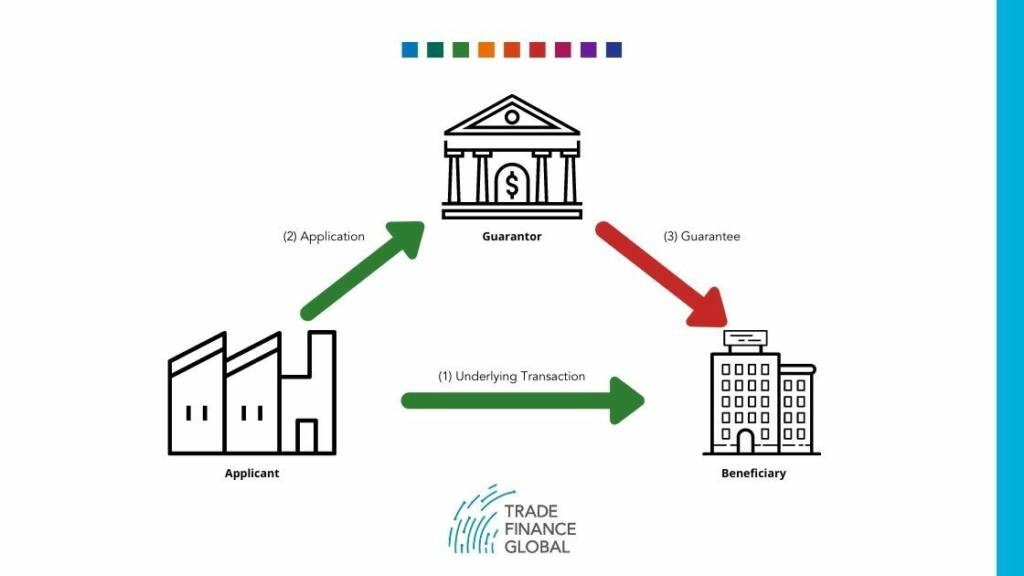

A guarantee is considered indirect if it is issued by a correspondent bank in the importer’s country under the instruction of the exporter’s bank. This correspondent bank is requested by the instructing bank (counter-guarantor) to issue a guarantee in favour of the beneficiary in return for the latter’s counter-guarantee. Figure 2 shows an illustration of an indirect guarantee structure.

Under indirect guarantees, there are two independent undertakings. The first is the counter-guarantee issued by the counter-guarantor in favour of the guarantor. The second is the demand guarantee issued by the guarantor in favour of the beneficiary. Indirect guarantees are generally used in cross-border transactions. An indirect guarantee structure can be demonstrated by an importer asking an exporter to arrange for a guarantee to be issued by a guarantor located in the importer’s country. A counter-guarantee is then issued by a bank in the exporter’s country (counter-guarantor) in favour of a correspondent bank (guarantor) in the importer’s country. This counter-guarantor acting upon the applicant’s instructions requests the local guarantor to issue its guarantee in favour of the beneficiary and undertakes to pay the counter-guarantee amount if the guarantor presents a demand that confirms the terms of the counter-guarantee. A counter-guarantee is independent of the guarantee, the underlying relationship, the application, and any other counter-guarantee to which it relates. The guarantee and the counter-guarantee may have different terms and be subject to different laws and legal jurisdictions.

Controlling Risk – mechanisms for identification and prevention

The same level of information may not be available to all parties involved in the execution of a guarantee transaction. Often the commercial parties will have complete information while other parties, like a guarantor or advising bank, may not have such detailed information available. Furthermore, it is important to note that:

- Banks have varying degrees of system capabilities, leading to differences in their reviewing capabilities.

- Commercial practices and industry standards determine finite timescales in which to act. For demand guarantees, banks may follow the Uniform Rules for Demand Guarantees ICC Publication No. 758 or otherwise be subject to local laws and regulations.

Wolfsberg Group, ICC, and BAFT indicate that the risk control framework for demand guarantees should generally have elements adequate to identify:

- The nature of the counterparty relationship;

- The reasonableness of the underlying transaction, when compared with the business operations of the counterparties; and

- Whether relevant authorities have sanctioned either the underlying activity or the counterparties to the activity.

According to the Trade Finance Principles paper, the risk control activities to be implemented by banks fall into four categories: due diligence, review, screening, and transaction monitoring.

Due Diligence

To be able to identify risks related to trade activities, financial institutions need to obtain a thorough understanding of their customer’s business model, the principal counterparties, the counterparties’ locations, the goods or services that are exchanged, and the expected annual transaction flows. The assessment of risk and application of appropriate financial crime risk controls usually depends on the role of a financial institution in a transaction. It is generally difficult for one financial institution to manage all the financial crime risks in the end-to-end process given the diversity of parties involved (from producer or exporter to the final buyer). Wolfsberg Group, ICC, and BAFT mention that each bank’s established customer due diligence policies should designate which party to a trade transaction is the customer, including correspondent banks, and therefore subject to the bank’s due diligence process. It is not the responsibility of the bank to perform due diligence on all parties to the trade transaction.

The customer due diligence should be an ongoing process that includes feedback loops where a trigger event in a transaction or normal review process leads to new information or questions about a relationship. This may lead to a greater emphasis on an active exchange of information between customer due diligence information and transaction information. The due diligence process concerning customers should be enhanced when a financial institution recognizes high-risk circumstances regarding the countries, products, or counterparties involved in the issuance of a guarantee.

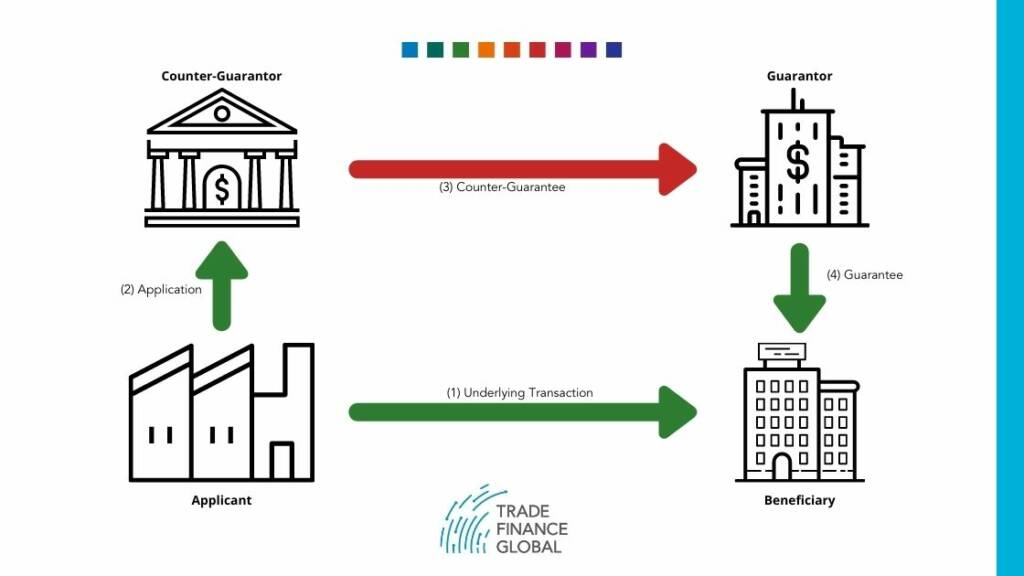

In a guarantee transaction, the issuing bank should conduct appropriate due diligence on the applicant (who is a customer of the issuing bank) before issuing a guarantee. This involves a series of standardized procedures for account opening within the issuing bank. The due diligence would support an ongoing relationship with the applicant and is not required for each subsequent guarantee applied for. The issuing bank could also conduct appropriate risk-based control checks on the beneficiary if it is not the issuing bank customer. Tables 1 and 2 summarize controls related to guarantees.

Review

The Trade Finance Principles paper defines the review stage as “any process (whether manual or automated) to review relevant information available in a transaction relating to the relevant parties involved, documents and data presented and instructions received.” Financial institutions should review guarantees on an individual basis. Transactions must be examined for fraud, sanctions, unusual, and potentially suspicious activities, the application of relevant ICC rules, and whether the conditions as documented conform to international standard banking practice and what is known of the customer.

Reviewing a guarantee should occur at initiation and during the life cycle of the transaction, primarily:

- When receiving the initial guarantee application and subsequent amendment applications from the applicant.

- In the event of a claim being made, receiving and checking documents presented by the beneficiary to the guarantor. Reviewing guarantee claims is a mostly manual process, requiring that the claim and any supporting documents that may be presented for payment are compared against the terms and conditions of the guarantee and, where applicable, any ICC rules and international standard banking practice.

- When making payment that involves screening the names in the payment instructions, including the names of any banks involved.

As described in the Trade Finance Principles paper, reviewing activity equates to document checking where the documents and their contents are checked for conformity. Appropriate financial crime risk checks should be done based on the information in the documents, transaction details, and relevant information from the customer profile. The review of events may lead to escalating the status of the relationship or exiting the customer.

For banks involved in processing guarantees, the knowledge and experience of their operations staff must serve as the first and best line of defense against criminal abuses of these products and services. Thus, banks should provide regular training to their staff who are involved in processing trade transactions. Furthermore, banks are expected to have procedures in place that allow staff to record the basis of their decision regarding any risk indicators or assessments of transaction risks that arise at any stage of the transaction. Banks are also expected to ensure that those comments are recorded for future audit control and regulatory purposes.

Screening

The screening stage involves automated processes where lists of officially sanctioned names, entities, persons, or countries are used to identify possible fraud or other concerns with respect to a relationship or transaction. This process can be applied to ensure that trade finance transactions do not violate sanctions against named individuals and entities. The effectiveness of this control depends on the availability, accuracy, quality, and usability of the source lists containing the details of target names. Financial institutions should be aware of UN resolutions concerning the proliferation of nuclear weapons, weapons of mass destruction (WMD), dual-use goods, and relevant local legislation that translates these into national laws or regulations. Financial institutions can also use the guidance issued by the Financial Action Task Force (FATF) and by the relevant authorities in regions where an export licensing control regime is in place.

In practice, once a guarantee has been issued, the issuing bank has an obligation to complete the transaction. Only if subsequent reviewing activity showed a positive match of applicable names in the transactions with the names on sanctions and terrorist lists, would the issuing bank be in a position to stop the transaction.

Transaction Monitoring

Transaction Monitoring is any review of completed or in progress transactions for the presence of unusual and potentially suspicious features. For demand guarantees, it should be recognized that it is difficult to introduce any standard patterning techniques concerning transactional monitoring processes or systems. This is due to the range of variations that are present when guarantees are used in support of construction, design, and supply contracts where beneficiaries, nature, and size of the transactions will vary significantly.

List of Control Activities for Demand Guarantee Transactions

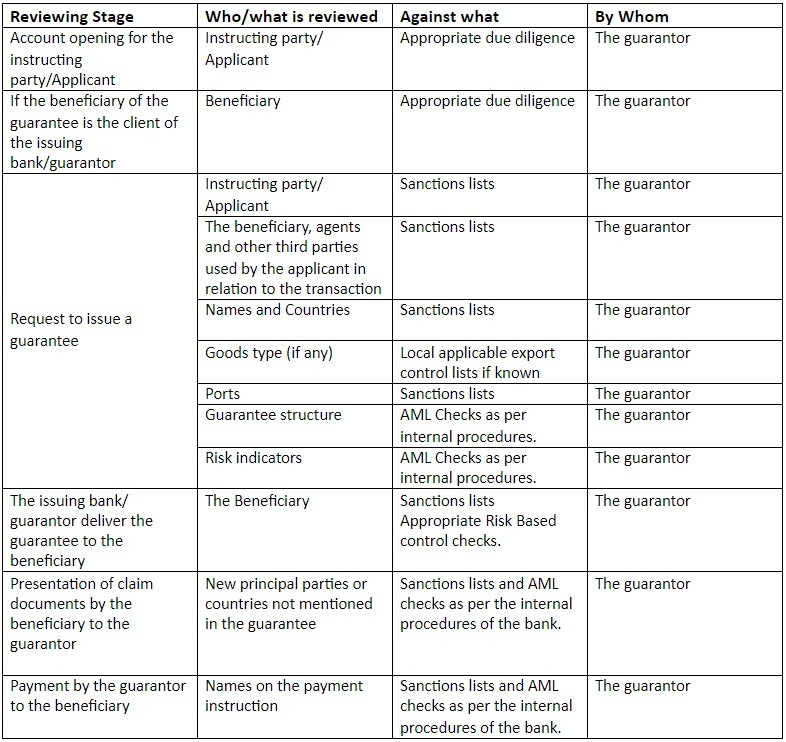

Based on the control mechanism provided by the Wolfsberg Group, ICC, and BAFT’s Trade Finance Principles, the following tables provide an overview of control activities to be applied by banks for demand guarantee transactions. Table 1 provides guidance regarding what is reviewed, against what, and by whom in a direct guarantee transaction while table 2 examines the same for indirect guarantee transactions.

Table 1: Controls Related to Direct Guarantees

For anti-money laundering purposes, counter-guarantees are treated in the same way as an original or new issuance. The bank receiving the counter-guarantee and issuing its local guarantee should treat the counter-guarantor as the applicant (instructing party) and perform customer due diligence on it. Table 2 provides guidance in respect of the risk control activities for an indirect guarantee.

Table 2: Controls Related to Indirect Guarantees