Anders la Cour, Co-founder and Chief Executive Officer of Banking Circle looks at the challenges and opportunities ahead for financial institutions serving SMEs.

For many start-ups, having a brilliant idea and getting the business up and running is the simple part. The issue of keeping increasing numbers of new and small business owners up at night is banking. The problem is, with the businesses varying so dramatically in almost every way, no single traditional banking solution can possibly meet the financial needs of every one of these small businesses. There is no one-size-fits-all solution.

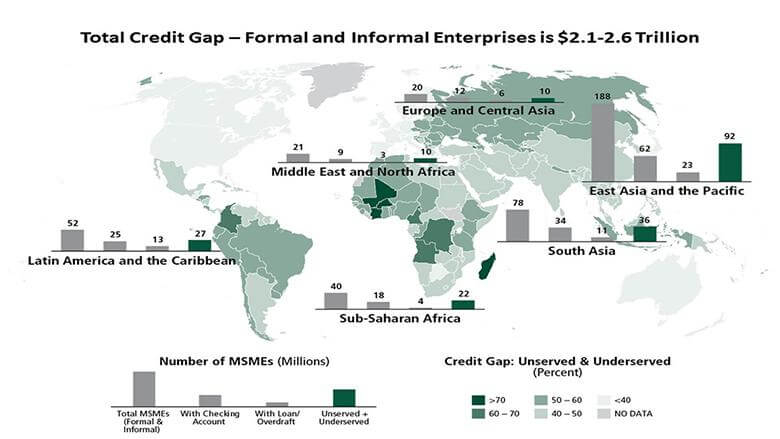

Depending on the size, structure, ownership and history of the business, and the bank they speak to, the banking options available to SMEs vary dramatically yet rarely suit the business. Application and set up takes too long, costs can be out of reach, credit repayments are inflexible.

As a business passionate about increasing financial inclusion for SMEs, Banking Circle recently commissioned MagnaCarta Communications to carry out research into these issues. The first report looking into the findings of the research was published in June 2019 – ‘Financial Inclusion for Europe’s SMEs: Building a Circle of Trust’.

A second report – ‘Circle of Trust or out of the loop?’ – will be launched at Sibos 2019, featuring insights gained from some of the people working right in the midst of the challenges and the solutions hitting the market today. Speaking to these experts gave us first-hand insights and experiences, uncovering where changes are happening, where opportunities exist, and where barriers are beginning to come down to improve SME financial inclusion.

Expert Insights

Kent Vorland, CEO of SmartTrade, explained why SME financial exclusion is such a serious issue: “Smaller merchants tend to have normal people problems. By that I mean that the problem isn’t that they want money so they can go on holiday or go out for a nice dinner. They need their money so they can feed their family, complete the jobs or orders for their customers, or to purchase stock for the customer who has ordered it.”

Roger Vincent, General Manager (UK&I) & CIO of Trade Ledger added, “Above a turnover of £1m, banks will flick businesses over to corporate banking from retail, and that’s the gap where companies are massively underserved.”

Paul Townsend, non-exec director of Vitesse PSP Ltd confirmed: “There are certain client groups where a bank is perfectly acceptable and works well. Where it becomes more challenging is when the client becomes more complex, requiring FX and cross border payments, having a small balance sheet and a low number of employees. This brings concerns around cost-to-serve.”

Broadening SME banking horizons

Thankfully, providers are beginning to realise the potential held by the SME banking market. Valentina Kristensen, Director of Growth and Communications at OakNorth Bank said: “SMEs are still not top of the agenda for most financial services providers, but many are waking up to the benefits. They are realising that if they get an SME on board, they will be loyal and bring multiple cross-selling opportunities.”

As our report shows, bringing about real change and better financial inclusion for SMEs requires market participants to work together and develop joint solutions, collaborating to build bridges between individual innovations already in the market.

Roger Vincent of Trade Ledger added: “We are creating a new ecosystem of financial services providers, in partnership with other providers such as Banking Circle, to establish a new era of financial services which will better service customers and SMEs in the banking space. If we better serve the banking space through the incumbents, then the SMEs will benefit greatly as they can access the services they want.”

He also believes providers could deliver the solution now: “I can assure you, every financial institution on earth could put together a risk structure that would allow these companies to have access to that finance. And on top of that, all insurance companies in the world would be happy to insure those liabilities, so the risk wouldn’t necessarily even lie with those offering that financial inclusion. All in all, there is a long line of companies that would benefit from being given that level of flexibility.”

However, as our latest report shows, the progress and achievements will remain limited until further collaboration, communication and joined-up thinking become commonplace within the financial services industry. As with any ecosystem, it must be perfectly balanced in order to function effectively. The banking ecosystem must include all types of financial services providers, from big banks to start-up FinTechs. Only with providers working together in such collaboration, not a competition, will we see financial inclusion reach its peak.

Click here to register for the new Banking Circle Insight Paper which will be launched at Sibos 2019, and here to download the report ‘Financial Inclusion for Europe’s SMEs: Building a Circle of Trust’.