P2P lending is a way to source alternative finance and complex funding types for businesses seeking to raise finance. P2P lending started in the UK in 2005 with consumers borrowing from other consumers and it has been steadily increasing year-by-year with another record year in 2017.

Peer to Peer – What is happening in the market?

Today, borrowers have increased and widened across many asset classes and the direct lending platforms have increased to meet the demand.

In 2017 there were 100+ direct lending platforms facilitating more than £4.5 billion of lending:

Direct lending is often now used to describe P2P lending as a result of the increasing number of different lenders keeping up with this high demand.

After the financial crisis, banks were forced to follow strict regulations to stop fraud and corruption and this meant that they stemmed the previous flow of money to companies seeking loans.

After this, SMEs had to find alternative finance. A selection of SMEs recently named the biggest barriers to their success in the latest SME Finance Monitor (from insight agency BDRC) : 15% of the SMEs said it was legislation or political uncertainty that limited their business, 14% said the economic climate and 5% accessing finance.

P2P lending stepped in to fill this gap and offer SMEs a new source of liquidity and an alternative from the banking culture – and direct lending is continuing to boom.

In fact, Deloitte reported that 2017 was the strongest in five years for direct lending in Europe with $24.5bn raised.

Borrowers are attracted by the lower rates and quick loan decisions that the direct lenders can offer and lenders are attracted by the investment opportunity with higher returns and low volatility.

Why do SMEs turn to P2P lending to raise capital?

SMEs are increasingly turning to P2P lending platforms for working capital or to help them develop the business.

It is vital for the economy that our most promising businesses have access to funds to allow them to expand, develop their products, increase their staff and enter new markets.

P2P lending platforms are usually smaller and more agile than banks which means they attract borrowers and lenders who benefit from better rates and faster decisions.

1.Better rates

Banks battle with outdated technology and higher distribution costs (which are less cost effective for smaller loans).

Not only this, but P2P platforms have very low operating costs per loan compared to banks enabling them to offer better rates:

Borrowers are attracted by the lower rates and so P2P platforms are increasingly competing for borrowers on price – potentially leading to even further reduction in interest rates for lenders in 2018:

The absence of differentiated organisation strategies (the method used to find borrowers) may also cause a further reduction in interest rates as P2P platforms compete to grow.

2. Faster decisions

Many business owners become frustrated with slow loan applications at banks and this makes P2P lending an attractive option. If a company needs to quickly buy stock, there is no luxury of time – you need a quick decision.

It is crucial for the lifeblood of the economy for SMEs to obtain finance within days rather than waiting months which could make all the difference to success or failure. It’s a simple case of fast versus slow for SME finance.

3. Choices

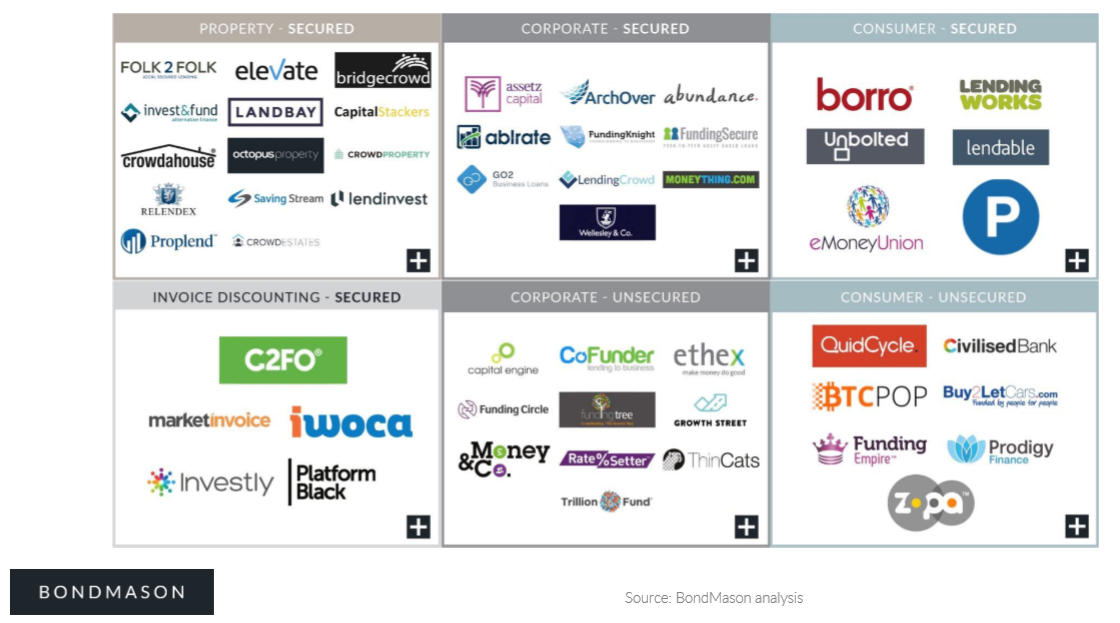

There are now over 80 successful direct lending platforms:

Not only this, but we are also seeing the big banks resurrect and return to offering loans in parts of the direct lending market leading some healthy market competition as the banks create better packages for their customers.

In 2018, there will likely be an increase in collaboration between P2P lenders and traditional lenders – with banks seeing direct lending as a source of capital.

4. Increasing quality

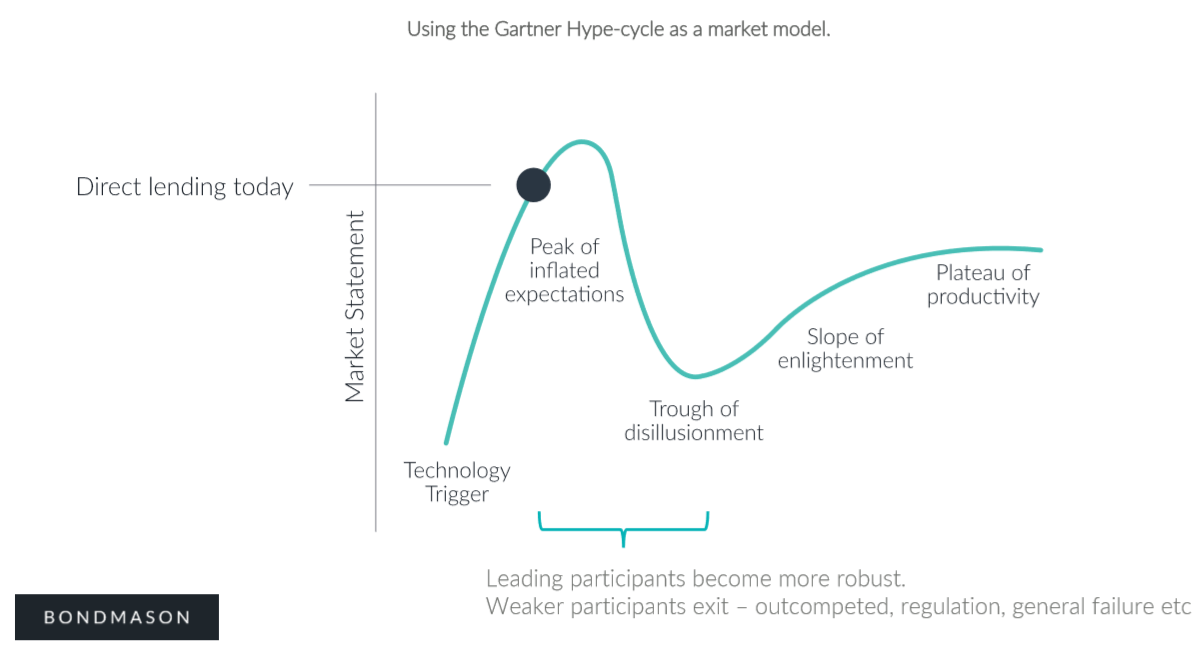

The future prediction is that the P2P lending market may slow down as there is a ‘flight to quality’ over the next couple of years. Better P2P lending platforms will outperform weaker platforms leading to their failure.

This will improve the service for borrowers and improve the reputation of the industry.

However, there is still plenty of room for the industry to grow there is still plenty of room for growth long term as reflected in the forecasting statistics.

5. Increasing expertise

P2P lending platforms are also increasingly staffed by financial experts rather than just being a tech platform and this also increases the attraction for borrowers with a better quality service.

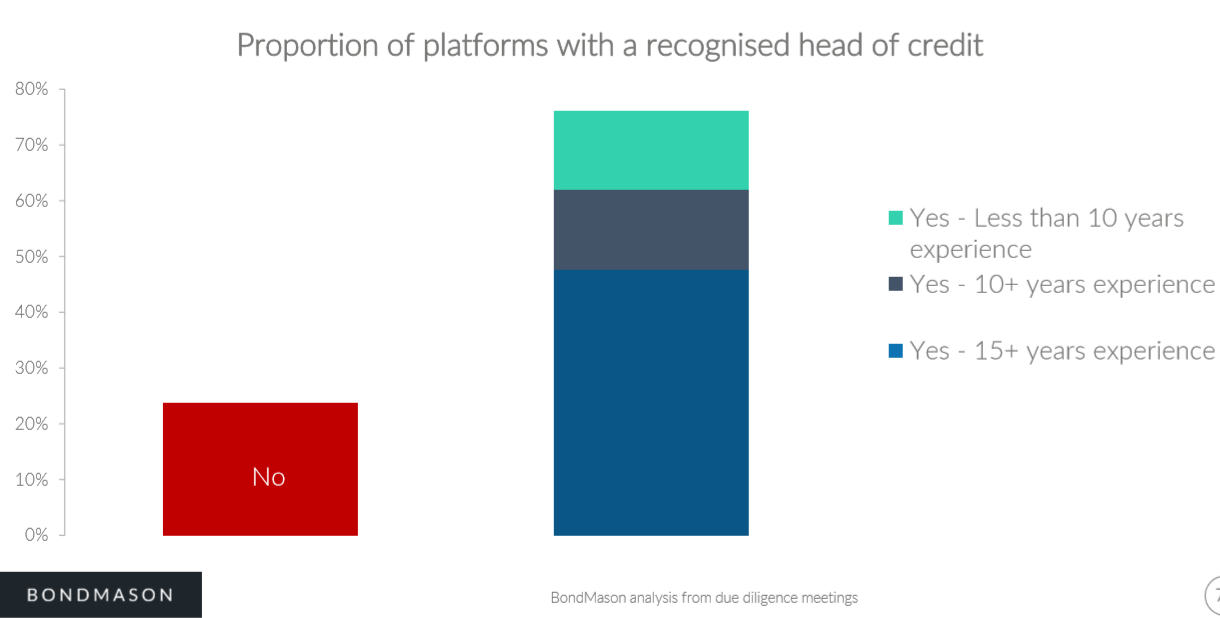

Nearly 80% of platforms now offer a recognised credit risk team. Most direct lending platforms are now managed by a head of credit with fifteen or more years of experience:

6. Increasing awareness of P2P lending

Awareness of direct lending and crowdfunding platforms amongst SMEs was 46% in the SME Finance Monitor report. This was up from 36 per cent at the start of 2017.

The media is also starting to view P2P in a better light as it becomes more mainstream and as the platforms evolve and mature – highlighted by the Bank of England in the latest financial stability report.

The introduction of regulation along with transparent credit data on borrowers means that more companies are seeing P2P lending as an attractive alternative.

However, although regulation of the industry continues to progress, diligent judgment is vital for companies going forward. The barriers to new lenders aren’t high and so the quality of different P2P lending platforms remains mixed.