- The trade insurance landscape extends well beyond credit insurance, encompassing marine cargo cover, war risk insurance, political risk insurance, surety bonds, letters of credit, and reinsurance.

- Digitalisation is fundamentally reshaping TCI, with AI, API-driven ERP integration, and smart contracts reducing administrative burden.

- Reinsurance, though largely invisible to traders, underpins the entire system – enabling insurers to offer higher credit limits.

Overview

Author: Kerlijne Van Steen, Deputy General Manager, CPRI & Surety Underwriting, Credendo

International trade exposes trading companies to a wide range of risks: non-payment by buyers, political instability, fait du prince, contract non-performance, or cash flow constraints.

100 years ago, the industry only had two financial tools to navigate volatility: the del credere and the letter of credit. Now, traders navigate multiple instruments, including whole turnover credit insurance, political risk cover, and trade finance solutions, which can be combined to protect and enable deals. Given the scale, complexity and financial exposure of international trade transactions, no single player can absorb and manage risks. Trade transactions often involve large ticket sizes and high concentration risks, sometimes across multiple jurisdictions; exposures which can quickly exceed the risk appetite or balance sheet capacity of a single institution.

Trade credit insurance (TCI) is not only a protection tool securing short- and long-term commitments, but also a facilitator of trade finance. By covering credit and political risks, insurers improve the credit quality of underlying assets, banks can extend higher credit lines or more competitive terms, and transfer the risk to credit insurers, all enhancing access to liquidity for traders. This creates a virtuous and resilient system. This link between insurance and finance is estimated to facilitate around €400-500 billion of financing annually, and over €9 trillion in shipments covered.

For most trade credit insurers, the approach is to provide a structured mix of solutions, tailored to the nature of the transaction, the counterpart risk, the geographic exposure… All the differentiated business lines have developed a complementary approach combining whole turnover insurance, single risk, catastrophic insurance (excess of loss), top-up cover, surety bonds, and guarantees that cover both sides and all stages of the trade cycle.

Trade credit insurers are moving fast towards deeper specialisation and more bespoke solutions where traders need coverage aligned with their specific risk exposure. Driven by data and AI, the entire trading ecosystem is morphing. This section will help demystify the main types of insurance and surety solutions available, offering a clear framework to support informed decision-making.

Specific types of insurance

Trade credit insurance

Author: Silvia Andreoletti, Senior Reporter, Trade Finance Global (TFG)

Different TCI policies cover different credit events, or causes for non-payment. Almost all policies will reimburse the supplier/ policyholder in case of the buyer’s insolvency or default; some policies also cover some political risks (for example, tariffs or government interference, leaving the buyer unable to pay on time).

The digitalisation of TCI

Author: Morgan Franc, CEO, Tinubu

While the purpose of TCI remains the same, digitalisation is reshaping its nature and reach. Historically, TCI has been a deeply manual, paper-heavy process.

Underwriter data – financial statements, payment histories, public records, credit ratings, and sector and country risk assessments – was acquired in stacks of paper. Underwriters had to evaluate risk by analysing this data page by page, clearing their desks as they tracked credit limits with physical ledgers. Trade references were collected by ringing up other suppliers, and delayed payments surfaced from local credit files.

Even once insurers traded paper for PDFs, cumbersome, multi-step processes and endless spreadsheets proved largely inefficient, with insurance brokers estimating manual tasks to take up around 40% of their time in 2022.

Consequently, these inefficiencies impacted businesses seeking insurance, either deterring them or subjecting them to lengthy, resource-intensive processes – impractical for small and medium-sized enterprises (SMEs), in particular.

However, according to McKinsey, five technology trends are transforming TCI today: distributed cloud infrastructure, network connectivity, trust architecture, next-level automation, and applied artificial intelligence (AI).

TCI is moving away from standalone portals and integrating with clients’ enterprise resource planning (ERP) systems directly through application programming interfaces (APIs), which allow multiple software applications to communicate with each other.

This provides real-time customer and credit limit lookups, end-to-end insurance cover applications, active monitoring of limit expiry or changes to payment terms, and generates alerts for invoice risk thresholds or overdue invoices. It also allows data to be encrypted and transmitted securely. Businesses are able to manage their credit insurance policy from within their own systems.

Insurance is also evolving beyond pilot stages when it comes to automation. Underwriters utilise probabilistic agentic AI models that view data as ever-changing and dynamic, and analyse patterns rather than isolated events and numbers.

Although AI is not yet at a decision-making stage in underwriting, it is actively used in submission intake. Automating submission intake enables AI to structure incoming information, streamlining a significant portion of the underwriting process.

AI is also heavily used in matching businesses’ risk profiles with insurers that have corresponding risk appetites, as well as in claim scope: simplifying processes associated with what a claim does and doesn’t cover.

Through digitalisation, policies are turned into smart contracts that replace complex, menial compliance processes, morphing into self-executing lines of code that interact with other contracts.

These shifts make TCI increasingly attractive for businesses. The fragmentation and inefficiencies of traditional TCI meant it was largely unsuitable for businesses that lacked in-house credit management.

Now, real-time data such as outstanding invoices are shared through integrated ERP systems, automatically adjusting coverage limits. With TCI visibly protecting against insolvencies across shared platforms, banks’ risk appetite grows, enabling them to lend more confidently.

Risk is now ultimately managed through digital networks, rather than by isolated actors trying to make sense of scattered data, page by page.

“What AI actually changes in credit insurance is the economics of all the administration. And there is a lot. Running a credit insurance programme is mostly repetitive, data-intensive work, assessing customers, managing limits, and keeping on top of the policy obligations, which is exactly the sort of thing AI handles well. Take it out, and the cost of cover drops noticeably.

It also makes the product far more configurable than it ever used to be. So instead of one model for everyone, a company can insure precisely where its concentration risk sits and automate the monitoring of the rest itself. Or just keep insuring everything, if that is what helps clients sleep at night. It really does vary from one balance sheet to the next.

That flexibility, in our view, is what finally makes credit insurance work for the companies that always wrote it off as too rigid or too costly.” – Burkhard Wittgen, Global Head of Multinationals – Credit Risk Solutions, WTW

Marine cargo insurance

Author: Silvia Andreoletti, TFG

Marine cargo insurance covers goods transiting by ship on oceans and inland waterways, insuring traders against loss and damage. Most insurance policies cover events like theft, damage while the goods are being loaded on or off the ship or due to rough seas, loss due to extreme weather, misplacement of goods, or losses caused by sinking, capsizing, or hull damage.

While shipping companies, freight forwarders, and logistics companies have their own insurance policies covering the ships themselves and their contents, traders usually also choose to take out marine cargo insurance for further protection. Marine cargo insurance is not mandated by law in most jurisdictions, although it is recommended. Exporters, importers, or both can choose to take out marine cargo insurance, but only one party is usually contractually obligated to do so; this party is set out by the Incoterms.

Each policy will cover slightly different things; some policies do not cover damage due to “acts of God” (extreme natural disasters like hurricanes or earthquakes) or war. Counterintuitively, some policies also cover those same goods while they are in transit via road, air, or rail to and from a port.

Pricing for marine cargo insurance often works slightly differently from other types of business insurance. Before signing an insurance policy, the policyholder and insurer agree on a valuation for the cargo being covered. This predetermined value is paid out in the case of loss or damage to the goods, avoiding debates about the valuation of the goods or their depreciation.

War cover

Author: Silvia Andreoletti, TFG

The risk of war, terrorism, and international conflict is a specific category in the political risk umbrella. While the likelihood of one of these affecting a transaction is traditionally very low, its impact can be catastrophic.

Political risk insurance can cover some of the risks associated with war in a supplier’s country, such as conflict-related asset seizures or delays caused by civil unrest. However, one of the biggest risks related to international conflict is damage to goods in transit, especially via sea.

War risk during transport is usually not covered by standard marine insurance. Firms can purchase a standalone marine war risk insurance policy to reduce risk in their most vulnerable areas of operations.

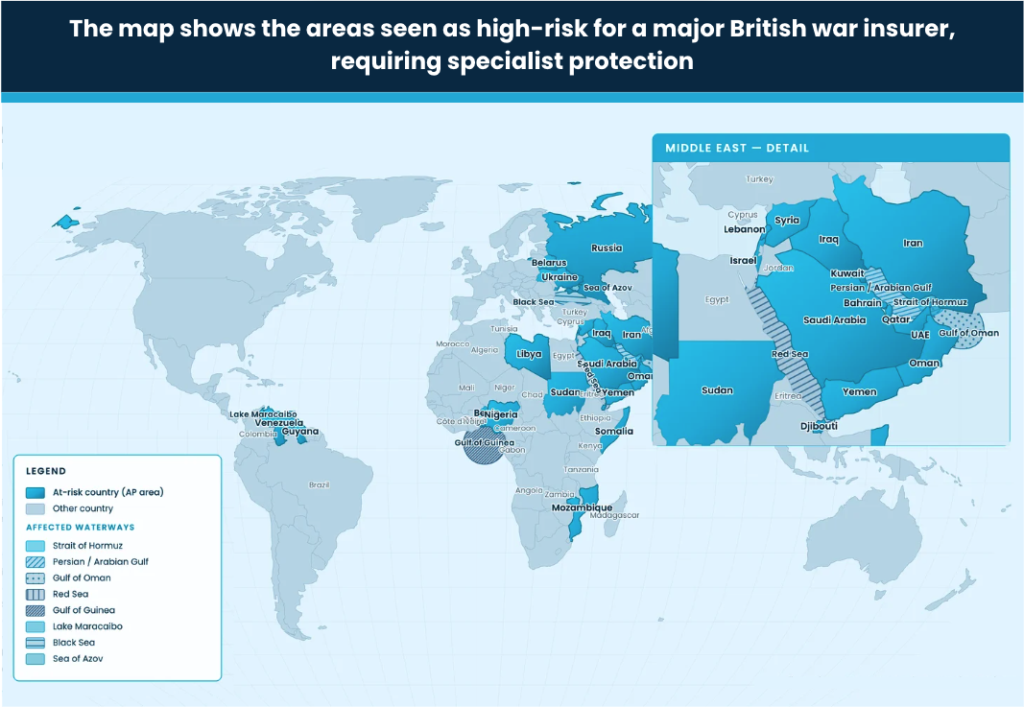

For example, companies would not take out war cover on trades that happen within the EU, or on ship journeys in a safe waterway like the English Channel. Instead, shipments that pass through risky waterways like the Red Sea, the Strait of Hormuz, or the Orinoco River in Venezuela will often be protected by marine war cover.

Marine war risk insurance is often an add-on to existing marine insurance policies, which cover ordinary damage to ships or their cargo. The additional policy specifically protects the company against losses caused by armed conflict: for example, the damage or capture of a ship (due to acts of war, terrorism, or sometimes piracy), loss or damage to its contents, and often ‘breach of warranty’ – when a ship enters a war zone in breach of trading warranties.

The cost of the policy varies greatly depending on the risk of the area the goods are transiting through: coverage in an area with an active ongoing conflict and a history of attacks on cargo ships will be far more expensive than in turbulent but less risky countries.

Source: UK War Risks

Case study: Marine war cover cancellations in the Strait of Hormuz

Author: Ellis Morley, Divisional Director, Howden

If we thought we had reached the peak of geopolitical instability, we were clearly mistaken.

Setting aside humanitarian considerations (the most important ones), and with the suffering of the victims of these conflicts very much in our thoughts, we would like to highlight what we consider to be the commendable performance of the insurance market: in this case, in relation to marine war insurance.

What has happened since the conflict in the Strait of Hormuz broke out?

To give an idea of the scale, prior to the first day of the conflict, an average of 140 vessels transited the Strait each day. From the day after the outbreak to the present, that figure has dropped to an average of 10 vessels.

How has the insurance market behaved?

At this point, it is worth explaining how these coverages operate in the event of a deterioration in risk, as is the case here.

In general terms, in both hull and cargo, insurers give a notice of cancellation with at least seven days’ notice. However, this notice of cancellation does not result in an immediate suspension of coverage, but rather in a revision of the premiums agreed prior to the event that could lead to cancellation.

While it is true that such increases can be multiple-fold, it is equally true that coverage remains available: the market remains undeniably active.

Beyond the obvious shift in risk perception, we are also told that one of the actuarial bases used in pricing – namely, the vessel’s nationality – has also been called into question in this instance, as vessels of many different nationalities have suffered the consequences of the conflict.

We would also like to highlight the importance, at present, of enhanced trade disruption insurance (which has now incorporated political risk cover).

Political risk insurance

Author: Emilia Levett, COO, BPL

In cross-border trade, credit and political risk insurance (CPRI) is typically used for larger, complex risks, where deep expertise in our client’s underlying transactions and the insurance product is essential.

As cross-border trade becomes increasingly complex and volatile, this level of support becomes even more vital as a strategic enabler. In turn, this volatility is signalling the importance and different applications of CPRI to a broad range of insureds who may not have engaged as strongly with the insurance market before now.

Indeed, we note an uptick in demand from financial institutions who have typically operated domestically or within a certain region as they look to mitigate trade-related risks and expand internationally.

Other ways to mitigate risk

Insurance isn’t the only approach to risk mitigation; suppliers have numerous options available to them. The next section outlines alternative strategies to mitigate risk, comparing their offerings with that of TCI.

Surety bonds and guarantees

Author: Silvia Andreoletti, TFG

Unlike insurance, which is a two-way relationship between the supplier/ policyholder and the insurer, surety bonds link three players in an international transaction: the buyer, the supplier, and the surety bond company (usually an insurer).

Surety bonds essentially guarantee that all parties stick to their contractual obligations, and compensate the affected party if this is not the case. Surety bonds are used in all kinds of contexts, from construction projects to lawsuit appeals, to make sure contractors complete projects on time. In international trade, surety bonds serve a similar purpose to TCI in that they guarantee to the supplier that the buyer will pay on time.

If that doesn’t happen, the surety bond company will pay the supplier and later pursue the buyer for payment. Vice versa, if a supplier fails to deliver goods to the required standard or on time, the buyer can request payment for the damages incurred via the surety bond.

Guarantees are a very similar mechanism, but they are issued by banks, not insurance companies. Guarantees are promises by banks to cover a client’s contractual obligations (in the context of international trade, payment obligations) if it fails to meet them.

A buyer may take out a guarantee to reassure the supplier that they will be paid no matter what: if the buyer defaults or experiences financial difficulties, its bank will cover the shortfall.

Guarantees protect both parties in an international trade transaction: suppliers from non-payment, and buyers from receiving damaged goods or not receiving anything at all. To issue a guarantee, banks need to assess the creditworthiness of a client, as they are effectively taking on the responsibility to pay in its stead if it were to fail. For this reason, banks will often ask for a security or collateral when issuing a guarantee.

Some businesses prefer surety bonds to guarantees because surety bonds are separate from their existing credit limit with their bank, which may mean the company has a new source of liquidity without having to reduce its borrowing. The credit ratings of large insurance companies are also often stronger than those of banks, providing companies an added layer of security.

On the other hand, guarantees often cover multiple obligations or transactions, which can make them easier to use as an overall risk-management mechanism. Another important difference between the two is that surety bonds function on condition, while guarantees function on demand: payment is made under a surety bond if a specific condition (usually, the breach of a contractual obligation) is triggered, while a guarantee can be called in at almost any time the beneficiary chooses.

The basic purpose of surety bonds and guarantees is essentially the same as that of trade credit insurance: protecting suppliers against non-payment. The difference lies in the workings of these instruments, the parties involved, and the specific requirements of each mechanism, which makes it more or less suited to different types of transactions.

Trade finance mechanisms

Letters of credit (LCs), known as documentary credits in the US, are another common way to reduce risk in international trade. They function similarly to bank guarantees: an LC is offered by a buyer to a supplier, and effectively acts as a commitment that the supplier will be paid on time even if the buyer cannot make the payment.

LCs are a staple in the trade finance industry, and they underpin a massive proportion of international trade. They are a legally binding document recognised by 175 countries globally, and are formatted according to a unified international code – the UCP 600 – making them easy to interpret in almost any jurisdiction. Some countries, like Egypt, have even made it mandatory for importers to use LCs in international transactions.

Unlike a guarantee, LCs involve four players: the buyer, the supplier, the issuing bank (the buyer’s bank), and the advising bank (the supplier’s bank). LCs also rely heavily on documents: often, the issuing bank will only pay the supplier once it has received documents certifying the goods have been delivered, such as a bill of lading (BoLs).

This makes the transaction safer for the buyer and its bank, but it can lead to delays if there are issues with the documents presented.

Reinsurance for traders

Author: Gloria Li, Senior Underwriter in Credit & Surety, Swiss Re

Why does reinsurance matter for traders?

Although reinsurance operates behind the scenes, it has a direct impact on traders. Spreading risk across multiple institutions enables insurers to offer higher credit limits and broader geographic reach in a stable and reliable manner.

This is especially important in cross-border trade, where transactions often involve high volumes, risk accumulations across multiple policies, and counterparties in unfamiliar or higher-risk markets.

How does reinsurance reduce risk in international trade?

Reinsurance strengthens the resilience of the entire insurance system in three main ways:

- Risk diversification: Instead of a single insurer bearing the full risk of a counterparty’s non-payment or the export country’s political risk, the underlying credit exposure is shared across multiple global players. This increases the resilience of TCI systematically.

- Capacity expansion: Insurers can underwrite larger or more complex deals (e.g. multi-buyer or emerging-market exposures) because part of the risk is transferred. This allows traders to secure protection even for high-value or higher-risk transactions.

- Market stability: Reinsurers absorb shocks from large losses or major disruptive events, helping insurers remain solvent and continue to provide cover during periods of stress, such as geopolitical tensions or global supply chain disruption.

Reinsurance also benefits small and medium-sized enterprises (SMEs) and new exporters, since it reduces the marginal risk of writing additional policies, thereby making insurers more willing to support new or smaller clients.