-

The rapid expansion of electric vehicles, clean energy, and AI is driving an unprecedented mining bonanza across Africa.

-

China currently dominates the global race for these critical minerals needed for the energy transition, by controlling significant production sites across Africa.

-

African policymakers are beginning to prioritise robust regulatory frameworks and financial instruments like deposit bonds to ensure sustainable mine closure.

As the global energy transition heats up, one continent that we must watch carefully is Africa. The continent is known to hold significant natural resources, especially some of the most sought-after minerals, centre of current geopolitical realignments.

This is currently evolving as the relentless, triple-engine mineral demand accelerator continues to churn. This refers to the three rapidly expanding sectors that drive growing demand for critical minerals: electric vehicles (EVs), clean energy technologies, and artificial intelligence (AI) and semiconductors.

At the centre of this is the green energy transition, guided by the 2023 United Nations Climate Change Conference (COP28) UAE Consensus deal that committed countries to reducing fossil fuel dependency in energy systems in a “just, orderly, and fair manner,” as well as tripling the use of renewables and doubling energy efficiency by 2030.

The next accelerator is the exponential AI data centre revolution, and the subsequent rise in energy demand. This is now further compounded by a surge in sovereign military-defence architecture, heavily reliant on drones and other technologies that require mining.

This can only mean one thing: we are on the cusp of an unprecedented mining bonanza, much of it expected to play out on the vast, underexplored African continent. This is coming into fruition through a new mineral diplomacy order – where mining and the lack thereof determine which country is courted by which superpower.

Chinese ventures into African mines

As the West seeks to out-compete dominant Asian suitors, Africa has been the recipient of numerous betrothal proposals.

Indeed, this is why the last decade has witnessed the worst explosion of mining adventurism in Africa. Mining companies are busy exploring, exploiting, and extracting precious rocks and soil matter amidst a tense, politically charged, and weakly governed mining sector.

For instance, Chinese President Xi Jinping’s 13-year-old Belt and Road Initiative has carved out a pathway that now has almost unfettered access to most African countries’ mineral resources.

China controls over half of global critical minerals production, with access to key sites such as Botswana’s Khoemacau copper mine, Mali’s Goulamina lithium mine, and Tanzania’s Ngualla rare earth mine. Chinese EV company BYD also controls six African lithium mines.

This explains the sheer dominance that China now has in the global race for the critical transition minerals – especially from Africa.

Chinese miners can be found deep in the trenches of the forested villages of South Kivu, Ituri, and Haut-Uélé in the Democratic Republic of Congo (DRC). Various cases exist where they have even been arraigned in local courts for illegal mining activities, as well as allegations of human rights violations.

They can also easily be found, relaxed and at home, deploying sophisticated heavy-duty machinery in informal artisanal and small-scale mines in the wide plains of Zamfara, Nasarawa, Niger, and Ogun States in Nigeria. As a result, rising allegations of illegal extraction, environmental degradation, human rights abuses, and labour laws contravention are abound.

They are also heavily involved in Zimbabwe, Ghana, Mali, Zambia, and South Africa, among many other countries, and they play a prominent role in the mining sector across the entire value chain.

From dominating African mines to dominating global clean energy

This is why the statistics emerging from Asia tell a story of sheer dominance. Last year, China’s internal electricity demand grew by 520 terawatt hours (TWh), with its generation from solar alone almost doubling with a 43% growth.

Electricity generation from wind power grew by 14% in 2025, as the overall increase in generation from just three sources (solar, wind, and nuclear) amounted to around 530 TWh, effectively meeting almost all the growth in demand.

Similarly, in 2025 alone, Chinese battery giants CATL and BYD held over 65% of the domestic market, which powers 70% of electric vehicles globally, controlling more than 80% of the solar supply chain and roughly 80% of all battery manufacturing. A significant chunk of the minerals required for these components originates from Africa.

Yet, Africa’s mining sector is only said to be taking off now, as many countries scramble to put in place regulatory and policy reforms to govern the sector. Of course, regulation always seems to be playing catch-up amidst increasing policy summersaults.

A new pan-African awakening?

Just last month, Kenya hosted the first meeting of ministers in charge of mining portfolios and ending raw mineral exports.

In June this year, both Kenya and Nigeria are expected to hold a second meeting in Abuja. The meeting will discuss a roadmap towards stronger continental collaboration, with many expecting a major policy announcement on value addition.

It seems that the continent’s policy makers and leaders are now taking notice, and with good reason. The sector is still nascent, yet the demand for minerals is skyrocketing, and Africa needs to ratchet up its systems fast so as to catch the windfall before it is too late.

Take Nigeria, for example. The country established its mining cadastre office in 2007, in accordance with Section 5 (1) of the Nigerian Minerals and Mining Act 2007 (which is now being amended).

A review of Nigeria’s electronic mining cadastre system reveals a fascinating insight: only very few mines have gone through the full cycle for the formal closure of their operations, while numerous minerals from the country are already widely circulating globally.

The pace for issuing licences and permits for new mines is rapidly accelerating, implying that continued informal, unsustainable artisanal and small-scale mining is ravaging the country.

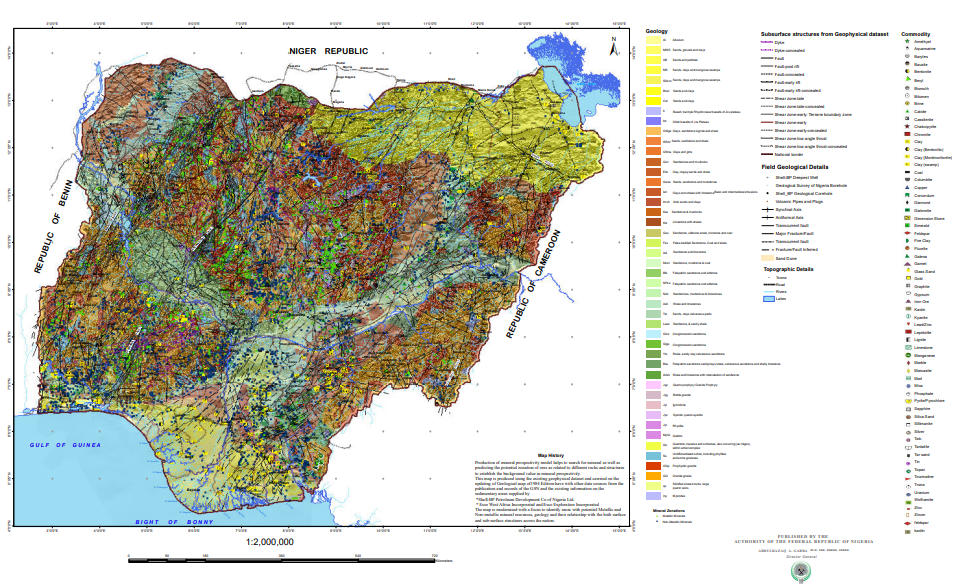

The mineral prospectivity map, issued by the Nigerian Geological Survey Agency, paints a picture of a trove of numerous minerals potential, just from the zonation of ores related to different rock structures. It makes one thing clear: the most populous country in Africa has its largest fraction of minerals, still untouched – buried deep in the bowels of the earth.

The situation in Nigeria mirrors that in other African countries.

In Kenya, since the pre-colonial gold mines and limestone excavations, the country’s largest mining expedition has been the Kwale Mineral Sands titanium project, which came into existence in 2013 and ceased operations in December 2024 due to resource depletion.

The company and the environmental regulator are now executing their formal post-closure management, and depending on how this final stage is executed, it could easily become a model worth replicating across the continent.

From South Africa to Tanzania, there are active exploration and extraction sites for these minerals. The Shimba Mrima rangelands in East Africa represent one of the most concentrated, mineral rich corridors in the world, with both the US and China locking their eyes into the area.

Of course, the DRC, another major mining epicentre, is home to numerous strategic mineral reserves – and is estimated to be holding roughly 70% of the global supply of cobalt, in addition to unknown reserves of coltan and more.

The environmental significance of formal closure

Historically, the romantic phase of mining has always been the beginning: the exploration, the discovery, the first dig, the precious stones, and the immediate influx of cash. But the true measure of a mine’s success is not how it starts, it’s how it ends. It’s not just how it impacts the economy, it is also how it affects the ecosystem.

Thereby, as we watch Africa’s fast-evolving mining dynamism, we must also radically shift our focus to the most critical, yet frequently neglected, dimensions of the mining lifecycle: the closure and post-closure phases.

When mining ends, operators and their business executives normally pack up – sometimes hurriedly – and rush to leave. If the mine closure is botched, the system crumbles as local communities lose their jobs and the environment crumbles.

Many environmental impacts, such as acid mine drainage, heavy metal leaching, and structural failures, can even extend to poisoning water reserves and devastating ecosystems for generations.

Africa will not survive another crisis, and unsustainable and unmanaged mine closures risks dealing the final blow to the continent’s fragile biomes. Already, the continent is ravaged by the triple planetary challenges of climate change, pollution, and biodiversity loss – it cannot afford a mining bonanza inducing even more disasters and catastrophes.

If left unchecked, the meagre economic windfalls expected from this mining bonanza can easily be swallowed by a century of ecological debt.

So, what must Africa do to avert such a scenario?

First, the continent must move to establish robust regulatory and policy instruments to govern the sector.

Second, massive investments in institutional and human capacity are required to enforce compliance. This is where the use of innovative financial incentives like environmental performance bonds and mine rehabilitation funds comes in.

Third, the mining bonanza can morph into an environmental tragedy. This imperative sits at the very foundation of the 2009 Africa Mining Vision (AMV), and must be actively prioritised today.

Source: Nigerian Geological Survey Agency

—

Beyond environmental, social, and governance (ESG) considerations, it’s important to embed deposit bonds at the heart of all mining regulations and laws in Africa. This is because the funds from the bonds would ensure immediate restoration, rehabilitation, and reclamation.

The longer it takes to act after a mine failure, the more deleterious the impacts become to nature and communities. Such instruments ensure that cash-strapped governments can step in and finance restoration immediately, though regulators must always remain vigilant against the moral hazard of companies treating the bond as a license to pollute.

Indeed, Africa is the bride in this evolving mineral bonanza but may well be left divorced after the honeymoon – when all her assets will be stripped away, leaving her destroyed and unable to fend for herself.

The thoughts expressed in this article are the author’s own, and do not represent the United Nations.