- A Barclays report argues that the UK government should strengthen support for SME exporters.

- Despite the UK remaining the world’s fourth-largest exporter, goods exports fell by 12% between 2019 and 2025 and the number of exporting SMEs dropped sharply.

- The report highlights limited awareness and restrictive eligibility criteria at UK Export Finance (UKEF).

The UK government could be doing more to support British exporters, especially small and medium-sized enterprises (SMEs), finds a Barclays report released today.

UK Export Finance (UKEF), the government’s export credit agency (ECA), plays a pivotal role in enabling trade, but its mandate and product offering should be expanded to reach more SME exporters, the report argues.

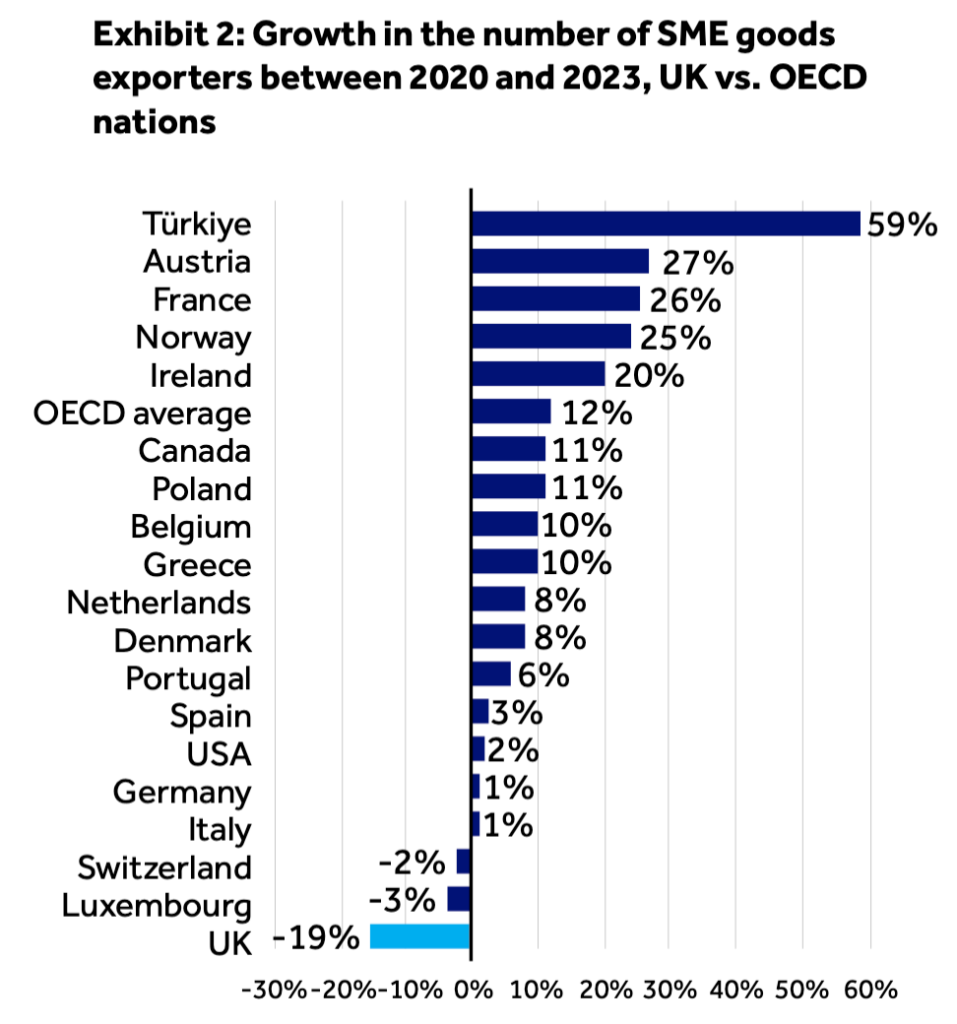

While the UK remains the world’s fourth-largest exporter, its trade growth has been slowing down in the past few years, and the country is falling behind its international peers. The UK’s goods exports dropped by 12% between 2019 and 2025, and the number of UK SMEs who exported abroad fell by 19% – or 23,000 – between 2020 and 2023 alone.

A global powerhouse lagging behind

Between Brexit, the COVID Pandemic, and tariff-related supply chain disruptions, it’s little wonder that UK exporters have been struggling in recent years. Between 2019 and 2025, the UK’s total trade grew by just 7% in real terms, compared to the over 20% average of the previous six-year periods.

SMEs, who account for 30% of the UK’s exports, bore the brunt of this slowdown: the SME trade deficit, already at £77 billion in 2020, nearly doubled, hitting £140 billion just two years later.

Source: OECD, Barclays report

This is not due to a lack of demand. According to previous Barclays research, UK exports are valued around the world, with overseas buyers willing to pay extra for products with a ‘made in Britain’ tag.

However, 95% of UK exporters surveyed for the report cited at least one barrier impeding exports, from regulatory complexity and logistical challenges to currency risk. Lack of access to finance was reported as an issue by 14% of respondents, while others cited a lack of knowledge and the fear of not being repaid by overseas clients.

The government’s new trade strategy and its small business plan, both released in July 2025, aim to remove some of these barriers, using export finance as a key tool. The new trade strategy raised UKEF’s capacity from £60 to £80 billion, and a bill currently being debated in Parliament would enable the Trade Secretary to raise this further, up to £160 billion.

James Binns, Vice Chair, Global Transaction Banking at Barclays, said: “As the UK looks to strengthen its export performance, now is the right moment to explore how government can make targeted, practical adjustments that would help UK companies – especially SMEs – access export opportunities, while continuing to safeguard taxpayers’ interests.

“Banks too have a role to play in getting this right, so we stand ready to do our part to help drive an export revival across the UK.”

Last month, five major UK banks partnered with UKEF to provide £11 billion in financing, 80% of which will be guaranteed by UKEF. But is all this enough?

UKEF’s image issue

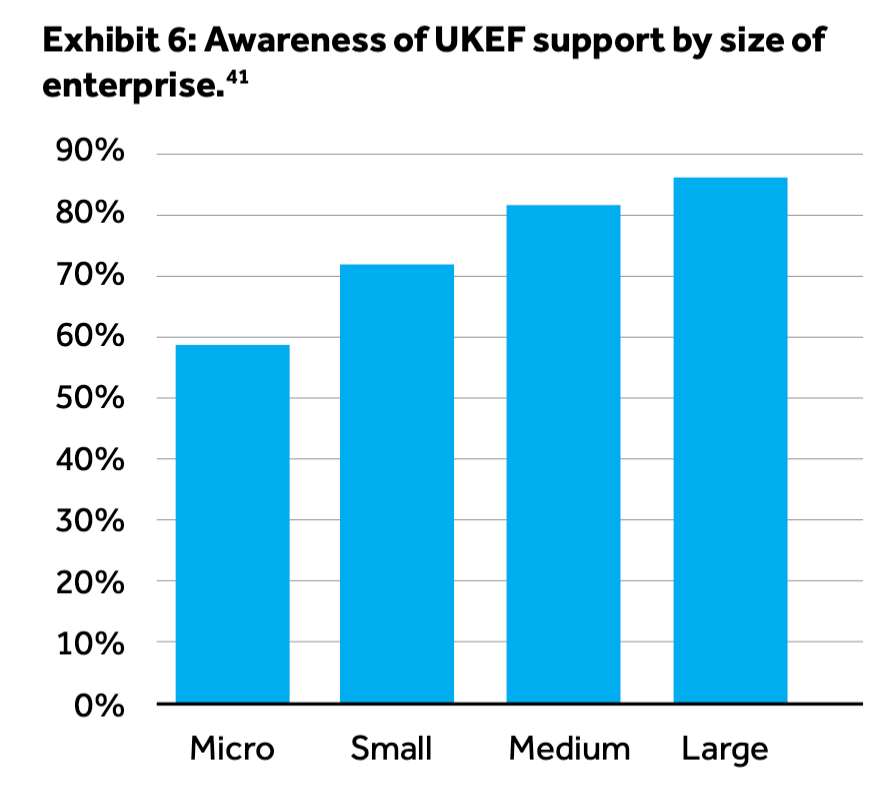

To be known is to be loved, goes the adage – but too few SMEs know about UKEF’s offerings to fully take advantage of its potential, the report claims.

According to the Barclays report, 41% of microenterprises and 28% of SMEs have not heard of UKEF, compared to under 20% of larger companies. Of SMEs who were aware of UKEF, nearly a quarter thought its support was unsuitable for them.

Source: Barclays report

This problem is not inherent to all export credit agencies: UKEF’s equivalents in South Korea, Germany, and Australia all have a far better SME/non-SME mix than their British counterpart, according to a 2020 report.

Despite recent improvements, including a commitment to double the number of SMEs supported – from 496 last year to 1,000 by 2029 – UKEF is still a long way from reaching all UK SME exporters.

Eligibility issues

One of the key barriers identified by the research was the eligibility criteria: of UKEF’s six criteria used to identify whether a firm can receive export financing, two – export contract requirements and the limit on levels of support – are significant hurdles for SMEs seeking financing.

The export contract requirement asks that exporters receiving most types of UKEF financing trade directly with a client outside the UK. This makes it difficult for suppliers of exporters to get the funding they need, which in turn makes it hard for exporters to make enough products to sell abroad.

A recent exception is the Critical Goods Export Development Guarantee, which would provide financing both to UK exporters who supply critical mineral products and their suppliers. More products like these are needed to strengthen the UK’s supply chains all the way through.

The second issue – one that may be harder to bypass – is UKEF’s maximum support levels. Currently, UKEF will only provide up to 80% support on its financing, a level mandated by the Treasury and intended to make sure firms and financial service providers have “skin in the game” in a transaction. However, this makes it difficult for banks to offer UKEF support to SMEs, which have less established credit ratings and require a higher cover, often up to 100%.

If guarantees covered more than 80% of exposure for smaller exporters, they would become a much more powerful tool to support SME exports, says the report.

More products, more risk, more automation

While the report identifies SME access as a key issue, UKEF must change more than that to become the trade finance engine that UK exporters need.

As one of the Treasury’s most efficient arms, and in light of its increasing funding, it’s only logical that UKEF should expand its product offering. Besides offering financing to exporters’ suppliers, which would largely help SMEs, UKEF should also develop a foreign exchange cover product to protect all companies from currency fluctuations, identified by many as a key obstacle to exporting.

UKEF should also increase sector-specific support as it has done with defence, clean energy, and critical minerals, and provide financing to firms in some of the UK’s other high-growth sectors such as life sciences and technology.

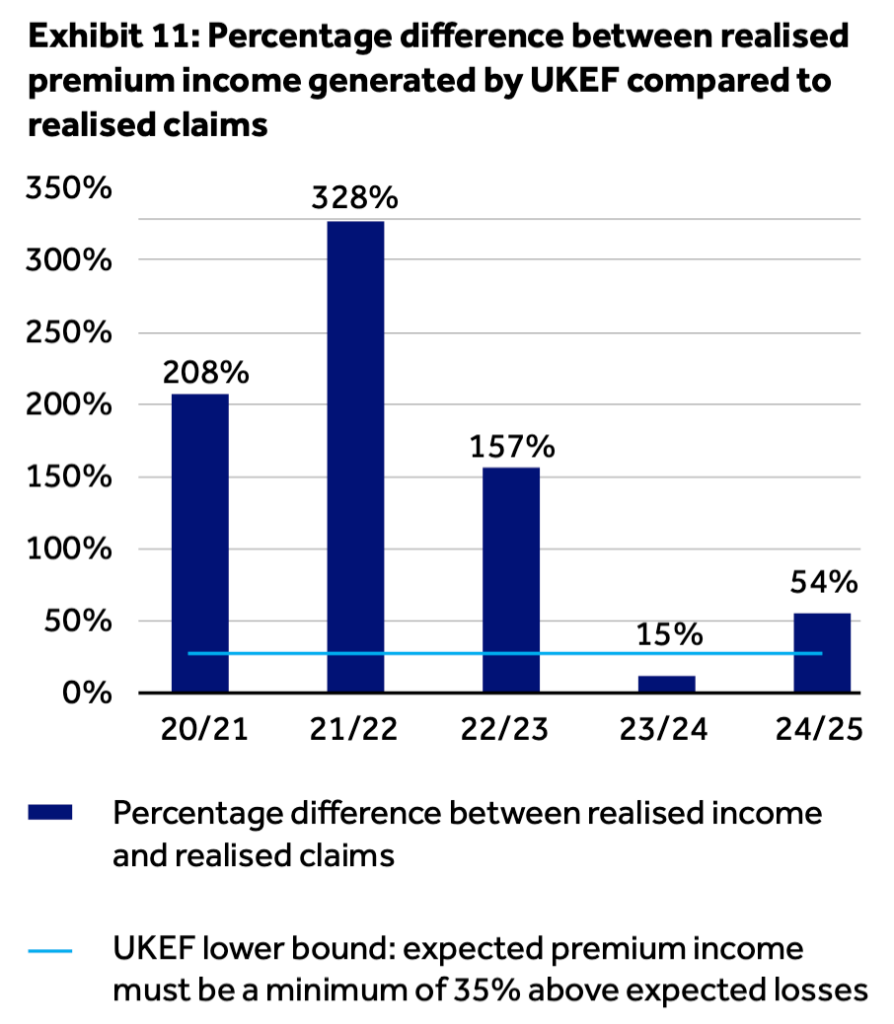

UKEF’s risk appetite and its 1.35 premium-to-risk ratio, which is set by the Treasury, is also widely perceived to be too cautious. This does not reflect the real default risk in the market, and instead is pricing out many would-be clients, especially SMEs.

Source: UKEF Annual Report 2024-2025, Barclays report

A lower premium-to-risk ratio (essentially, a slightly higher risk appetite) could still enable UKEF to turn over a profit while reaching more firms in need of financing.

Lastly, UKEF’s application and approval process should be simplified, finds the report, potentially by increasing the authority of automated underwriting. This would reduce delays and encourage more applications by reducing complexity.

—

UKEF is a key tenet of the UK’s trade finance, a government agency that has consistently acted as a force for good, facilitating trade at no net cost to the British taxpayer, and consistently turning a profit for the Treasury.

However, as UK export growth falls behind other Organisation for Economic Co-operation and Development (OECD) countries, UKEF must become more accessible, and evolve and expand to meet the changing needs of UK exporters – especially SMEs.

Marcus Dolman, Honorary Vice President, British Exporters Association (BExA), said: “Although UKEF is already one of the world’s leading ECAs, there is always room to make the best better. The report’s conclusions largely echo BExA’s own findings through our UKEF benchmarking work, and we look forward to collaborating with both UKEF and Barclays to deliver on these actions.”

In response, a UKEF spokesperson said: “We welcome Barclays’ report in raising awareness of UKEF’s products and services. In 2024/25, UKEF provided a record £14.5 billion in new financing to help British exporters of all sizes break into international markets and grow. We continuously listen to our partners and customers so we can provide the best support.”