on Trade Gaps, Growth and Jobs in Asia")

We caught up with the Head of Trade Finance at Asian Development Bank, Steve Beck. We talked about the newly published Trade Finance Gaps, Growth, and Jobs Survey. This year’s survey found that the global trade finance gap remains at around $1.5 trillion, nearly 60% of respondents expect the gap to increase over the next 2 years. Another key finding was that women-owned firms face greater challenges accessing trade finance than do men-owned firms. Meanwhile, small and medium-sized enterprises (SMEs) also face considerable barriers with more than 40% of SME trade finance applications rejected by banks. However, there is growing optimism that FinTech and digitization are potential solutions to bridge the trade finance gap, particularly for SMEs.

Featuring: Steven Beck, Head of Trade Finance, Asian Development Bank

Host: Deepesh Patel, Editor, Trade Finance Global

My name is Steve Beck. I head the Trade and Supply Chain Finance businesses at the Asian Development Bank. I’m living in Manila where the ADB is headquartered. I’m Canadian.

And also, you’re a world-renowned trade geek?!

World-renowned trade geek. I’ll put that on my business card.

What keeps you up at night?

Well, these trade tensions are concerning. Some of the discussions I’ve been having with clients and partners over the past couple of days here at Sibos has indicated that everyone sort of shares this concern around trade tensions and what it’s doing to the availability of finance for small and medium-sized businesses and their ability to grow the companies, employ more people and create growth in the economy. So that’s a concern. And we need to work together to try to ensure that some of these tensions don’t impede our efforts to create growth and jobs. Yeah, improve people’s lives.

Tell us about what the Asian Development Bank does some of the markets it serves?

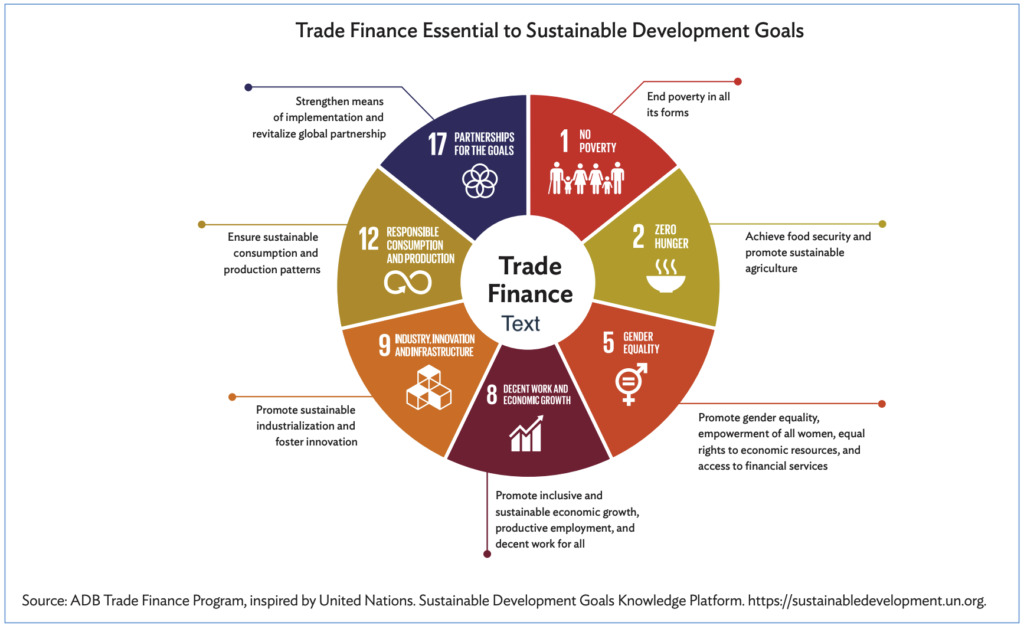

So the Asian Development Bank is owned by 68 different governments. And those governments created the bank back in 1966, to improve people’s lives – most of the world’s poor are in Asia – and the bank’s core mandate is to improve people’s lives and reduce poverty. So my role is to help close market gaps for trade finance. The United Nations put out a report on Development for Finance and stated very clearly that there’s a link between trade finance and achieving the Sustainable Development Goals. So it’s really important that the Asian Development Bank, working with its partners, commercial banks, and others, ensures and so on, and tech is able to close these gaps so that we can achieve our Sustainable Development Goals – and improve people’s lives of course.

And I guess, going into bit more detail on the mention of gaps ADB recently released its report, Trade Finance: Gaps, Growth and Jobs just a few weeks ago. Can you give us a quick executive summary of the report?

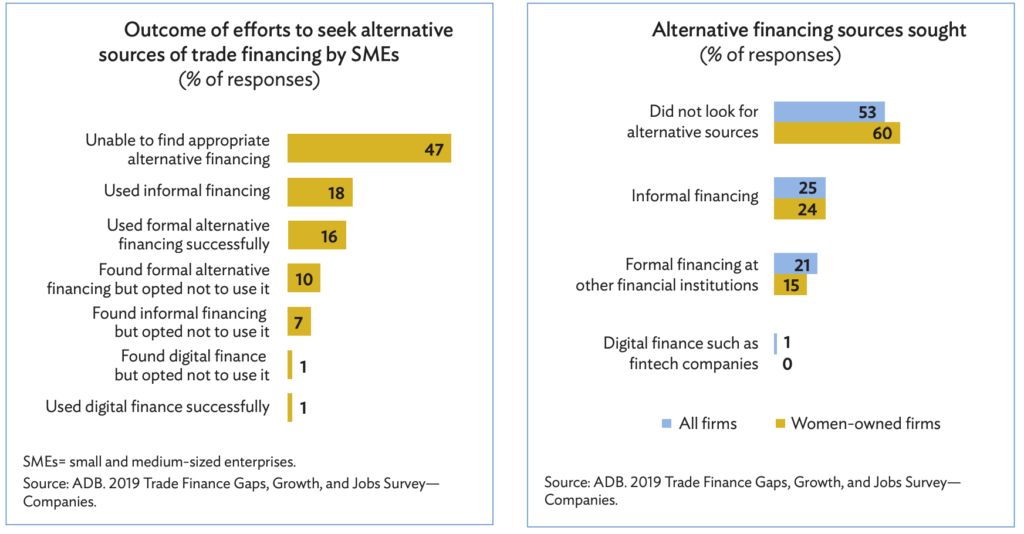

Yeah, yeah, sure. So, I mean, we found it important to try to quantify what the market gaps are for trade finance and why they exist. So we’ve estimated a $1.5 trillion market cap globally for trade finance, and it may come as no surprise that the bulk of that gap is in the small and medium-sized business market segment. And women-owned businesses have an even harder time accessing finance to support their trade ambitions. So that’s basically what the report found, and of course, there is a concern as expressed in the report that without sufficient levels of financial backing, especially the small and medium-sized entities, we’re not going to create the growth and jobs that are necessary to reduce poverty and improve people’s lives.

Yeah, yeah. And I guess going into that kind of SME space, what are some of the products that you are able to offer to SMEs at the ADB to help them grow?

Well, the Asian Development Bank is like a wholesale bank. So we don’t have branches and staff dispersed in all of our developing member countries. So it’s very difficult for us to interact directly with SMEs. So what we do is we operate through partner banks and other kinds of institutions to get to those SMEs.

We provide guarantees and loans to banks to support trade, including for SMEs. In fact, most of the 4500 transactions we did last year were in support of small and medium-sized businesses, we do that in partnership with banks. Yeah. We’ve also started a Supply Chain Finance business, which we’re in the process of growing, again, partnerships with banks. And their focus is on supporting SMEs in supply chains, again, with guarantees and loans. In addition to financing, we provide capacity building and technical assistance to provide companies and banks in our developing member countries with the knowledge that they need to acquire the resources to grow and create more jobs.

Another question that’s very close to our hearts is the diversity gap in the trade finance sector. What is ADB doing to support its partners to help promote diversity?

Well, I’ll speak to the trade part. I mean, the gender agenda, gender agenda is very important to the Asian Development Bank. Of course, women are more than 50% of the population. And it’s not just about women, it’s about economic growth overall, everyone benefits by having women more fully participating in the economy. So it is extremely important. And one just needs to look around Sibos to see that the vast majority of people here are men. So what we’ve done on the trade finance business, is we approached our partner banks and asked them if they would be interested in volunteering their HR, their human resource policies for assessment, and 19 banks participated. And we took those human resource policies and we had them assessed by gender specialists to understand how those policies could be enhanced so that they would result in attracting, retaining and promoting more women in banking, you know, and 50 of the recommendations were implemented. So it’s a, it’s been a really successful little pilot. It’s been a lot of fun working with the banks to do this, you know, and we’re in the process of expanding that to a number of different areas to work on the gender front.

Innovation is another very exciting aspect of trade, particularly around the digitalization of trade. We see a lot of innovation, particularly in receivables finance coming out of Southeast Asia, what’s your perspective of this and what is the ADB be looking at in terms of digitization?

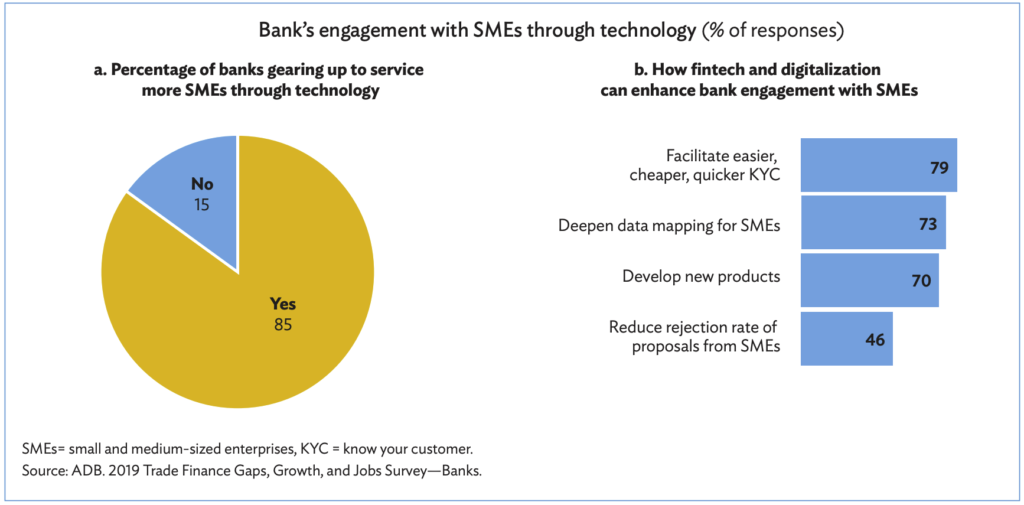

Yeah, tech is very exciting in terms of its ability to close market gaps, but you know, in the research that we’ve done, while there have been marginal gains, certainly there hasn’t been any sort of gain that has moved the needle in terms of closing gaps through tech. And that’s where we need to go. We need to support tech. So that it really does make a material difference in closing those gaps.

And I think there are three main things that are missing in terms of the sort of fundamental architecture for tech. What’s holding it back from being able to make that kind of a significant contribution. One is their lack of laws. So for example, you may know that most countries don’t have digital Bills of Lading something as basic as that codified in law.

It becomes very difficult to digitise trade if you know it’s not recognised in law. So we need governments to adapt UNCITRAL, there’s a UN body that creates laws for trade. We need governments to adapt some of those laws. So that we can, we can see tech, playing a much stronger role in that space. Second thing is we don’t have digital standards. We have lots of silos, and individuals sort of pilots and the blockchain or whatever it is operating independently from each other. And so what we’re in the process of doing now is creating with the Government of Singapore, a body that’s going to be housed in the International Chamber of Commerce. So it’s going to create the digital standards and protocols that enable interoperability between all of these different tech pilots. And then the third thing is around identity. We’ve been promoting the Legal Entity Identifier. Yeah. Which I think is really critical to moving the needle on gaps through tech. So if you have like an ocean of metadata that’s created by having a lot of transactions being recorded, including by SMEs, recorded digitally, you’re not going to be able to get the information that helps you lend more financing to SMEs, unless you’re able to take, you know, through an identifier, a unique digital identifier. To identify a grain of sand let’s that’s the SME in that ocean of metadata. So we’re very keen on the legal entity identifier being adopted globally.