- Critical minerals are essential for industries such as clean energy, defence and AI, but their supply chains remain highly concentrated and vulnerable to geopolitical risks.

- Although demand for critical minerals continues to rise, weak investment, price volatility and high development costs are slowing efforts to diversify global supply chains.

- Governments and industry must support new mining and processing projects through investment, partnerships and policy reforms to strengthen supply chain resilience and reduce market concentration.

“Everyone talks about the minerals. There’s so many”, US President Donald Trump said. “There’s no such thing as rare earth. There’s rare processing. But there’s so much rare earth”

The Trump administration has intentionally moved to end the US dependence on foreign states for critical minerals. The US is 100% import-reliant on at least 15 critical minerals, with 70% of US rare earth imports coming from China.

Trump’s speech above, made at the World Economic Forum (WEF) in Davos, Switzerland, in January 2026, came just a week before he announced Project Vault, a $10 billion initiative to establish a US Strategic Critical Minerals Reserve.

But what are critical minerals? Are they really rare? And why are they such a sensitive subject geopolitically?

Trade Finance Global (TFG) recently hosted the inaugural TFG Singapore, where they sat down with Anis Nassar, Head of Critical Minerals at the World Economic Forum (WEF), to discuss what makes a mineral critical, the existing monopolies, and the economic difficulties of breaking into the supply chain.

What are critical minerals and are they rare?

There is no standard definition for critical minerals. The US government’s most recent list names 50, whereas the UK government lists just 22, excluding a group classed as rare-earth minerals.

While each country is free to define a critical mineral, the definition broadly follows two main axes: application and supply chain resilience.

Firstly, critical minerals have strategic applications in sensitive industries, including technology, energy, semiconductors, aerospace, defence, and artificial intelligence (AI) data centres.

Secondly, critical minerals have vulnerable supply chains. That can be a lack of available volume in the short and long term, but it can also refer to concentration at the extraction, processing, or manufacturing stages.

A good rule of thumb is “if it’s used in strategic applications and supply is vulnerable, then it is often defined as critical,” said Nassar.

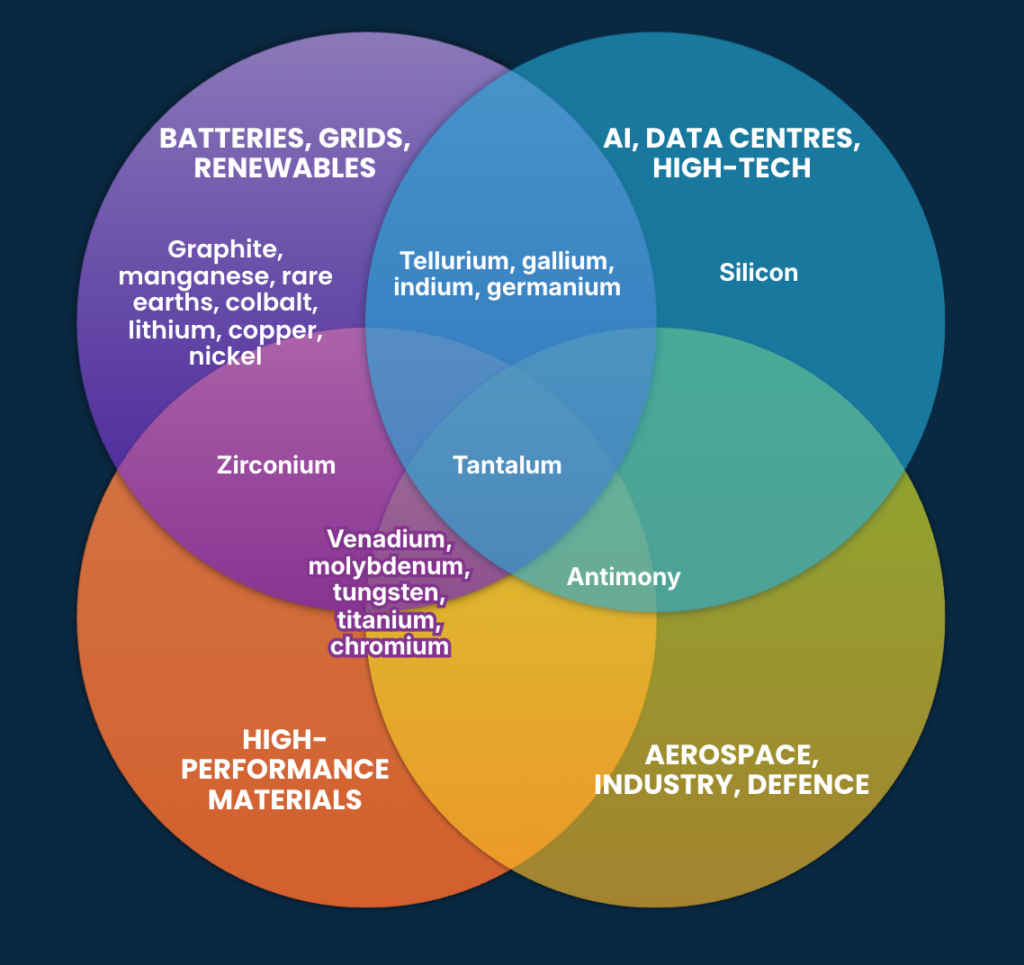

A diagram of some of the most common critical minerals and their industry usage. Sources: IEA, WEF

Rare-earth minerals are a subset of critical minerals. There are 17 naturally occurring rare earth minerals, the 15 lanthanides of the periodic table, plus scandium and yttrium. Though abundant throughout the Earth, they are widely scattered and rarely found in the necessary concentrations needed to make mining viable. That dispersion has given them the name ‘rare’.

Although known as ‘minerals’, rare-earth minerals are all metals, with distinct properties that have applications for lasers, glass, magnets, industry, and are found in everything from MRI machines to TV screens.

China’s geology dominates, occupying 48% of known rare-earth element reserves globally. Brazil follows with 23%, then India with 8%, Australia with 6%, Russia and Vietnam with 4%, and the US with 2%.

But China’s natural reserves pale in comparison with its production and refining facilities. The International Energy Agency (IEA) analysed 20 energy-related, multisectoral minerals that play a vital role across several crucial sectors. China is the dominant refiner for 19 of the 20 minerals analysed, with an average market share of 70%.

Given US geopolitical interests, it is reasonable to assume that efforts to diversify critical mineral supply chains are intended to reduce dependence on China.

However, in the global context, diversification should be understood as a strategy for building resilience rather than pursuing complete decoupling. The global economy is unlikely to decouple from China, nor would that be desirable. Instead, the focus should be on strengthening and safeguarding supply chains, while maintaining collaboration with China.

The flailing economics of critical minerals

The demand for critical minerals has soared. Electric vehicles (EVs), AI data centres, the rapid expansion of grid investment, and defence spending have all driven demand for critical minerals. The energy sector has accounted for 85% of all growth in demand for battery metals, which include lithium, nickel, cobalt, and graphite.

In 2024, Lithium demand rose by nearly 30% – compared with a 10% annual growth rate in the 2010s – and demand for nickel, cobalt, graphite, and rare earths increased by 6-8% in the same period. The energy sector accounted for 85% of the growth.

However, supply growth for battery metals has kept up with demand, leading to a decline in prices. Since 2020, supply growth has been twice the growth rates seen in the late 2010s. Following the sharp price surges in 2021 and 2022, prices for key energy minerals have continued to decline. Lithium has fallen by 80% since 2023

“Currently, processing is very concentrated for many minerals, and prices do not always reflect the cost of processing. Many smelters and processing facilities are closing”, Nassar explained.

Investment momentum is not growing at the necessary speed

Spending for critical minerals rose just 5% in 2024, down from 14% in 2023. Real investment growth was even lower, at just 2% when adjusted for cost inflation.

For many minerals, risk profiles do not align with investor requirements. High upfront capital needs, policy uncertainty, long development timelines, and weak revenue make projects difficult to underwrite.

For instance, despite the projected copper supply shortfall of 30% by 2035, the subject of much discussion, investment will fall short first: projections indicate a $250 billion gap by 2030.

The problem is that “different mineral markets have different economics,” as Nassar put it. Most markets have to deal with a long lead time from exploration, finding the deposits, and bringing minerals to the market. That already makes the economics complex.

But emerging markets, such as the lithium market, have high price volatility on top of that, so price stabilisation tools like price floors or offtake agreements are helpful. In other, highly concentrated markets, such as rare earths, government procurement can bring stability and a long-term horizon to contracts.

Growth is occurring mainly in incumbent markets.

Despite the importance of diversifying the extraction and processing of minerals, growth is coming mainly from incumbent markets. For example, in 2024, the most recent growth from mining output stemmed from established producers: the Democratic Republic of the Congo (DRC) for cobalt, Indonesia for nickel, and China for graphite and rare earths.

The IEA’s 2025 report showed that the average market share of the top three mining countries for key energy materials rose from 73% in 2020 to 77% in 2024.

Market concentration in refining mirrored this pattern: the market share of the top three refining nations of key energy minerals rose from 82% in 2020 to 86% in 2024.

In fact, 90% of market growth for refiners is being led by the top supplier alone: Indonesia for nickel and China for cobalt, graphite, and rare earths.

That means the monopolies are big and getting bigger. And these market constraints make it extremely difficult for new entrants to step in.

“This concentration, the capex intensity of the industry, and demand uncertainty “create barriers for new entrants to come in and to put money in a process that might actually be losing money,” said Nassar.

Without new entrants, the critical minerals market is vulnerable. For battery metals and rare earths, suppliers outside the dominant producer can, on average, only meet half of the remaining demand in 2035.

A sustained supply shock for battery metals could increase global average battery pack prices by as much as 40-50%.

Yet, the broken economics mean there is a lack of new entrants needed to diversify the industry away from narrow supply corridors.

However, it’s important to note that for countries already supplying critical minerals, growing demand represents a significant opportunity to expand industrial capabilities. This is particularly true for African nations such as DRC and Mozambique, where the supply of critical minerals is considered increasingly important, is being amended to meet the demands of external processing facilities, and states are reclaiming sovereign control over the mining and exports of minerals.

In Mozambique, for example, the state recently banned the export of raw and semi-processed minerals unless there is an illustrated commitment to refining locally. The ban came just after the introduction of a new law requiring the state to have at least 15% of ownership of all mining projects.

Can we trade our way out?

For a resource so dependent on geography, there are only a few choices: uphold the vulnerable and narrow supply chains, build on-shore processing facilities and redirect market dynamics, or go to the source, either through partnership or by digging in your own backyard.

Nassar explained that in the last few years, we’ve seen a decrease in collaboration through the multilateral system, replaced by a more agile, interest-based coalition. A 2024 McKinsey study found that trade between ‘geopolitically distant economies’ is decreasing. Indeed, trade with ‘geopolitically distant economies’ fell 12.7%, 11.2%, and 9.6% for the US, China, and the European Union (EU)/ UK, respectively, in 2017-2025.

The tensions are exacerbated for critical minerals and their predominantly Chinese-dependent supply chains.

China has required foreign companies to obtain an export license from China to export components and assemblies containing China-sourced rare earth materials. The policy has given China greater oversight over the supply chain.

However, countries leveraging their natural resources may offer a tool to correct the balance.

The DRC announced a four-month export halt of cobalt in February 2025. The DRC’s initiative to curb falling cobalt prices drove a surge, which peaked at a 67% price increase since the announcement of the ban.

Zimbabwe, which has 9% of the global lithium market, imposed a ban on raw lithium ore exports in December 2022. Zimbabwe’s gambit to onshore refinery paid off, with a new lithium processing plant, backed by Chinese investors, nearing completion. Other players are interested. Saudi Arabia is looking to fund a port to complete the transportation supply chain.

“Some countries have dominant or leading positions in certain aspects of those value chains, and then they can use this leading position in any kind of economic negotiation, and this can create barriers to trade,” Nassar explained. However, that is also where the opportunity lies.

The WEF’s 2026 white paper on critical minerals sets out six policy instruments necessary to bridge the gap between market needs and investable projects: upfront capital support, offtake and demand anchors, risk mitigation, and tax and royalty mechanisms.

These instruments can reduce investment risk and the fiscal burden for projects, which could enable market entrants to set up.

In March 2025, Trump’s executive order hammered the need for domestic supply chains, prioritising mineral production activities over other activities on federal lands that hold critical mineral deposits.

However, the order also set aside dedicated financing, loans, and investment support and a directive to collaborate with private industry to ensure a stable and resilient domestic supply chain.

Dedicated financing and collaboration with international partners – not just a move to dig up new ground – could support market entrants at the earliest levels, and trigger a shift to de-monopolise the supply chain.

—

The game is rigged. Geographical luck has historically dictated which countries have had access to critical minerals, granting them monopolies. But Trump might have gotten something right: the game is in the process.

If we can avoid a flurry of resource nationalism and financial market entrants at the processing and production stages, there is an opportunity on the horizon to diversify and demonopolise this strategic, geopolitically sensitive market.