Lenders across the world are grappling with the trade finance asset class. In Singapore, a string of legal cases has left banks facing the prospect of staggering losses with the nature of the trade finance asset class, as secure and self-liquidating, facing an existential crisis. Year after year, from REI Agro to Qingdao to Hin Leong, banks get befuddled by the simplicity of the frauds perpetrated against them through fake invoices, photocopy bills of lading (BLs), and duplicate documents.

The fallibility of paper documents is often blamed as the source of the problem, but sometimes the real danger lies in the intangible aspects of human psychology behind decision-making processes. A compelling narrative and competitive lending market set against challenges in the verification of trades and finances can unwittingly lead a lender into a blinkered decision.

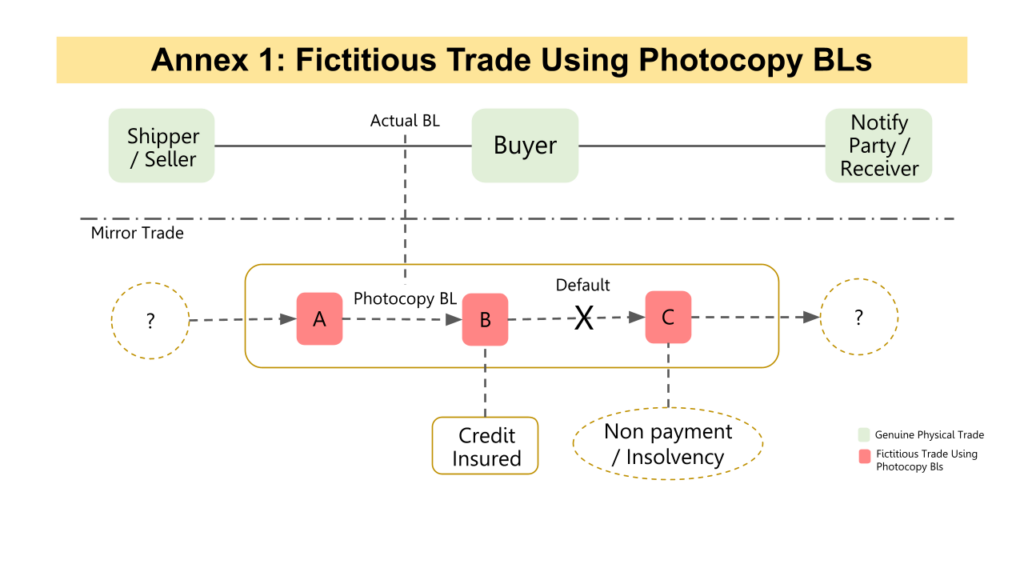

Far from sophisticated, trade fraud can be so breathtakingly simple that the mind does not address and arrest its possibility (see: Annex 1 modus employing photocopy BLs). The deception often occurs well before the fictitious trade peddled and lies in the all-consuming need for liquidity. Having worked on trade fraud cases for close to a decade, the common denominator in most, if not all, cases is that liquidity is the actual commodity being traded.

Cobbling a trade together can mean accessing the lower costs of borrowing in Dubai and Singapore and applying it elsewhere: for other trades, for working capital or even to unrelated investments in other sectors/geographies with high borrowing costs. Liquidity could also be transferred by loans between traders, dressed up as transactions where the physical goods are secondary or sometimes completely absent.

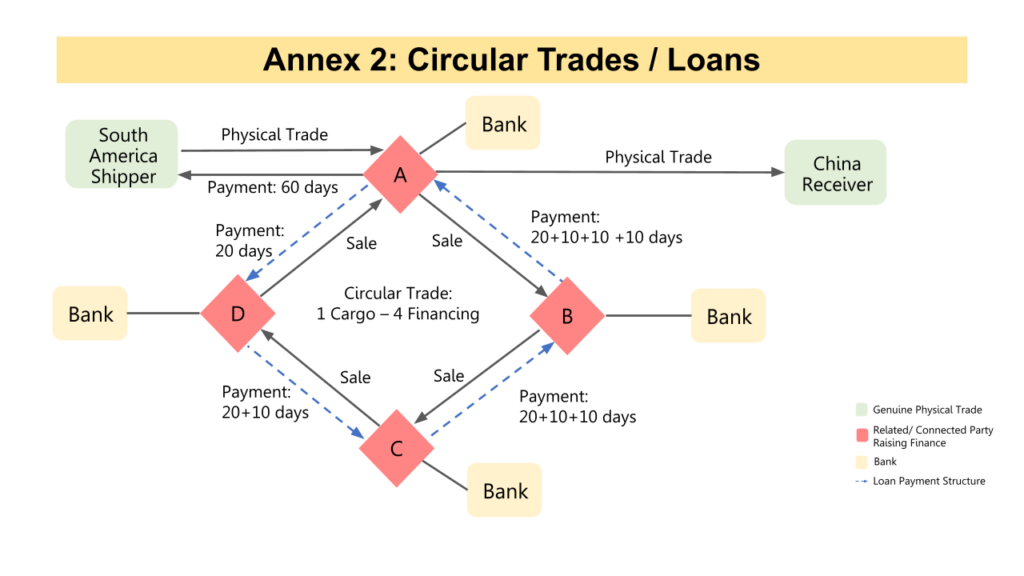

As it is, structured trades where trades are sometimes conducted forwards, backwards and then in circles, are deployed to seek financial arbitrage (see: Annex 2 where a circular trade between related companies creates multiple financing and might even be seen as a loan). The temptation to create such structures, even without the underlying goods, cannot be understated. Balance sheets soar, everyone benefits and, in any case, who will find out?

The balance sheet bias

The need for liquidity highlights the central role of having a positive balance sheet. Balance sheets provide a visible insight into the financials of the company, but also provide a far more powerful force that can make a compelling case: narratives.

The hype around an individual or company level creates a powerful self-perpetuating loop, where lenders might take the balance sheet as gospel and gloss over doubts. But balance sheets have historically proven to be poor tools to accept unquestioningly. The balance sheet is, at best, a snapshot of the company’s financial health at a point in time.

There are weaknesses in the document because it doesn’t give a clear indication of leverage. There is no distinction between structured trade and physical trade (the former arbitraging on financial positions rather than physical goods). Receivables, sometimes the only asset of a trader and the backbone of receivables financing, can often be difficult to verify or distinguish from a secondary loan from your borrower to its “buyer” (see: Annex 2). In a world where the balance sheet is supreme, there is every temptation, opportunity and ability to dress it up to fit the narrative instead of reality.

A healthy dose of scepticism towards the balance sheet would facilitate a critical analysis of the growth story of the company.

How did the company go from a $10 million turnover to $100 million in just a few years; how does a company borrow at 10% interest from private lenders to trade a product that makes a 1% margin?

The biggest blind spot tends to be when the lender is actually part of that growth story – this is how modest lines can turn into staggering sums without ever visiting the offices of their borrowers to test the financials against reality.

Can a handful of people run a $100 million balance sheet; can one trader be responsible for 10 different products; is the owner the sole decision maker? Lenders might deploy such checks at the onboarding stage, but reliance on “track record” might catch them off-guard when traders move from physical trades to purely financial structures over time.

Groupthink: Others can’t be wrong

Even when circumspection in the balance sheet starts to creep in, biases tend to find a justification. Trade finance is a high-velocity and competitive business where decisions need to be made fast. The involvement of other lenders is perhaps one of the most persuasive factors that can sway a decision, even if it is never articulated.

It once again provides confirmation bias as it diverts attention from ambiguities in the statement and encourages a logical fallacy that the involvement of other lenders is some form of quality assurance. This can also amplify the desire for involvement in what can loosely be described as a fear of missing out.

Interrogating the trade

The lure of an impressive balance sheet might divert attention from the fundamentals, i.e., the trade. Fraud flourishes in fragmented information chains: physical goods are placed in the custody of a third party, such as a vessel carrier or warehouse operator, while the trades are being conducted on paper with the passing of title documents by traders using financing.

It is this disjunct which lies at the heart of most trade fraud. Shipping documents can only tell you information relating to the start and finish points of the journey but it is the mid-point of the trade where fraud can occur. When we investigate trade fraud, we painstakingly piece together the actual movement of physical goods from shipper to receiver. That knowledge shouldn’t just be the purview of litigation lawyers like myself, but would be better placed before credit and risk committees prior to a lending decision.

More importantly, interrogating the trade is really ensuring that each party in the trade can justify its role in the chain: why is a small trader inserted as a sleeve in between two large traders; why are trades being conducted in circles; what has the trader done to verify title back to the shipper listed in the BL?

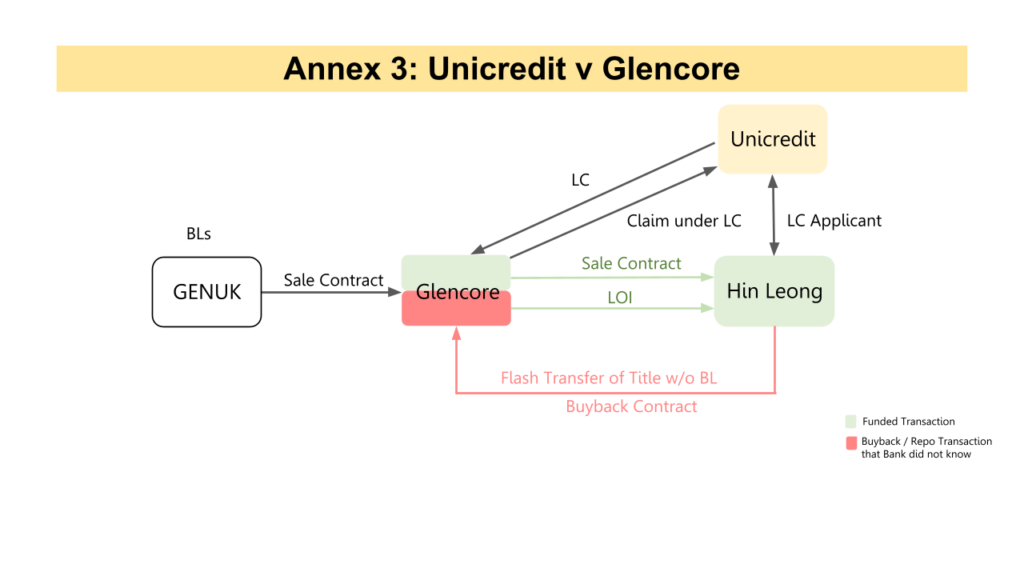

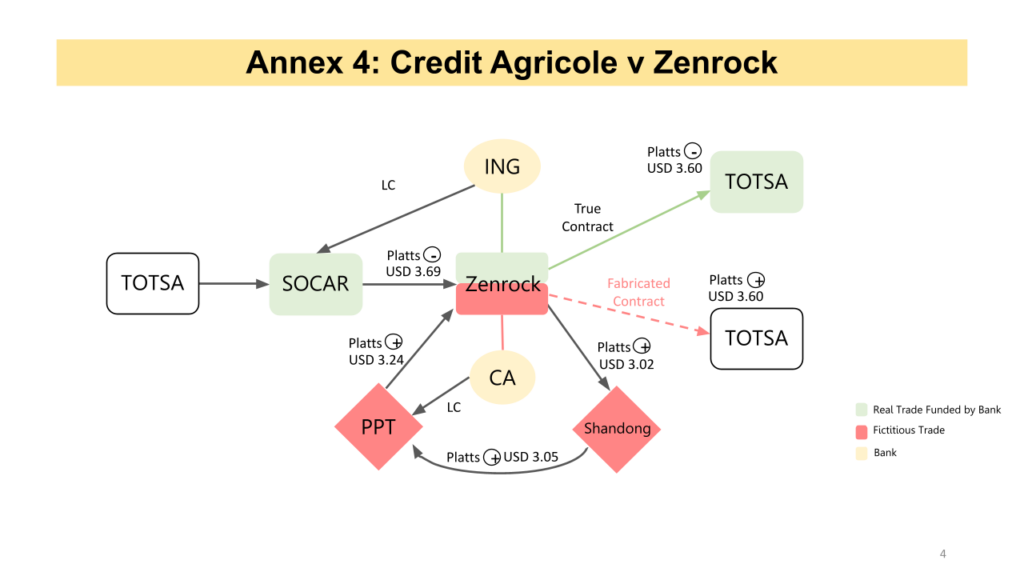

In two recent cases in Singapore involving letters of credit payments by Credit Agricole and Unicredit for trades involving Zenrock and Hin Leong, financing a segmented trade flow without clear visibility of the full trade flow left the banks exposed. Credit Agricole was left paying out on a fictitious double-financed trade by Zenrock, while Unicredit’s weakness appeared to be its unawareness that its borrower, Hin Leong, resold the goods back to the seller in a flash title repo transfer (see: Annex 3).

Interrogating the trade needs to be a dynamic process rather than a static assessment, as savvy traders are able to have their trades under the radar, for example, by reducing the shipment size or cargo value to the right price to avoid enhanced due diligence.

Testing your security

The hallmark of trade finance is its self-liquidating nature. Holding title documents such as BLs should give the lender a right to possession of the goods, and the failure to deliver the goods can lead to a legal case.

In recent misdelivery cases in Singapore, banks have found it less than straightforward to enforce their security of BLs through misdelivery claims against shipowners. Both SCB and OCBC were unable to convince a Court to get a summary judgement, as the Court believed questions on the banks’ treatment of the BL and security should be examined at trial.

The cases demonstrate the danger of treating the requirement of a BL as a checklist item, particularly when the bank may be aware that the cargo represented by the BL has been mixed into a new cargo or even discharged at the time of issuing the facility. The BL isn’t just a document to be kept in a folder – as a security, it needs to be constantly tested in case enforcement is needed.

Poor investment choices aren’t limited to trade finance. But trade finance often presents an intoxicating mixture of invincible individuals, glamourised financials and compelling narratives that play on our bias and divert our attention from the substance of the trade and the credibility of the narratives being peddled. The solution is not in stopping trade finance but by creating enough checks and balances that address the fallibility of the human psyche as much as the robustness of the trades.