- Corporates face the same sanctions liability as regulated firms, making it essential to use contractual audit rights to verify counterparties rather than relying solely on trust.

- Increasing global sanctions enforcement by authorities such as OFSI, OFAC, and the EU means failing to verify supply chains and payment flows creates significant legal and financial risk.

- Exercising audit rights helps organisations detect issues like trade-based money laundering, deceptive shipping practices, and opaque payment structures before regulators intervene.

From ancient Mesopotamian clay tablets to the emergence of global trading hubs in Singapore and Hong Kong, for centuries, trade finance has been built on trust. Commercial relationships, reputation, and routine documentation make up the connective tissue enabling goods, capital, and risk to move across borders.

But today, that foundation is shifting, and the failure to verify what counterparties tell you is becoming a structural weakness.

Banks invest heavily in due diligence because they are regulated and continuously supervised. The assumption that corporates are bystanders is dangerously outdated. Most commercial, distribution, supply, agency, and financing agreements contain information provision clauses, sanctions, warranties, and explicit audit rights designed to illuminate counterparty behaviour.

In sanctions enforcement, corporates face the same strict liability penalties irrespective of their regulated status. Being ‘unregulated’ is not a defence. The practical implication is clear, corporates have access to the same tools to verify claims, interrogate controls, and test counterparties, and, where they are regulated, the expectation is higher.

Regulated firms operate within established supervisory frameworks, with dedicated compliance departments and formalised governance. Unregulated corporates, by contrast, may lack equivalent oversight or maturity of controls, but this does not reduce their exposure to penalties.

And yet, audit rights remain chronically underutilised across sectors.

Why audit rights matter

Recent enforcement trends leave little room for ambiguity. The UK’s Office of Financial Sanctions Implementation (OFSI), the US Office of Foreign Assets Control (OFAC), and the European Union (EU) have dramatically increased investigations, penalties, and cross‑border collaboration, reshaping expectations for international trade.

- In the UK, OFSI continued to escalate enforcement in 2024/25 with 57 enforcement actions across corporate and financial services firms, demanding £500,000 in penalties, and more enforcement actions than ever. However, the biggest signal came from OFSI’s strengthened intelligence sharing with OFAC and the EU, and its proactive identification of sanctions breaches across global trade routes.

- In the US, OFAC, via its secondary sanctions regime, can penalise non‑US companies involved in transactions with sanctioned jurisdictions beyond American borders. Non-US companies operating in Africa, Asia or Latin America can be penalised if funds or goods indirectly support sanctioned actors, threatening access to the US financial system and US dollar (USD) clearing channels.

In this environment, relying solely on trust and contractual assurances, without ever exercising the right to validate them, is a growing vulnerability. The omission contributes to enforcement failures, as reflected in numerous sanctions cases where basic verification could have prevented breaches.

Audit rights, when used effectively, enable organisations to:

- Understand the commercial logic behind flows of goods, money, and vessels.

- Guard against trade‑based money laundering (TBML).

- Detect sanctioned‑fleet exposure, deceptive shipping practices, and routing anomalies.

- Validate counterparties, including non‑client and non‑contractual actors.

- Authenticate documents across the trade lifecycle.

- Escalate suspicious patterns before authorities do.

- Comply with relevant enforcement regimes

Yet, across industries, the same pattern persists, resulting in enforcement action which could have been avoided by following basic verification steps. Audit rights need to be applied as a strategic risk control and a source of commercial intelligence.

A trade finance reality no one wants to admit

Modern supply chains are no longer linear, transparent, or easily validated. They run through complex and often opaque ecosystems involving:

- Offshore booking centres

- Regional freight consolidators

- Multi-tier agents and distributors

- Third-party warehouse operators and inspection firms

- International banking correspondents and cash networks

In today’s environment of tightening trade barriers, the reliability of corporate assurances within these supply chains becomes increasingly fragile.

Against this backdrop, exercising contractual audit rights remains one of the most effective, yet underutilised, risk management tools available to companies. These rights are often the only mechanism capable of cutting through complex supply chain structures to validate counterparties, test controls, and ensure the integrity of trade flows.

Audit rights are not a legal technicality. In an era where visibility is shrinking, risk is migrating, and regulators increasingly expect verification, they are a practical necessity.

The compliance cracks your audit will reveal

Cross-border trade and payments routinely break down at the same predictable weak points: fragmented counterpart networks, opaque routing, and an over‑reliance on assurances that are never independently tested. Two recent enforcement themes show how these cracks become costly:

- Maritime sanctions evasion & the shadow fleet

The US Treasury sanctioned multiple Singapore-connected companies for facilitating Iranian oil shipments, engaging in ship‑to‑ship (STS) transfers, and deceptive maritime practices designed to obscure the origin and destination of crude oil. These actions reflect OFAC’s broader strategy to dismantle Iran’s ‘shadow fleet’ and disrupt global sanctions‑evasion networks.

- Payment chain and ownership failures

In the UK, OFSI imposed a £152,750 civil monetary penalty on Colorcon Limited, a UK pharmaceutical manufacturer, for “making funds available to a designated person” under the breach of the ‘Russia Regulations’ of 2019.

The US designations and the OFSI enforcement case both describe a familiar typology: obfuscation-based maritime sanctions evasion, involving STS transfers in high‑risk anchorages, dark fleet tankers, weaknesses in counterparty screening, payment assurance, ownership checks, front companies, and petroleum traders using deceptive shipping practices.

Would your current controls detect these patterns before the authorities do?

What could have been spotted:

In these instances, the compliance failures were not obscure, hidden, or unforeseeable. In fact, many of the vessels, companies, and intermediaries involved exhibited red flags that regulators and authorities, including those that OFAC, the Bureau of Industry and Security (BIS) and OFSI have repeatedly published and warned industry about.

These are exact indicators that commercially minded actors often overlook, but which a simple invocation of audit rights would have surfaced early:

- Repeated automatic identification system (AIS) in or near Iranian territorial waters

- AIS ‘spoofing’ showing falsified coordinates, mirrored tracks, or extended dark periods

- Unexplained port calls at known high‑risk terminals such as Kharg Island

- Multiple STS transfers involving:

US-designated tankers and tankers publicly identified as part of a ‘dark fleet’:

- Payments are being routed to companies with no physical footprint, no website, or mailbox‑only offices

- Letters of credit (LCs) or trade structures intentionally obscuring the origin of goods

- Pricing anomalies, involving discount structures commonly used to launder Iranian crude revenue

- Use of third-country intermediaries with no clear economic rationale

- Repetitive payments to UAE-based petrochemical companies linked to bitumen (a known Iranian origin product)

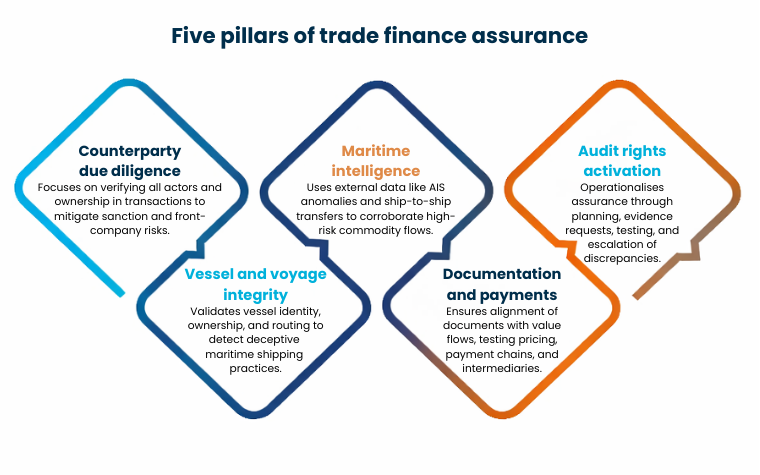

The five pillars of trade finance assurance

Regulators increasingly expect corporates and banks to demonstrate active verification across five critical dimensions of trade finance assurance. The barrier to this isn’t capability, it’s activation. An unexercised audit right is a blind spot, and an audit request that a counterparty cannot satisfy is a critical risk indicator.

Audit rights as a competitive advantage

Trade finance leaders state that non‑financial risk (fraud, sanctions, documentation risk) is now the top priority, surpassing credit risk.

Authorities are accelerating enforcement. Global supply chains are becoming more opaque. Corporate assurances are growing less reliable. Digital documentation, despite advances, introduces its own fraud vectors.

Banks verify because regulation compels them. Corporates should verify because liability, disruption, and reputational risk land on them equally. It means embedding verification checks into distributor selection, vessel assurance, and documentation pathways. For both, it means shifting from reactive compliance to proactive validation.

Trust is not a control; verification is a strategy, and audit rights are a competitive advantage.