- This article forms the fifth and final chapter of the whitepaper from Trade Finance Global (TFG) and the Bankers Association for Finance and Trade (BAFT): “From lenders to leaders: Banks in flux”.

- Digitalisation has been a hot topic in trade finance for years, but only recently has the industry as a whole stepped up to the plate.

- However, significant challenges remain, from inequality to fragmentation.

While AI’s impact on fraud detection falls short of what many had hoped, its potential is shining elsewhere. In the payments sphere, AI is enabling faster processing times and more precise transactions, and it can be a powerful tool to build resilience in international trade.

Digitisation as a whole is being embraced by banks and corporates, with growing investments in AI and new technologies, but it is still far from fulfilling its full potential. Challenges like fragmentation, a lack of interoperability, widening adoption gaps, and cybersecurity concerns are stalling progress around the world.

There’s more to tech than just AI

Virtually every bank and corporate is investing in AI, both to keep up with recent industry innovation and in the hope of increasing internal efficiency. However, this doesn’t come at the cost of other technology projects, even in a macroeconomic environment that encourages cost-cutting.

“Digitisation and AI are complementary priorities for banks, not so much competing priorities; banks continue to invest in those areas,” said one participant.

AI use for banks and institutions is mostly divided into outward and inward-facing implementations. On the one hand, companies want to improve customer experience: for instance, payment infrastructure providers are using AI to improve their early fraud and anomaly detection capabilities and flag potential mule accounts or otherwise suspicious transactions.

On the internal side, banks are looking towards AI to improve productivity and free up resources. For example, AI can ensure payment messages go to the right place and incorrectly filled-out fields are fixed automatically, ensuring transactions go smoothly and quickly.

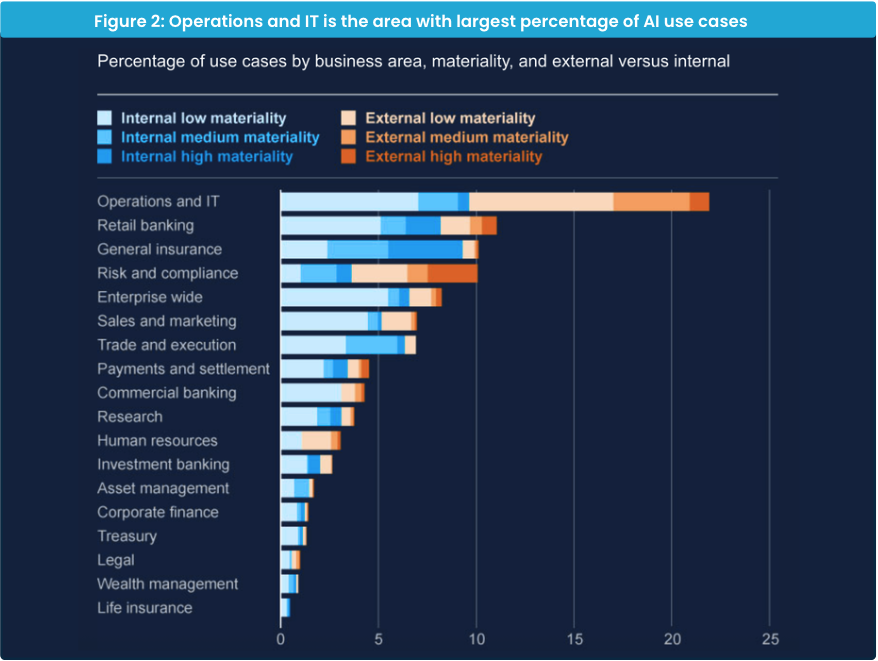

Source: Trade Finance Global (TFG), with data from Bank of England, 2024. Most banks still focus on internal uses for AI, with the exception of their Operations and IT departments.

Most of all, AI can help in repetitive but hard-to-automate tasks, like deciphering descriptions of goods in trade messages or other specialised communications. Using AI can help banks and institutions tackle long-standing pain points around efficiency and speed of manual processes.

Past paper?

After years of lagging behind the rest of the finance world, trade finance institutions are finally embracing digitisation – but mostly in isolation. Apart from some support from the International Chamber of Commerce (ICC), which five years ago launched a Digital Standards Initiative (DSI) to promote trade digitisation across the world, most digitisation pilot projects are driven by individual platforms and institutions, with little collaboration between projects.

In their search for interoperability, banks are increasingly looking to the government to drive the push towards digital trade documents, as the UK did in 2023 with the Electronic Trade Documents Act (ETDA). Other conversations, such as on digital identities, which could vastly improve KYC processes, have stalled, with AI now acting as the new hope for more efficiency in AML and compliance.

Increasing industry attention on blockchain and digital assets is also driving the conversation on digital trade documents, with smart contracts and tokenised trade documents potentially serving as a more practical and secure alternative to paper.

However, here, too, the issue is interoperability. Universally accepted smart contracts that remove much of the need for documentation in the first place would be ideal, but the industry has a long way to go in terms of interoperability before it gets there.

Islands in the digital stream

Corporate clients are reticent to go all in on digitising their trade flows, especially as they would be among the first in the industry; those that do, struggle to find viable platforms to handle trade documents with, and may in the end find that clients or intermediate players in the supply chain are still using legacy systems and won’t integrate with new solutions.

A lot of digitisation in banks is currently happening internally, which can drive growth up to a point, but will ultimately only lead to siloed systems unless it is integrated with the wider industry. Corporate clients, who may be using several banks across a range of global jurisdictions, increasingly want seamless and standardised service, but fragmentation – in anything from nation-specific fraud registries to contrasting local regulations – makes it hard for banks to provide for international clients efficiently.

On the other hand, regulation can be a solution if done right. “No matter how much we automate, if a fraction is automated, but then you still have to use a paper bill of lading (BL) to go to customs to clear your goods, it’s useless. So maybe that’s where the regulators need to focus energy: helping us to digitise that entire supply chain rather than continuously coming up with new regulations,” said one participant.

Trade digitisation would also go a long way towards thwarting money laundering and sanctions evasions, by making it harder, for example, to hide a good’s true origins or swap out the contents of containers mid-transit. This helps governments stop financial crime, taking some of the pressure off banks in the process. Cross-government collaboration is also crucial, especially as multinational banks struggle to align their own vision with that of the countries they and their clients operate in.

The dark side of digitisation

Ask any bank or trader in a developed economy what an ideal digitisation scenario looks like, and you might hear about digital-only ports, automated customs checks, and fast, paperless goods processing. However, the social impact of this full digitisation, especially on emerging economies, rarely features in the conversation.

Customs and goods processing are an important source of employment, which is even more crucial in developing countries that have only just started having a professional middle class. Jobs as customs agents, inspectors, or document couriers are highly coveted positions in countries such as India or Nigeria, providing stable government employment and a good salary. If digitisation and automation remove the need for most of those tasks to be done by humans, what happens to that workforce?

More importantly, digitisation is set to replace entry-level, menial tasks which would often be done by juniors in the industry. Without this crucial training, and while more senior practitioners prioritise cutting costs at every corner, will there be a massive vacuum when the current batch of senior trade finance professionals retire?

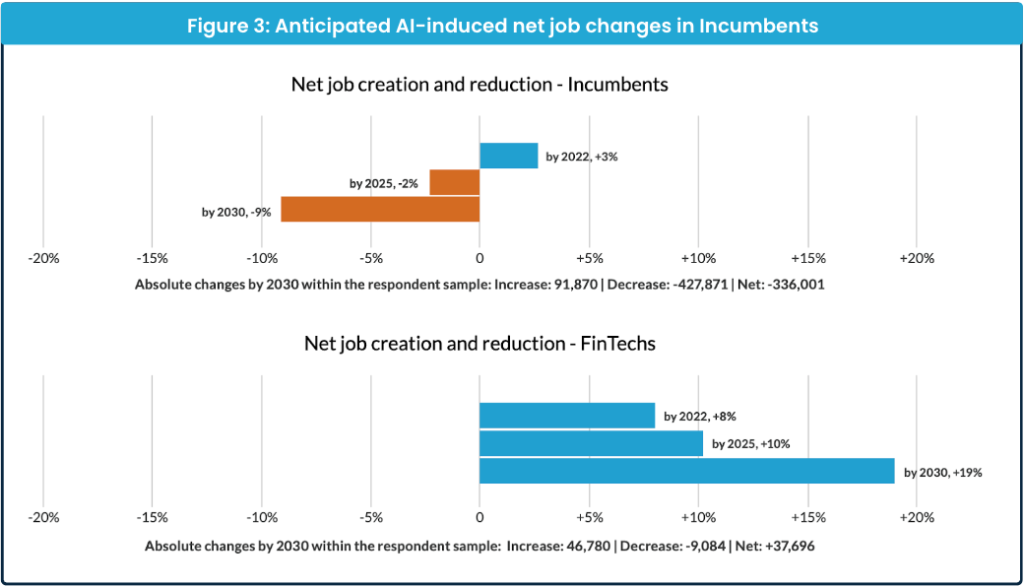

Source: Trade Finance Global (TFG), with data from Cambridge Judge Business School, 2020. While AI is widely expected to reduce the need for human workers in most sectors, it might have the opposite effect on fintechs.

On a practical level, too, digitisation in advanced economies may spell trouble for developing countries that are already lagging behind. “The move towards digitalisation [may] require infrastructure investments that will only widen gaps between emerging and more developed economies,” said one participant.

Even though much of the technology needed to digitalise is cheap and widely available, large-scale transformations may still be inaccessible for some investment-stricken countries.

Emerging markets superpower

In many ways, however, emerging markets are uniquely placed to win the race on digitisation. Countries on the other side of the widening digitisation gap feel the pressure to innovate more than anyone else – not just for the sake of progress itself, but to solve the real, practical issues of having fully analogue supply chains.

“When we look across Africa, some of the most exciting innovations are emerging from regions like East and West Africa. This is driven by deep talent pools, supportive government policies, and vibrant startup ecosystems that foster creativity and growth,” said one participant. Countries where there is less pressure for immediate innovation may feel threatened by developments like AI, while emerging economies are naturally more optimistic and enthusiastic about these developments because they’re seeing benefits almost immediately.

Emerging economies also have a step up when it comes to the implementation of new technology, like AI. “Emerging markets don’t have these legacy systems that they need to tear down and start again. This is not the case for every emerging market, or indeed every bank: but broadly, when they’re building these systems, they can start with technology like this embedded in every stage,” said one participant.

From a banking perspective, many new digital banks or fintechs can start with fully digital systems from day one, without needing to think about integrating legacy systems or retraining staff. Established banks in emerging economies, on the other hand, may be dealing with outdated systems that they lack the funds to modernise, further widening the gap.

—

In Pixar’s 1997 ‘Toy Story’, Buzz Lightyear came into Andy’s life promising to take him beyond human capability, “to infinity and beyond”. Woody, the cowboy toy of the past, looked on with suspicion and anxiety. He feared being replaced and struggled to understand this new, unfamiliar technology. Why bother changing legacy systems? But, as ‘Toy Story’ demonstrates, new capabilities and speed are obsolete without the judgment and resilience that human experience provides.