Established by national governments, Export Credit Agencies (ECAs) have broad mandates to serve their countries’ trade agenda. There have been two periods in the world of ECAs: those established before the 1990s, and those established after. The pre-1990s ECAs were mostly found in industrialised, set up post World War Two, with the mandates to support their countries’ exports into new markets. The newer ECAs which have come into being in more recent times, have had broader mandates to support both exports and imports. Many, especially in Asia, also have both insurance and lending operations.

Even under normal economic circumstances, ECAs have an important and active role in the economy. The International Association of Credit and Investment Insurers (known as the ‘Berne Union’) reports that their members provide cover for USD $2.5 trillion in exports annually, which is nearly 3 percent of the USD $87.77 trillion global GDP reported in 2019. During economic crises, as countercyclical actors, ECAs are tapped by their governments as critical policy instruments to bring support and facilitate recovery.

This pandemic is not ECAs’ first time being exposed to this kind of economic environment where they have been specifically mandated to play a supporting role. What has been the nature of their interventions in economic crises and then recovery? There are several patterns to discern over the past three decades:

- As a capital provider: during this current global pandemic, some ECAs have been tasked to provide a readily available channel for firms to access capital.

- As a market gap filler: during the Global Financial Crisis of 2008-09, ECAs stepped in as the private sector sources of risk capacity and financing retrenched

- As a market signaller: during the Asian crisis of the late 1990s, ECAs extended lines of credit to Asia governments, offering important signals to the market as a demonstration effect

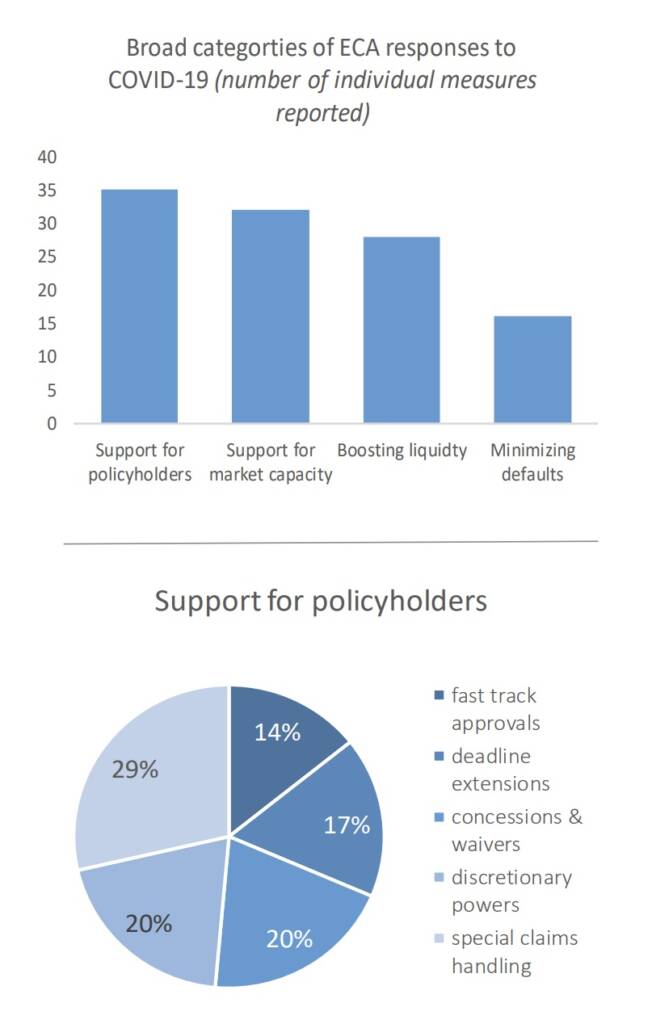

Since appearing in March last year, the COVID-19 pandemic has had significant economic implications to both international trade and domestic commerce, affecting nearly all economic actors. In response to the COVID-19 pandemic, ECAs around the world have not been hesitant to adapt their products and introduce new tools to help mitigate the economic fallout caused by COVID-19. Most ECAs have increased their flexibility and relaxed terms for policyholders, increased the timeliness on approvals and claims processing, expanded their risk appetite, and made concessions through waivers or flexibility on fees and premium payments. To avoid a liquidity crisis becoming a solvency crisis, many ECAs also have a focus on support for finance indirectly related to exports, including providing cover for working capital, pre-shipment finance, import guarantees, and bonds. By maintaining and expanding the availability of ECAs’ products and tools, many governments are able to provide some support for mitigating the economic effects on ECAs’ exporter clients and collectively on the global economy.

During the Global Financial Crisis of 2008, when liquidity and access to credit were hard hit, ECAs stepped in to fill the large and crucial gap left by the retracting private market of insurers and lenders.

During the Asian crisis, as a signal to the market to stem capital flight, ECAs were the first to extend credit into these markets facing temporary uncertainty, thus giving confidence that the underlying risks had (yet) not changed significantly and that these markets were still open for business.

These three roles – capital provider, gap filler, signal giver – have been critical in the midst of current and past economic crises and in helping to lead into recovery.

Where the world sits today, as vaccines are beginning to roll-out, hope for the start of economic recovery is growing. But what happens when markets have returned to “normalcy”? As we begin to imagine what a “new normal” may look like, ECAs will need to remember – as they must after each crisis – that private sector capacity and appetite will recover and it will be important that they remember to play in their lane, acting foremost as a catalyst role in global recovery and not getting too attached to a “hero” role.

“ECAs will need to remember to play in their lane, acting foremost as a catalyst role in global recovery and not getting too attached to a “hero” role.”

However, the need for ECAs to support clients through more flexible terms is likely to continue into the initial post-pandemic recovery period as businesses seek to reopen and/or restructure. In the short-term post-pandemic recovery, ECAs will likely continue to focus on maintaining support for their clients and national supply chains. In efforts to mitigate defaults, many ECAs are facilitating favourable restructuring either directly, or in conjunction with the private banking system. This restructuring can include deferred payment schedules or extended repayment periods, and waivers of some interest and fees. It’s again likely that ECAs will continue restructuring to support clients throughout post-pandemic recovery.

Looking toward the more medium and long-term stages of recovery, ECAs should turn their focus to facilitating a more resilient economy. ECAs should continue their focus to grow sustainability in strategic sectors where gaps have been exposed, such as healthcare infrastructure. ECAs should also stay aware of activity in the private market, taking steps to crowd-in as risk appetite and capacity undoubtedly resurges. From a development perspective, ECAs should also take this unprecedented crisis as an opportunity to adopt a “build back better” mindset for the long-term recovery, integrating the United Nations Sustainable Development Goals (SDGs) and the climate agenda into their strategies.