- This article forms the third chapter of the whitepaper from Trade Finance Global (TFG) and the Bankers Association for Finance and Trade (BAFT): “From lenders to leaders: Banks in flux”.

- Regulation is not a new issue for banks, and complaints about excessive regulations are as old as the banking industry itself.

- With the growing body of standards intended to widen financial access and promote the environment, however, banks are shouldering more and more of the burden.

On a Formula 1 racecar, faulty brakes can prove costly for lap time, track position, and driver safety. No matter how advanced the engine, how aerodynamic the front and rear wings, brakes play an integral role in both slowing the car down and in rotating and pointing the car so it catches the most momentum. Regulation should be viewed in a similar way.

In the environment, in tariffs, in AI, regulation dictates banks’ future plans. A swathe of growing, changing, and nation-specific regulation is driving just as varied a response – with banks, once again, playing a dual role of regulated and enforcers of regulation, all while advising corporations navigating the changing landscape.

Regulation, when done right, can fast-track growth and enable banks to look beyond risks towards creating a sustainable, shared future. However, even the most well-meaning standards and regulations – such as those governing payment languages – can end up widening the chasm between countries and institutions across the world.

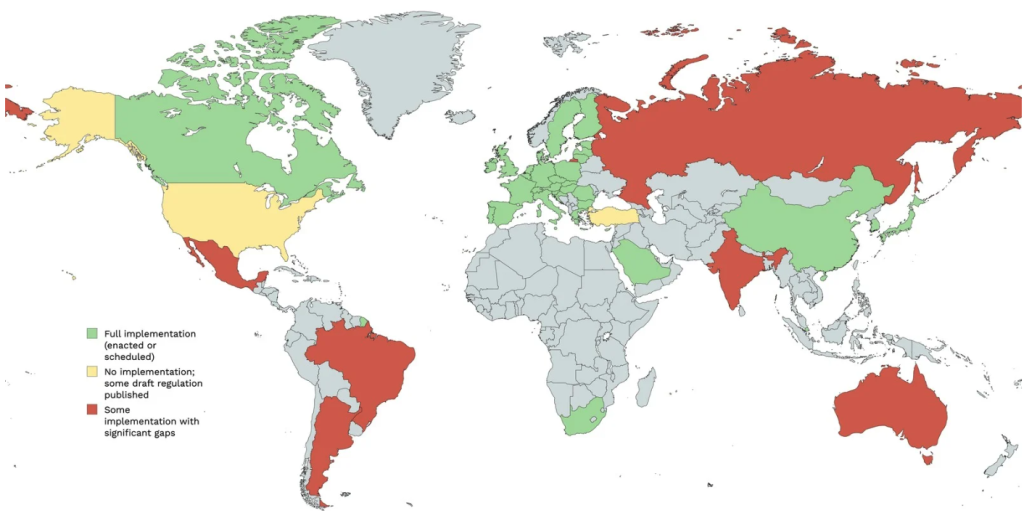

The Basel gap

Basel IV, intended to standardise banks’ approaches to credit risk and level the playing field across institutions, is sometimes doing the exact opposite. While the Basel IV standards are beginning to shape the conversation, if not come fully into effect, in much of the Western world, many jurisdictions are yet to start implementing them.

Source: Trade Finance Global (TFG), with data from BIS

In the US, the Basel rules are yet to come into effect fully, with the transitional period ending in 2028; UK implementation has also stalled on the back of US uncertainty. On the other hand, the EU and Canada are virtually done with implementation, while India, Argentina, and Turkey lag significantly behind. South Africa has fully adopted Basel IV, the only outstanding item is the output floor, which phases in up to 2028.

India, for example, has only implemented legislation for Basel IV’s revised operational risk framework, with no plans or draft regulations for the credit risk or credit valuation aspect of the standards. As of October 2025, only 40% of member jurisdictions have revised market risk standards in effect, despite a nominal implementation deadline of 2023.

Between banks, too, the implementation and impact of Basel IV can vary wildly, due to factors as trivial as differences in the makeup of banks’ books. Basel’s aspects that are detrimental to trade and trade finance will deal a much heavier blow to institutions that prioritise and invest in trade finance, potentially discouraging further investment. Industry associations have tried to make the case for rightsizing the approach to capital requirements when it comes to trade finance because of its stark difference from other corporate lending products, but this often falls on deaf ears.

One participant highlighted how the approach to Basel was initially relatively “broad-brushed”, painting nearly all banks’ activities the same way. When the trade finance industry tried to make the case that trade finance was different and should be treated as such, it only led to “an even more unlevel client fee” as the Basel Committee proved reticent to their arguments.

Advocates have made some progress in persuading individual regulators who are implementing Basel IV to rightsize their approach to trade, but this can be counterproductive for some large international banks.

“If you are a bank operating in multiple jurisdictions, you need to know how the local [Basel IV] approach is going to affect you versus your competitors in that market,” said one participant.

Bearing the regulatory burden

Beyond Basel, many types of regulation – especially client-related ones on money laundering or those countering financial crime – hone their focus on the trade finance sector to regulate issues that are characteristic of the whole of the industry.

Cross-border trade is susceptible to laundering illicit funds or evading sanctions. However, the issue is not with the use of trade finance, but with the complex nature of cross-border trade, of which trade finance is just one of the many moving parts. Instead of regulating trade finance with additional due diligence and know-your-customer (KYC) requirements, regulators should look to promote trade finance as a tool to actually mitigate financial crime risk, due to the end-to-end, granular visibility of the transaction it provides.

Regulations also tend to weigh on banks much more heavily than they do on other institutions. Banks, which provide the vast majority of the world’s financing, face stringent and increasing regulation, while non-bank lenders operating in niche markets face much laxer controls.

This is partially a result of regulators prioritising financial inclusion above all else, even at the cost of an unlevel playing field for established financiers like banks. In this case, banks and their clients often bear the brunt of regulatory developments like tariffs and sanctions: just as they were once effectively used as a police force against money laundering, banks are now being increasingly tasked with tariff compliance, a growing regulatory burden.

Verifying certificates of origin and transhipment routes for the trades they finance takes up valuable time and resources for banks, and makes them vulnerable to becoming a regulatory whipping post if things don’t go the right way.

Here, too, banks must wear many hats: on top of navigating tariff development themselves and advising clients on their next steps, they must also develop an almost real-time monitoring and compliance strategy to keep up with the changing regulations.

What does a better way look like?

Instead of increasingly specific standards for institutions, better regulation could look more like a model code, dictating appropriate behaviour and risk-taking associated with a transaction.

“If you focus on the behaviours and the risk of the activity rather than the character of the entity, then you’re more likely to get it right than having different regulations depending on what type of organisation is doing the [activity],” said one participant.

But the character of an institution matters especially for regulators looking to maintain structural economic stability. Banks are held to higher standards because the impact of a large bank, which also holds consumer deposits, collapsing is very different to that of a non-bank lender like a private equity company. Non-bank lenders are usually backed by investors with a higher risk appetite and lack the levels of systemic risk that banks carry with them, and so can avail of looser regulation and capital requirements.

In the long term, though, this can have a knock-on effect on the market that is hard to predict. While most non-bank landers lack the scale needed to take over the trade finance space, the cheap and fast liquidity they provide will set a new standard in the market that corporates will come to expect from all lenders.

This may put pressure on banks to follow suit, sacrificing compliance and rigour for speed and creating bad practices. Little-regulated non-bank lenders collapsing or losing interest in trade finance as an asset class could contribute to even more instability in the market, further widening the trade finance gap.

The standards paradox

Regulators are applying different standards to banks compared to non-bank lenders; while well-intentioned in terms of widening access, this creates challenges for banks in the provision of financing. Restrictive and costly regulation is making it harder and harder for banks to expand access to financing, and SME loans are often the first to suffer.

In the payments sphere, too, regulators push for cheaper cross-border payments while at the same time imposing a growing number of anti-money laundering (AML) and KYC requirements on international transactions. This raises cost and processing times for banks, making it even harder for them to adhere to the growing body of regulations around instant payments, such as the EU’s Verification of Payee and Instant Payments Regulations, which came into effect in the last couple of years.

If banks are forced to carry an excessive burden, especially in terms of KYC requirements to fight financial crime in certain areas or activities, they might decide to forego those activities entirely.

This pushes banks away from the markets that need them most, as they may come to deem those markets too dangerous or complicated to apply the regulation to. In the long term, excessive regulation and a fragmentation of global standards could cause some banks to abandon supply chain finance entirely, again depressing access to trade financing.

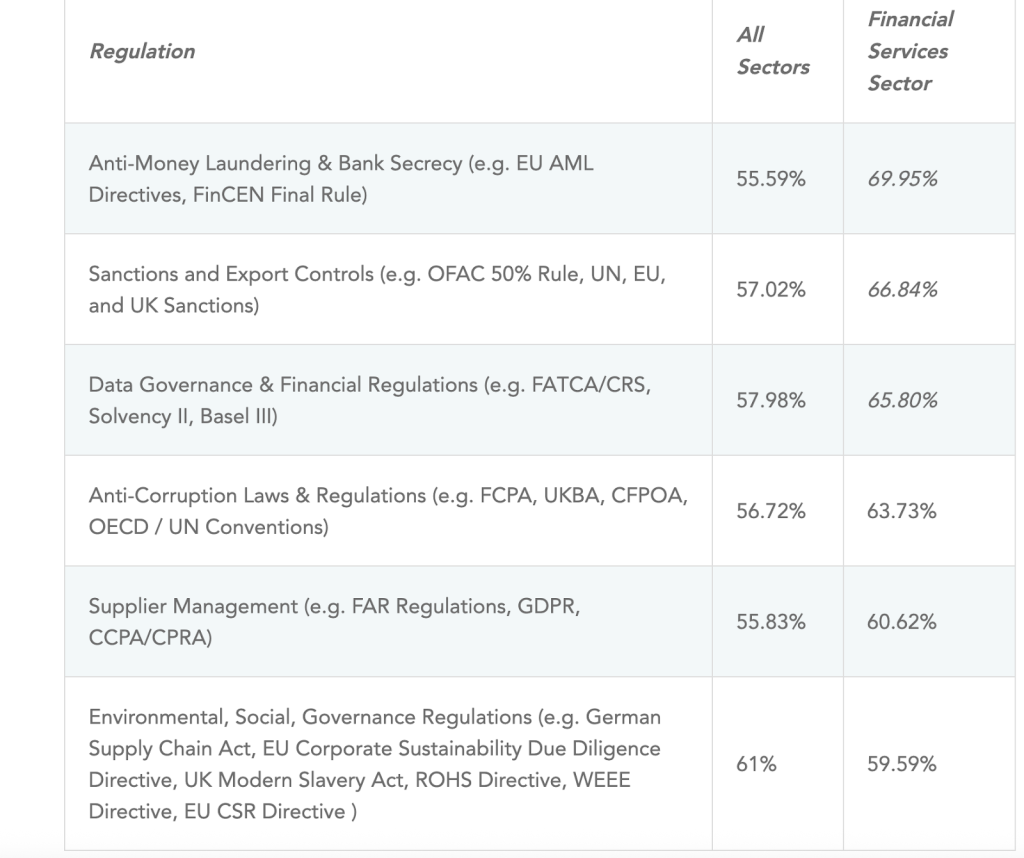

Source: Dun & Broadstreet, 2024. The top regulations taking up increasing amounts of time for firms – the financial sector is the most affected in nearly every instance.

Overall, as Dr Ian Malcolm (Jeff Goldblum) lamented in the 1993 ‘Jurassic Park’, “Your scientists were so preoccupied with whether they could, they didn’t stop to think if they should.” There is little in the human psyche to curtail the desire to innovate. It takes someone whose head isn’t in the thrill of the discovery, whether that’s cloning extinct dinosaurs from DNA traces or mitigating credit risk, to apply the brakes before the damage is done.