Estimated reading time: 7 minutes

The payments ecosystem continues to rapidly change and evolve. This is being driven by increasing pressure from regulators, intense competition from new entrants and customers who now expect payments to be instant, frictionless and account-to-account. To address these challenges and meet the needs of our clients, a modern, structured, open and pervasive payments language is now required.

What Is ISO 20022?

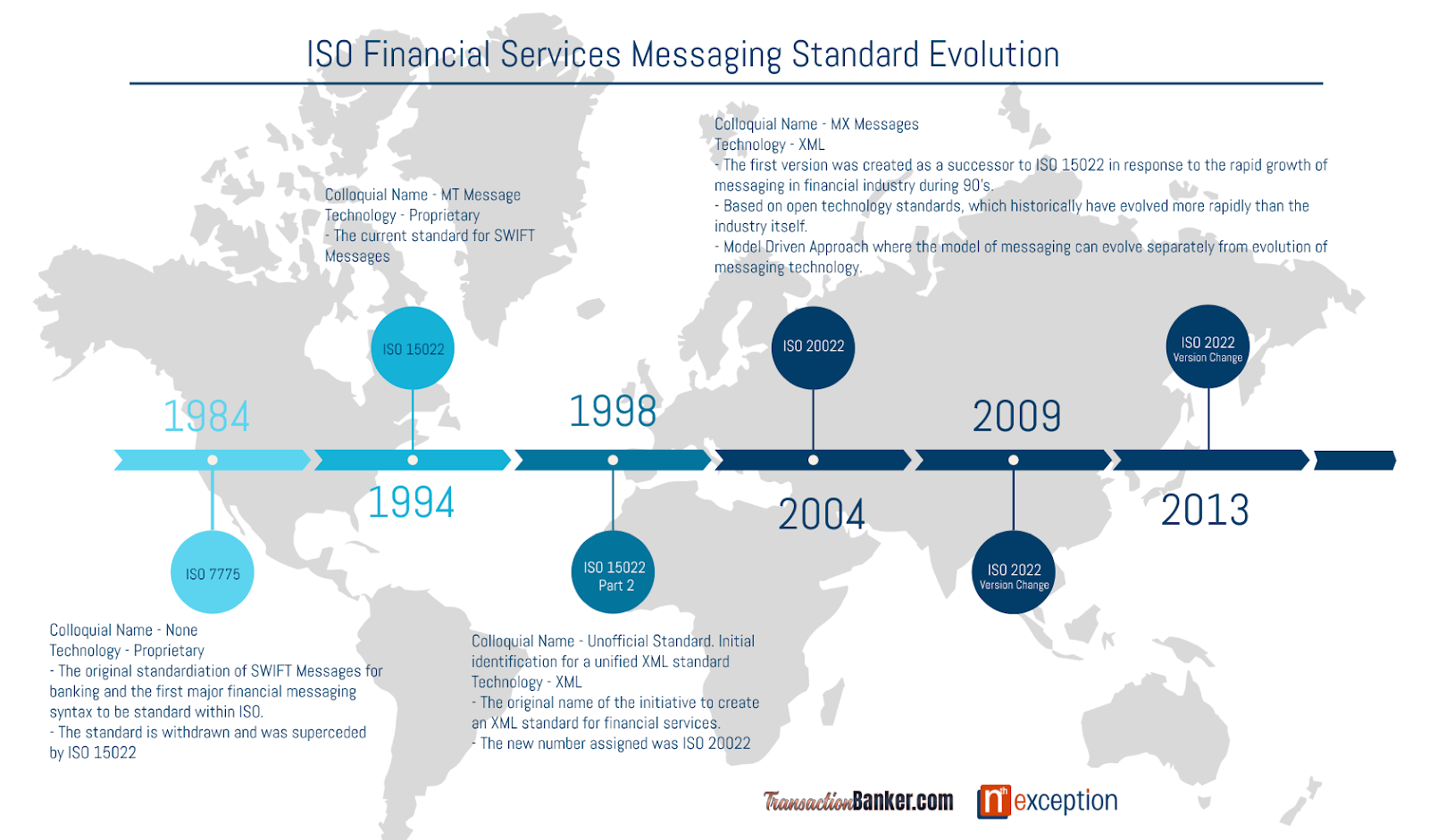

For over 40 years the MT standard has enabled industry automation, reducing the cost and risk of cross-border business, and enabling the development of the correspondent banking system on which world trade depends.

Today, around 28 million MT messages are exchanged on the Swift network every day. But after 40 years, MT is beginning to show its age. MT was designed at a time when storage and bandwidth cost more than they do today, emphasising brevity over the completeness or readability of data.

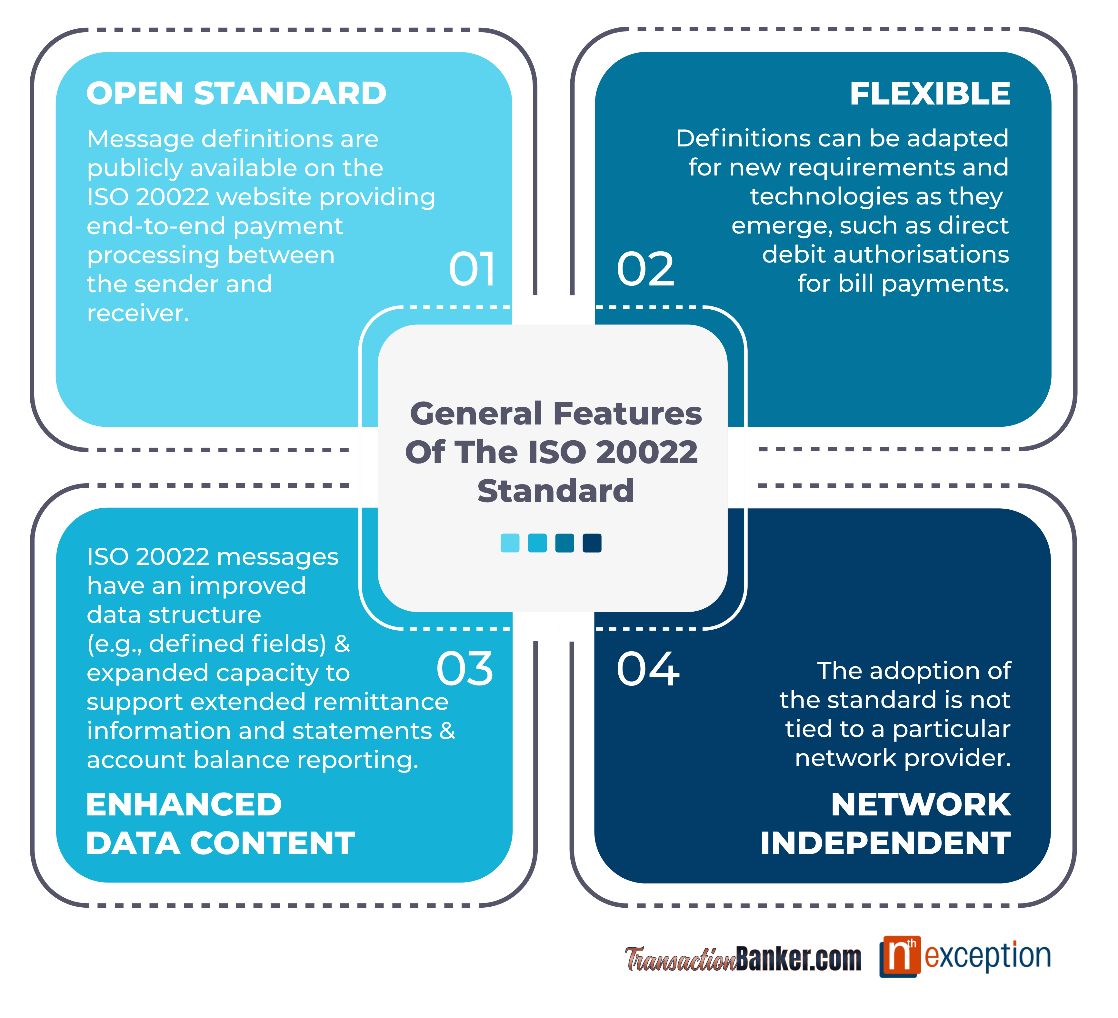

ISO 20022 was introduced by the International Organization for Standardization in 2004. It is an open and general-purpose global financial electronic communications standard. The ISO 20022 message standard is a data library of business components from which messages can be defined.

The ISO 20022 message standard provides flexibility as payment messages can be adapted over time to evolving requirements. It supports structured, well-defined and data-rich payment messaging. This improves the quality of payment information contained in the message.

Adoption factors

The success of ISO 20022 amongst market infrastructures has led to increasing community demand for ISO 20022 for cross-border business. There are several reasons for this, particularly for international payments:

Key Benefits of ISO 20022

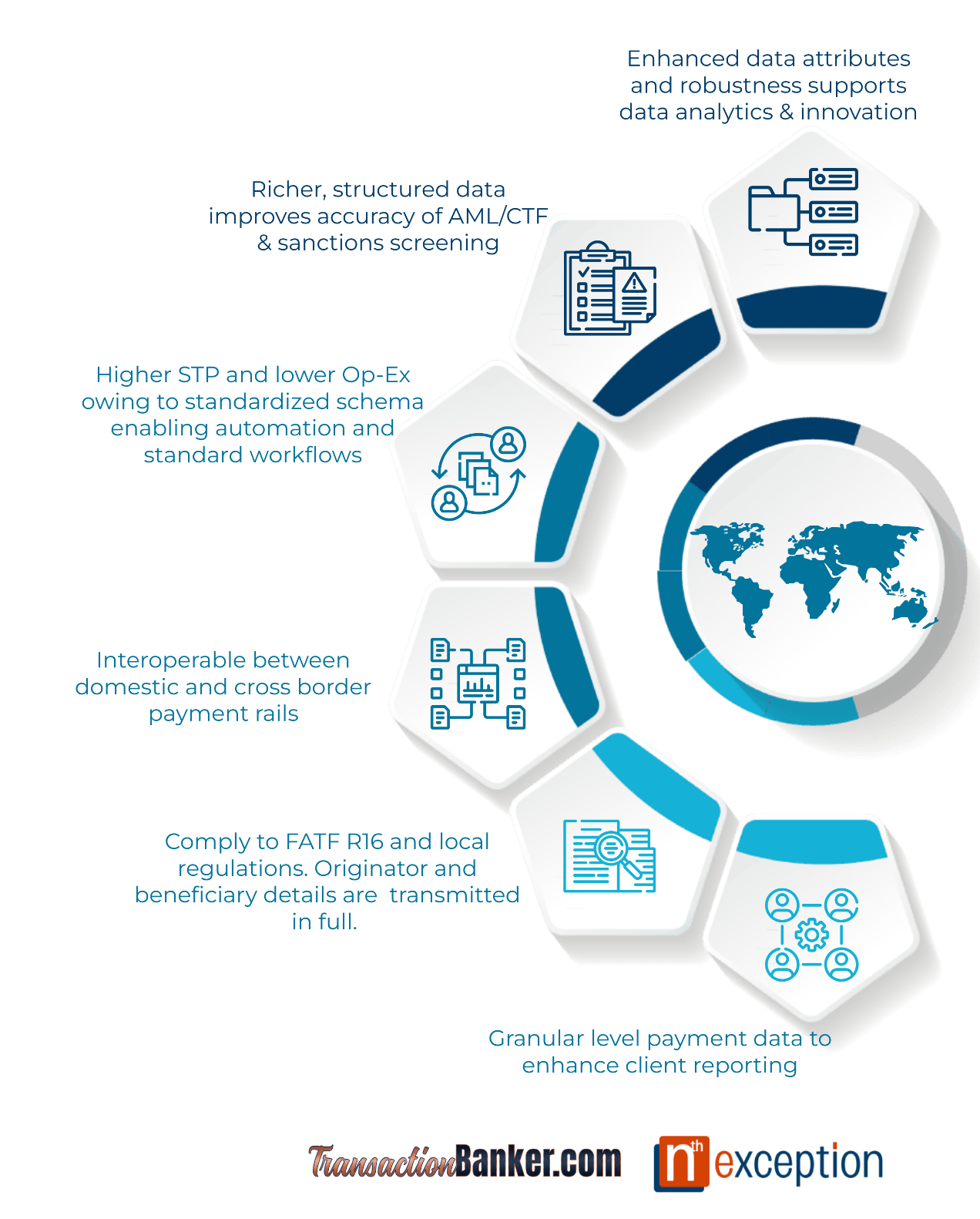

The ISO 20022 message standard delivers benefits to all users throughout the payments chain. In the HVPS, the benefits are realised by the financial institutions and their corporate clients who send and receive these messages.

Over time, customers are expected to benefit from data-rich payments, more efficient and lower-cost payment processing, and enhanced customer services such as improved remittance services. Among the benefits financial institutions may gain from the migration to the ISO 20022 message standard are shown below.

Key Considerations

ISO 20022 is more than a technology investment. It provides more remittance information to improve reconciliation for clients; makes payment processing faster with consistent and structured data across the end-to-end payment chain; and improves the efficacy of compliance controls with all payment actors identified with granular details.

Data truncation during coexistence of old and new message standards

During the coexistence period, financial institutions will translate payment messages between Swift MT and ISO 20022 standards. Truncation may occur when translating to MT, potentially affecting compliance screening.

Institutions must ensure full message data is used for monitoring and screening. From March 2023, HVPS intermediaries receiving ISO 20022 messages for cross-border payments must pass on the complete ISO 20022 message for processing. Translation to MT for HVPS processing risks data truncation due to ISO 20022’s richer content. These messages were to be translated into an MT message for processing through HVPS.

Scale, timing and competing priorities

The migration involves significant work for financial institutions and potentially their corporate customers over an extended period. The new data structure and rich payment information impact a range of processes, including monitoring, screening and analysis of payments, with flow-on effects for a range of supporting systems.

These systems may need to be modified to process ISO 20022 transactions, and enhanced to be able to fully reap the benefits offered by the new message standard.

With a range of other industry projects and international initiatives currently underway it is important that domestic migration is appropriately managed to ensure that it does not place undue pressure on participants, which could give rise to additional risks.

Alignment and Harmonisation

The straight-through processing of SWIFT cross-border payments relies on the alignment of HVPS messages with those that will be used for SWIFT cross-border payments. Domestic alignment between the payment systems should be considered, particularly with the longer-term objective of creating resilience between the systems.

Adopting international standards for public infrastructure

Central banks are adopting ISO 20022 as the messaging standard for new systems, an internationally accepted standard that enables participants in the payments ecosystem to send richer information on transactions than in the past.

Further, central banks should collaborate closely with industry groups already working on international standards harmonisation, such as the Payments Market Practice Group, which is leading efforts to define usage guidelines for consistent use of ISO 20022 in cross-border payments.

The adoption of ISO 20022 could reduce cross-border payment friction in two important ways.

- Central banks sharing a common messaging standard will be able to make more transactions and pass along richer information important for clearing transactions (e.g. KYC information, AML/CFT reporting, etc.).

- By adopting an international standard for important financial infrastructure, payment providers wishing to connect with this infrastructure have an economic incentive to modernise their messaging systems and adopt new standards.

- This in turn could have multiplier effects throughout the broader ecosystem, in which players use common standards to send messages to each other and within their own payment networks, either through a real-time payment system or through other open, interoperable networks. Finally, adopting the same standard as other payment systems reduces the costs associated with integrating with the other systems.

Modernisation will be costly for Central Bank participants, especially for larger financial institutions, so central banks should expect multiple international standards to run in parallel in the near term. Costs may be a significant impediment so new financial infrastructure and broader modernisation projects should be evaluated in parallel with other priorities given initial implementation costs.

International Developments

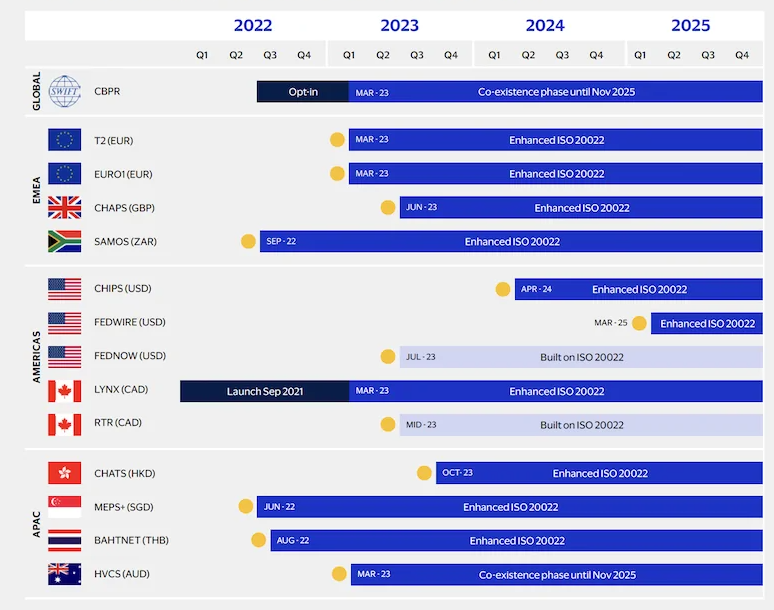

Over the past decade, there has been an international push to migrate to ISO 20022 messaging from a number of key FMIs. Swift estimates that by 2025, 87% of the value and 79% of the volume of high-value domestic payments messaging worldwide will use ISO 20022. A number of the migration projects are being completed as part of a larger infrastructure refresh.

Source: CBPN (https://cbpn.currencyresearch.com/blog/2023/11/22/decoding-iso-20022-lessons-for-cross-border-payments)

SWIFT ISO 20022 migration for cross-border payments

Swift and Swift CBPR+ listed vendors facilitate the coexistence of ISO 20022 and MT message standards until 2025. Post-transition, only ISO 20022 will be supported, with internal translations continuing during system upgrades.

Swift will cease support for MT Categories 1, 2, and 9. ISO 20022’s adoption has enhanced payment systems like FedNow, TCH RTP, NPP, FAST, and Swish, enabling efficient, data-rich processing. Notably, it allows for up to 240 characters of remittance information, a significant improvement from previous limits, enhancing payment flexibility and efficiency.

ISO 20022 has transformative impacts on transaction banking, driving standardisation, automation, interoperability, innovation, and efficiency across payment and trade processes, cash management activities, and client services.

Transaction banks need to embrace ISO 20022 structured data to capitalise on the benefits and opportunities it offers for enhancing their operations, services, and competitiveness in the transaction banking landscape.