-

US President Donald Trump has threatened 10% tariffs on several European allies as part of a push to take over Greenland.

-

The European Union has proposed a retaliatory €93 billion tariff on American imports in response to these threats.

-

The escalating trade tensions and US interest in the region are partly driven by the development of the North Sea Route by Russia and China.

During his speech at the World Economic Forum (WEF) in Davos today, US President Donald Trump argued for the “ownership to defend” Greenland. A rambling keynote speech leaves a lot of statistics to be verified, and a lot of Europeans in confusion, not least for his constant mistaking of Greenland for Iceland (“big pieces of ice”).

Coupled with his threat to apply tariffs to his closest allies as he pushes to take over Greenland, the North Atlantic Treaty Organization (Nato) looks like it is becoming more and more fraught.

Much of the speech focused on the US relationship with Nato, which Trump has long argued is one-sided; Trump said the US had been providing “100% or close to 100%” of funding, but he was not sure the alliance would come to the US’s aid were the US to need it.

Quieting the fears of many in the room, the US president said he “probably won’t get anything unless I decide to use excessive strength and force, where we would be, frankly, unstoppable. But I won’t do that.” However, a pointed story about using tariff threats on European wine exports to bend the wills of European leaders – many of whom were present in the room – left no doubt about the tools he will use instead.

To be clear, these are threats, not a plan. Perhaps this article is worth revisiting on the proposed 1 February implementation date, after what will continue to be a tumultuous week in Davos.

In the words of UK Prime Minister Keir Starmer, for Trump’s 10% tariffs on the UK, France, Denmark, Norway, Sweden, the Netherlands, and Finland – as he has threatened to do in a post on Truth Social – is “completely wrong”. The tariffs would amount to roughly $36.5 billion, based on a 10% tariff applied to 2024 levels of exports to the US; the European Union (EU) has proposed a €93 billion tariff on US imports in retaliation.

Whether this is another instance of TACO – Trump Always Chickens Out – or whether we will see some real and serious costs to European suppliers from some significant tariffs, the symbolism of Nato dissolving under the pressure of a trade war will hold significant implications in trade finance.

What do growth-promoting hormones in beef and luxury champagne have in common?

There is a distinct pattern in the history of US tariffs on Nato members, of perceived discrimination resulting in retaliatory tariffs. Never has anything come close to the situation at present, where tariffs are being used as an intimidation tool against the countries that have deployed troops to Greenland in response to US posturing.

Many twentieth-century disputes between the US and European Union (EU) and Nato counterparts are a consequence of the vastly different cultures on agriculture and meat. The 1961-1964 ‘Chicken War’ between American poultry producers and the European Economic Community (EEC) began with an EEC-imposed tariff on American chicken imports, ostensibly because US chicken was “diseased” – but largely understood to be a protectionist measure. In response, President Lyndon B Johnson imposed retaliatory tariffs amounting to $26 million, to offset the calculated loss to the US.

The beef hormone dispute of 1998, which centred around an EU ban on the import of US beef raised using growth-promoting hormones, followed a similar story. The General Agreement on Tariffs and Trade (GATT) and the World Trade Organization (WTO) ended up ruling against this ban, arguing that the health and safety concerns touted by the EU were not backed by enough valid scientific evidence. However, the EU claimed it could not comply with this ban, and sought stronger legal recognition of the “precautionary principle” in consumer safety matters.

The EU ban on growth-promoting hormones in beef resulted in the US levying ad valorem – customs calculated as a percentage of the value of a product – tariffs of 100% on certain EU products. These concessions were valued at $116.8 million, set to reflect the damage of the hormone ban.

The beef hormone dispute was resolved with a memorandum of understanding (MoU) establishing a duty-free import quota for grain-fed, high-quality beef (HQB) for the EU in 2009. Nonetheless, the US Trade Representative (USTR) wrote in 2017 that the US will continue to engage the EU regarding the “unscientific ban on meat and animal products produced using […] growth promotants”, which will be an interesting trajectory to monitor with Robert Kennedy Jr at the helm as health secretary.

During his first administration, in December 2019, Trump threatened tariffs on French goods up to 100% in response to the French Digital Services Tax (DST). The DST was intended to limit how much American tech giants, including Google, Amazon, and Facebook, could avoid tariffs; a study from the USTR found the DST to “amount to de facto discrimination”, prompting an American response.

Trade wars between the US and Nato members have until now centred around consumer safety and domestic protectionism. The tariffs threatened as part of the Greenland dispute encompass billions rather than millions, and threaten to escalate into a dangerous military situation set to rattle through political risk markets.

Rebecca Harding, CEO of the Centre for Economic Security, told Trade Finance Global (TFG), “Recent US tariff threats linked to Greenland are not about trade policy in the conventional sense, but about using trade instruments as tools of economic warfare.

“While tariffs are typically designed to protect domestic industries or rebalance trade flows, these threats are aimed at advancing US national security and foreign policy objectives, even against allies. Their economic impact – rates, coverage, or implementation – is largely irrelevant; the damage lies in the uncertainty they create for businesses and the signal they send: that trade with the US is becoming more costly, complex, and politically contingent.

“The mere threat of tariffs undermines trust in the post-war liberal trading order and weakens institutions built on shared rules and values.”

Why Greenland and the Arctic antics?

There are plenty of reasons to speculate why the US has chosen now to escalate tensions in Greenland. That the US have been doing the heavy lifting in terms of investment in Nato for most of its existence, and that the Organization is realigning as a whole; that the US has security interests in Greenland, which was the basis for the 1951 Defence of Greenland Agreement. These are the ones put forward by Trump in his speech today.

Perhaps even that Trump is seeking a nineteenth-century-esque planting-the-Star-Spangled-Banner takeover. “Some [European countries] had great, vast lands all over the world, they went and reversed it. But some grow,” he told the Davos audience.

But of more relevance to trade finance and supply chain finance practitioners is the Russian and Chinese plan to develop a North Sea Route (NSR) through the Russian Arctic, as agreed in autumn 2025. The first shipment using the NSR – from Ningbo, China, to Felixstowe, UK – took 20 days, a week less than the southern route.

Transit figures between 2024 and 2025 through the NSR reveal 103 transit voyages from China to Russia and the UK, a 6.2% increase compared with last year’s figure. Figures also show unclear destinations in crude oil shipments from Murmansk, Russia, through the NSR over the last year, suggesting possible transhipment for exports.

All of these trends have contributed to US fears of sanctions bypassing and security threats, and have been put forward as justification for their Greenland ambitions. But given that over the past decade, Asia has overtaken North America as the largest market for European exports, the US has clear domestic trade interest in accessing the NSR.

Additionally, the disruption compounds the fact that “Western operators are already shying away from testing or using the Arctic shortcut, partly for environmental reasons,” as Malte Humpert, founder and senior fellow at The Arctic Institute, observed (coupled with environmental reasons and political reasons following Russia’s invasion of Ukraine).

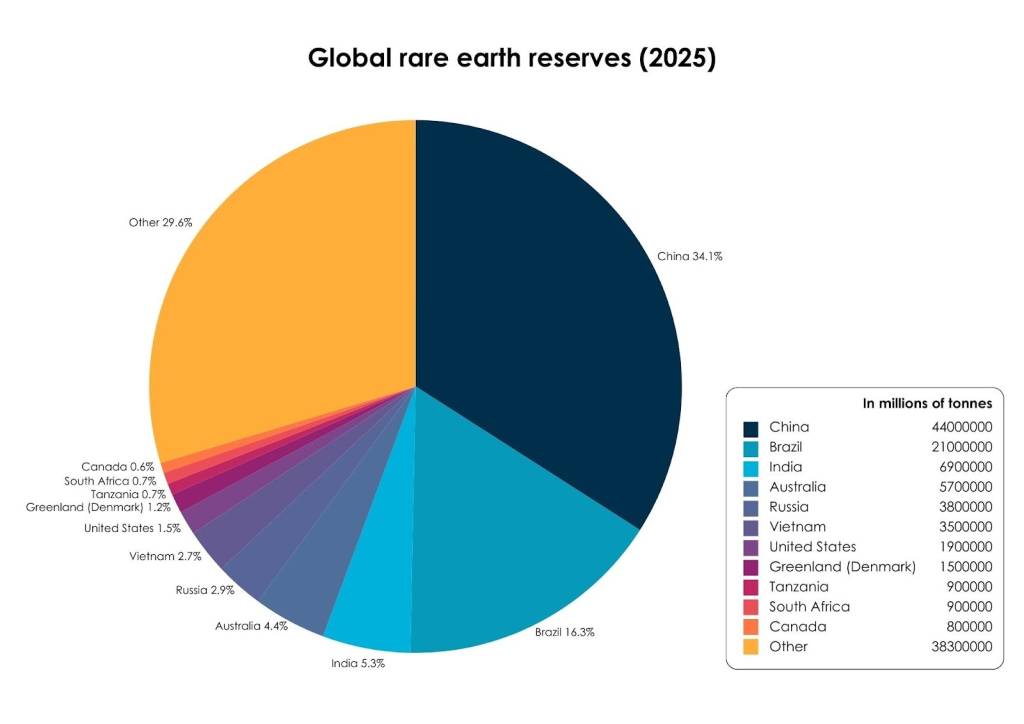

Rare earth materials could pose another area of interest for the US. Greenland ranks eighth in terms of global rare earth reserves, with 1.5 million tonnes; additionally, 24 of the 34 critical raw materials on the list of critical raw materials for the EU can be found in Greenland. However, Greenland only has two active mines – one gold mine and one anorthosite (feldspar) mine.

In his speech, Trump said his interest in Greenland was “not about minerals,” despite claims to the contrary, and that in fact “there is no such thing as rare minerals.”

Source: Trade Finance Global (TFG), with data from the US Geological Survey

Trump’s Venezuelan ambitions portend a similar trajectory, though his mining ambitions have been dismissed as “completely bonkers” by Humpert. “You might as well mine on the moon. In some respects, it’s worse than the moon.”

What should trade finance businesses do?

His approach to tariffs on Switzerland appeared to have been strongly based on being “rubbed the wrong way”, and brought down when appeased. Many places, Trump argues, are making a fortune because of the US, that the US are keeping the whole world afloat and being “taken advantage of.”

The fervour Trump is whipping up is likely to disincentivise businesses from investing in the Arctic region, as Humpert told TFG. “Businesses like predictability and certainty, something that’s already in short supply in the rapidly changing Arctic region. Trump’s ongoing Arctic antics are not conducive to attracting investments in the region.”

The situation is vastly different from instances where tariffs were deployed to protect domestic industries, as Matthew Fox, Tax Partner at Spencer West LLP, reiterated. “Tariffs are increasingly deployed as a bargaining chip. They are announced, threatened, paused, or targeted not because they improve economic outcomes, but because they create pressure.”

As such, business resilience and insurance from volatility grow more crucial. “For internationally exposed UK businesses, my consistent response has been preparation through a disciplined tax operating model that integrates tax, trade, and supply-chain strategy,” said Fox.

PANGEA-RISK’s Insight 2026 report highlights how alliance disunity can be a source of geopolitical risk for its potential to instigate adversary behaviour.

“Understanding where real trade exposure sits, separating tax risk from customs risk, and stress-testing operating structures against trade friction are no longer optional, but core elements of international structuring and decision-making,” said Fox.

From a foreign exchange (FX) perspective, “Without the constant drumbeat of commentary from the US administration about a variety of geopolitical and trade topics, the US dollar would be a lot stronger,” Neil Parker, Chief Economist at Moneycorp, told TFG. “The risks from additional US tariffs lie not in weaker global economic growth, but in higher US prices and lower US earnings.

“For the US dollar, the ever-changing global trade environment will continue to exert short-term pressures, but medium to longer term, the US economy continues to possess the upper hand, in my view.”

—

Trump’s plans for Greenland have dominated the Davos discussions, edging global markets lower and conflating trade sovereignty with security and ideology.

“Without us, it’s not any of the countries that are represented here. And we’re not looking to destroy them,” he said at the WEF. A bellicose leader steering a dominant global economy cements an uncertain few months ahead for trade, commodities, and FX practitioners alike.