Recent trade developments with the US and China had accelerated a trend of companies in the South-East Asian region taking the seat a global, cost-efficient, manufacturing hub from China, who is slowly moving towards more sophisticated production lines.

Recent trade developments with the US and China had accelerated a trend of companies in the South-East Asian region taking the seat a global, cost-efficient, manufacturing hub from China, who is slowly moving towards more sophisticated production lines.

However, what we find is a previously importer-focused economy engaging in more and more international trading, with a majorly underserved trade finance market. Prospective traders within the South-East Asia region, particularly SMEs, find themselves held back by critical financing barriers due to a system not optimized for the ever globalizing world.

The Trade Gap

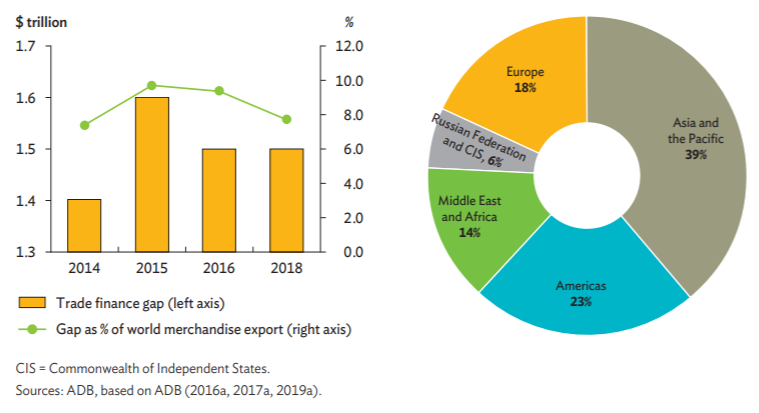

The gap between unmet demand and inaccessible supply of trade finance in the South-East Asia region has been estimated to be the largest (39%) and most persistent, when compared to global performances.

A 2019 trade facilitation report from the Asian Development Bank (ADB) and United Nations Economic and Social Commission for Asia and the Pacific (ESCAP) measured the region’s finance gap through quantitative analysis of trade finance proposal rejection rates, indicating an unmet demand gap measuring up to $1.6 trillion USD (£1.24 trillion GBP).

Global Trade Finance Gap 2014-2018, Measured by Rejection Frequency & Region | SOURCE : Asian Development Bank (ADB), 2019

The report found that approximately 50% of international trade finance applications are initiated from the Asia and Pacific region, 40% of global rejections originate from the region.

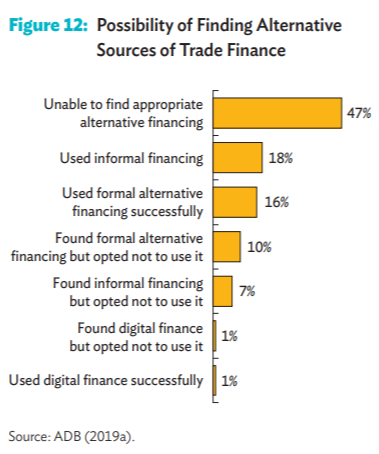

SMEs in particular are facing the effect of inaccessible trade finance – their higher transaction, information, and risk costs for banks contribute heavily to SMEs’ particularly high trade finance rejection rate. The lack of appropriate trade financing for the SME market in South-East Asia blocks inclusivity of a very significant portion of the region’s revenue generation.

Probability of Finding Alternate Sources of Trade Finance for SMEs in the South-East Asia Region | SOURCE : Asian Development Bank (ADB), 2019

Survey data from ADB’s 2019 report estimated that around half of firms with rejected trade finance proposals were unable to find appropriate alternative financing, and found that access to finance is significant to SME growth and international participation.

Adapting For the Future

Although the large number of trade finance proposals coming from the South-East Asia indicates the region’s populated participation in the international value chain, the disproportionate high number of rejections implies the need for more inclusive trade.

One of the most significant contributing factors to the trade imbalance is process inefficiency–especially as the region is still developing, local banking institutions, more often than not, still rely on paper-based procedures. The very sluggish process often creates a chain effect that increases the occurrence of financial fraud. Other barrier concerns include banks’ complicated procedures, high bank commissions, the region’s tariff-related uncertainties.

Regulatory requirements (i.e. AML/KYC compliance) form the most significant concerns trade finance candidates face, according to a 2019 survey by ADB; SMEs bear a disproportionate burden from bank regulation. Due to a lack of a case-by-case consideration basis for regulation, the already high costs of compliance procedures is exaggerated for SMEs because of their much lower assets and collateral, and higher risk consideration. Banks tend to avoid risk altogether in such scenarios, creating the large rejection rate of trade finance proposals we see in South-East Asia.

Technology Leads the Way

With recent, visible growth of Foreign Direct Investment in South-East Asia, the move towards digitalising trade finance access observes its demand more than ever.

“There is an enormous untapped potential in the rapidly evolving digital technologies. Emerging new technologies can help address long-standing issues of high transaction and processing costs, while mitigating the huge trade finance gap,”

— Bambang Susantono; ADB Vice-President for Knowledge Management and Sustainable Development

Data pulled from Singapore’s Department of Statistics in October last year showed that their national trade volume was valued at more than S$89 billion (£49.67 billion GBP), of which up to 40% was facilitated by trade finance banks. What Singapore had done to refine their trade finance market was to adopt extensive digitalisation of their processes, notably through the use of blockchain in Singapore’s Networked Trade Platform (NTP). Singapore’s trade finance environment enables the application of finance proposals through standardized and secured forms, as well as the receival of real-time status updates on their proposals, all pushing towards facilitating a seamless, international value chain.

Digitalisation for the rest of the South-East Asia region would mean more readily available, traceable, and transmittable information, creating a more accessible and optimized trade ecosystem and putting countries on the same path as Singapore.

Digitalisation has also introduced efficiency the supply chain financing time cycle around the world, showing reductions such as from 90 days to 24 hours.

From a report by ADB and ESCAP, technological trade finance access does not only mean blockchain, but also the application of Artificial Intelligence and optical character recognition (OCR) solutions to streamline documentation verification processes

Getting Onboard

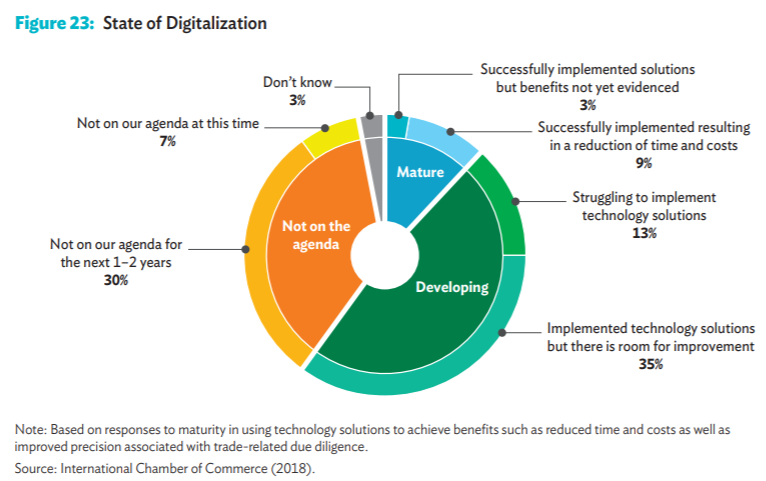

While digitalisation of the region’s banking processes seems to be the right way forward, one of the major factors to the persistent nature of South-East Asia’s trade imbalance is the burden of widespread onboarding.

State of Digitalisation in the South-East Asia Region as of 2018 | SOURCE: International Chamber of Commerce 2018

According to the ADB, the chance of new technologies being successfully implemented becomes higher as more parties get involved in the process, and an emphasis on platform interoperability and widespread participation is required to realize the benefits of digitalisation.

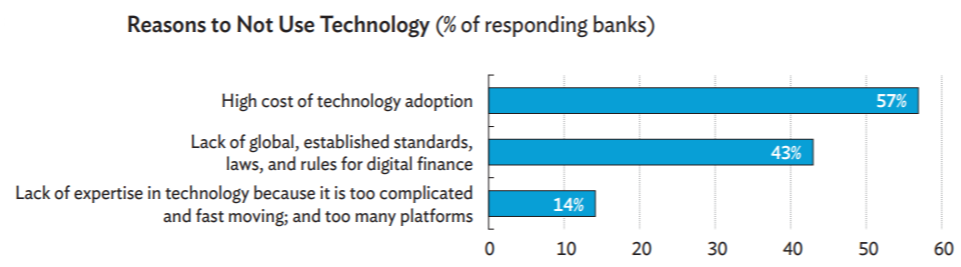

To facilitate holistic digitalisation in the industry, being backed by established global standards and laws such as current initiatives by the World Trade Organization’s Trade Facilitation Agreement and ESCAP’s treaty on enabling digital trade in Asia and the Pacific can also help push banking institutions into adopting new technological processes.

Survey Data of Trade-Finance Banks; Reasons to Not Use Technology | SOURCE: Asian Development Bank (ADB), 2019

Road Towards Seamless Trade Finance

It is clear to see that the path to growth and accessibility in Trade Finance within the South-East Asia region, is the turn to digitalisation.

In order to create a more inclusive and productive trade environment for the region, digitalisation of certain trade processes will create connectivity that provides SMEs increased participation in global value chains.

Progress has already been taking off in the region: the Malaysian multi-bank supply chain finance platform, CapitalBay, has recently received approval from regulatory bodies to operate peer-to-peer (P2P) financing processes; Deutsche Bank recently begun more intensive participation in driving transaction banking in Southeast Asia.

Digitalising processes is key for Southeast Asia to close the trade finance facilitation gap, and reach its true economic powerhouse potential on the global stage.

Now launched! Spring Edition 2020

Trade Finance Global’s latest edition of Trade Finance Talks is now out, taking a deep dive into trade finance in emerging and developing markets.