- This article forms the second chapter of the whitepaper from Trade Finance Global (TFG) and the Bankers Association for Finance and Trade (BAFT): “From lenders to leaders: Banks in flux”.

- Banks have always had a leading role in encouraging ESG adoption.

- However, as governments and corporates rethink which investments are valuable and which to discard, banks are internally recalibrating their priorities too.

Sustainable supply chains have pervaded the conversation around environmental, social, and governance (ESG) for years. Statistics around the polluting impact of container shipping or child labour scandals in the clothing industry act as phantoms in any discussion on the ESG impact of international trade.

With ESG regulation that ebbs and flows and consumer sentiment that is often hard to decipher, corporates are having to chart their own path towards ESG adoption. It is often up to banks, however, to drive the way forward for the trade industry, incentivising sustainable development while still prioritising growth.

The spectre of green-hushing

After the past five years, when it seemed like ESG was all anyone could talk about, corporates are seeing a slowdown and even a decrease in sustainability commitments. This is driven on the one hand by a political backlash in some regions, such as the US, and on the other by increasingly stringent laws on greenwashing (such as Bill C-49 in Canada and the EU taxonomy in Europe) that punish non-factual commitments to environmental goals.

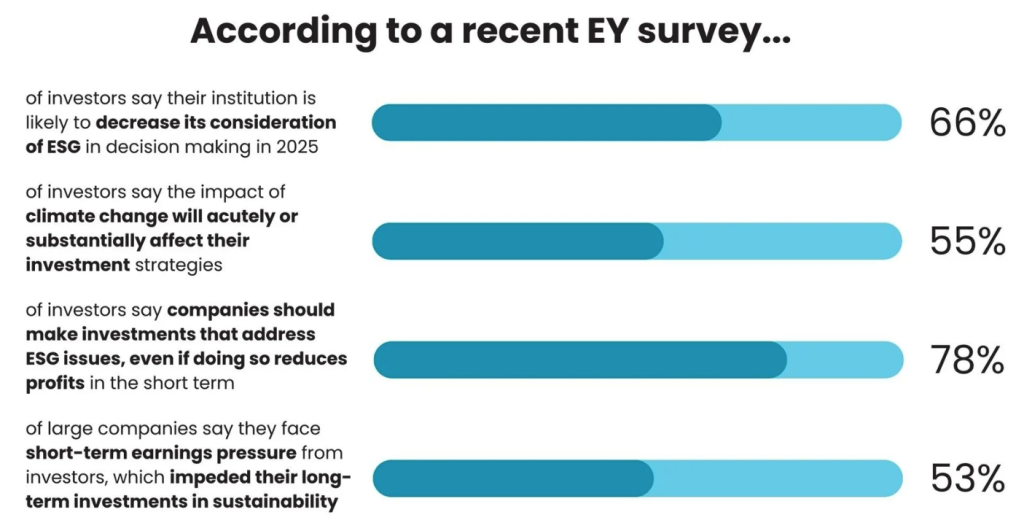

Source: EY Global Investors Survey 2024

Instead of regulation dictating how banks and corporates can describe their ESG initiatives, the key to sustainability across the economy is financial support. Companies looking to transform their production to become environmentally friendly may find it to be prohibitively expensive, especially with the tight timelines set by many jurisdictions, such as the EU. “It’s not just a matter of having a sustainable supply chain, but also having one that you can pay for,” said one participant.

However, not transforming production and procurement processes can also be financially unwise, especially as carbon credit schemes and border adjustment mechanisms gradually come into force. Therefore, corporates must find ways to keep up with the green transition that are not just environmentally but financially sustainable.

ESG: An incentives game

“If you’re a corporate, setting aside the ethical imperative, why are you going to structure things in an ESG way?” you may ask. Corporates are notably not as affected by ethical imperatives as Kant would like them to be. They are pushed towards ESG by three main sources of pressure:

- Government or regulators, either in terms of restrictions or fines, or on the other hand, by incentivising good performance;

- Investors, especially activist investors or green funds with specific environmental targets;

- Customers and consumers.

In consumer and retail supply chains, especially the retail clothing sector, customers are one of the most important sources of pressure. Even in regions where it seems like the push for sustainability is waning, this is only visible in terms of regulation, as consequential as that may be: consumers and investors have not changed their priorities. This also means that in many regions unaffected by a regulation rollback, nothing has changed at all, and talk of “green hushing” is mostly spillover from the US.

While banks have an enormous potential to drive the green transition and incentivise ESG commitments, they don’t necessarily have a mandate to do so. “At the end of the day, banks provide financing solutions. You can use a financing structure to incentivise any behaviour. It’s for the corporate to tell us what they need to incentivise in order for them to succeed, then we structure accordingly,” said one participant.

Banks often have their own standards around sustainability-linked and green investments – if nothing else, to protect themselves against the reputational damage caused by accusations of greenwashing. Within those guidelines, though, banks mostly follow their corporate clients’ priorities in terms of sustainability tracking and goals.

Banks, then, are those most affected by changing and loosening environmental regulations, which removes their financial incentive to invest in sustainable projects. In the absence of regulatory incentives, banks may struggle to justify financing an ESG-linked firm rather than a comparable, potentially more profitable, emissions-intensive project – which is why internal guidelines are so critical.

Sustainability is a many-splendored thing

James Cameron’s ‘Avatar’ (2009) paints a world where the extraction of one rare resource – unobtanium – destroys an entire ecosystem, chronicling the push and pull between progress and preservation. Is there a way to satisfy both? In the rush to fuel growth, what are we willing to trade away?

Even when talking about straightforwardly sustainable investments, there is a world of difference between “pure play” sustainable investments and ESG-structured or linked investments.

The renewable energy sector, one of the most sustainable industries there is, is booming – but it doesn’t need incentivised loans to do so. Especially in Asia, where governments and companies have been investing in green energy for decades, the sector is expanding at breakneck rates, powered by an AI revolution that guzzles record amounts of energy and a global economy that will need more than the world’s dwindling supply of fossil fuels to keep growing.

Even petrochemical companies are investing heavily in green energy, vertically replicating their existing company structure through sustainable energy. This is not because of a regulatory push or promised incentives, or even to appease clients and investors, but to respond to the continuously growing global demand for energy. Pure play sustainable investments like renewables, then, are the most organic sort of sustainability there is, and will prosper no matter the regulatory or corporate incentive structures.

Non-pure play sustainable investments, on the other hand, have much less of an incentive to maintain rigorous sustainability standards or even link themselves to ESG goals. Corporate interest rates in most of the world are so low nowadays that any incentive banks give for sustainable investments will likely not be enough to convince corporates to transform their supply chains to be more sustainable. This means corporates willing to submit themselves to the rigorous measurements and KPIs required by a sustainable-linked investment are few and far between, and there is little, if anything, banks can do about it.

The one exception to this is investments to increase resilience to climate-related risks, such as extreme weather events or water shortages. While not ESG in the traditional sense, infrastructure investments to adapt to the climate crisis will make the global economy more resilient in the long term, and often include measures that are beneficial to the environment today, such as those that lower energy or water consumption.

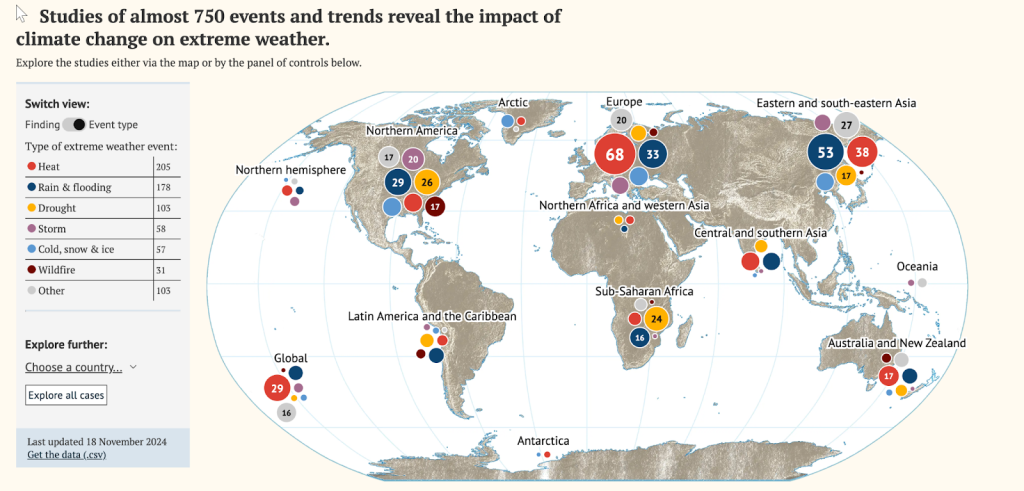

Source:

Rigour beyond regulation

That many regulators have stepped back from stringent taxonomies and standards may, in fact, breathe new life into sustainable investment, especially in emerging economies. There, large banks have been committing to ESG goals for years – especially those around the much-neglected S and G, such as inclusive financing, loans for small and medium-sized enterprises (SMEs), and support for women and youth-led businesses.

When regulators imposed strict standards and taxonomies, they risked cutting out not just small businesses, but also local and regional banks that often lack the resources to measure every standard required by regulation. In this way, a smaller institution that has been complying with ESG goals for years saw itself blocked from reporting its social impact by a regulation that holds it to an impossible standard.

Now that regulators have stepped back somewhat, small and large banks alike are continuing their sustainable investments – in many emerging economies, increasingly pushed by a need for them, especially in terms of resource optimisation. The ESG revolution is then balanced and motivated from the ground up, and thus truly, economically as well as environmentally, sustainable.