Supply Chain Finance (SCF) is defined as the use of financing and risk mitigation techniques to optimise the management of the working capital invested in supply chain processes. It is typically applied to open account trade and is one of the fastest growing trade products. However, financial institutions often don’t use similar terminology or accounting techniques.

Supply Chain Finance trends in 2019

Some of the most interesting recent developments in the SCF sector are data-driven credit decisions and the advanced deployment of blockchain. The technologically saturated market resulted in the movement of SCF programmes down to the SMEs, creating new opportunities for growth. However, the challenges for financial institutions stay fundamentally the same. Meaning as more suppliers want to sell directly to SMEs; the KYC, AML and underwriting trade credit practices are not less strict (assuming customer risk is the same but there are many more customers with smaller balances).

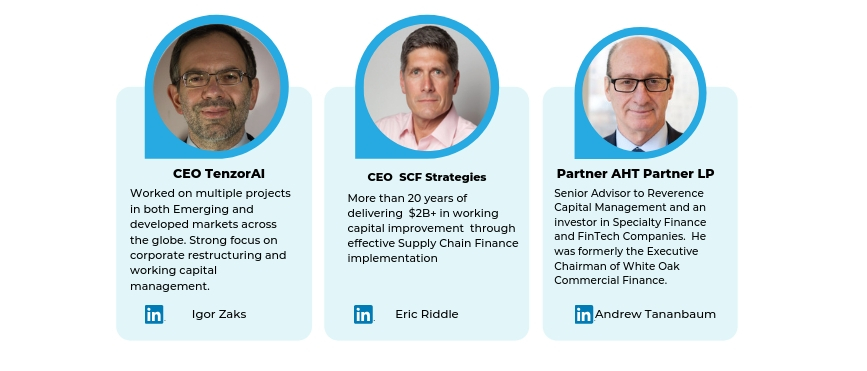

In this interview series, we heard from 3 Supply Chain Finance experts and learned about the developments in the sector and the best of practices SCF implementation. TFG’s Persiana Ignatova spoke to Igor Zaks, Erick Riddle and Andrew Tananbaum, who are members of World of Open Account (WOA).

Persiana: Thank you so much for doing this with us! To start off, please tell us about your involvement with the WOA community?

Igor: I am an advisor to WOA, mainly focusing on two learning labs, New Technology & Fintech and SCF – Buyer-led Receivables Finance. In this capacity, I have been presenting in a number of webcasts/roundtables. I also recorded (with my colleague from TenzorAI) a webcast on using Artificial Intelligence in Receivable Finance.

Eric: I have known Erik Timmermans for years and was excited to join the community as an inaugural advisor. I remain excited for the future and potential for WOA to continue to have an enormous impact on the space

Andrew: I am on the initial Steering Panel of WOA which is composed of representatives from founding members and of some of the early Strategic Advisors.

Supply Chain Finance vs. Reverse Factoring: What’s the difference?

Persiana: What is Supply Chain Finance / Reverse Factoring? What are the trends in SCF over the last 24 months?

Igor: There are multiple definitions of Supply Chain Finance (such as essentially catch-all ICC definition), however, the majority of banking operations are focused on “plain vanilla” buyer-centric reverse factoring on the back of various technology platforms. In the current environment, both margin pressure caused by most players focusing on the same clients and structure and accounting/regulatory pressure asking for transactions to have “right” economic substance means the industry needs to look at different types of structures/risks. This means either going to a wider range of buyers (that require better credit management tools) or going to structures involving some sort of performance risk (that requires better tools to measure and manage such risks)- the ability of the market participants to adopt in both areas will significantly reshape the market.

Eric: Supply Chain Finance/Reverse Factoring is the interconnection of an Anchor Buyer with their Suppliers, usually facilitated by a technology platform, which allows a third party funder to insert themselves into the funding and payment flows. The Buyer typically obligates themselves to an Irrevocable Obligation to Pay contract which the Funder then uses to assess payment risk on the Buyer, which is then used to extend early funding opportunity to the supplier. Over the past 24 months, space has been evolving quickly noting a few key developments,

- Data-Driven credit decisions are being made rather than traditional methods

- Blockchain continues to advance in deployment, adding to the data available to support the extension of credit based on operational certainty and performance

- SCF programs are moving down toward the middle market, away from large public Anchors as a result of the availability of data.

- Regional Banks have begun to offer SCF programs and their sophistication advances and they fight to compete with the Fintech space

Andrew: SCF is domestic and crosses border open account accounts receivable finance and factoring, both with and without recourse. Reverse Factoring is when the account debtor agrees to irrevocably pay its obligations on the due date without offset, counterclaim, dispute or deduction. The new trend is to adopt new POS cross border payment mechanisms, service smaller SMEs, and non-investment grade account debtors.

Off-balance sheet financing: SCF and Factoring Programmes

Persiana: What are the challenges corporates face when it comes to supply chain finance? How has the market changed in the recent macroeconomic climate?

Igor: The biggest challenge corporates face is lack of clarity in the way these transactions are treated, including accounting treatment, rating agencies and securities regulators. There is also limited credit appetite outside of major corporate clients from banks (non-bank players try to address it, but lack of liquidity and relatively expensive pricing limits its penetration). Going outside of confirmed payables space it becomes even more challenging as banks and even many non-bank financiers do not have efficient tools/models/methodology to access such risks.

Eric: SCF still faces uncertainty and ratings and compliance agencies still do not address the accounting treatment for the credit extension associate with these programs and their impact on the Buyer’s balance sheet. Additionally, most corporations still struggle with supply chain instability as a result of their SCF programs primarily reserved for the “top” of the supply chain where the bulk of the money spent lies. The “long tail” still struggles for low-cost capital in tight credit markets around the world. Most banks led SCF programs to stay limited to the top of the chain and Buyer opportunity remains limited in terms of Working Capital.

Andrew: The challenges, in my opinion, are fundamentally the same. Meaning as more suppliers want to sell directly to SMEs, KYC, AML and underwriting trade credit and assuming supplier or customer risk is the same but many more customers with smaller balances. The market has changed because FinTechs are trying to solve the problems with AI and Big Data.

Supply Chain Finance Standards: What are your thoughts?

Persiana: Do you think standardisation (of terminology) is achievable in the SCF space? Why is it required?

Igor: I think standardization terminology is achievable (as was attempted by ICC) but serves little purpose so far as transactions stay private (as opposed to platforms) and accounting treatment is not standardized (i.e. the definitions are not synchronized between market participants, auditors, rating agencies, etc.).

Eric: Yes, associations such as WOE and ICC are helping to standardize terms by bringing industry experts together to help define the space and its components.

Andrew: I have never been too concerned with this issue when discussing the SCF in all of its forms.

Persiana: What is the most interesting part of your role in supply chain finance? What do you enjoy most about your job?

Igor: I have a dual role in this segment, as an advisor (through Tenzor Ltd.) and a technology company (TenzorAI). One allows me to focus on building a strategic bridge between corporate needs and ability of finance providers to serve them, and another to focus on technology gaps allowing the business to deal with a variety of risks in such transactions.

Eric: I simply LOVE the impact an effectively implemented SCF program can have on the working capital for both a Buyer and their suppliers. This is truly a profound way to reduce the burden of working capital in a business and relieve the stress on both sides.

Andrew: To me being a leader in import finance since the 1980s. Seeing the changes from LC-based finance to open account and inventory finance. Opening an office in China in 2010, one of the first, and doing cross border reverse factoring with Chinese suppliers. Starting a 3PL logistics company in 1990 to supplement my import finance business.

Persiana: Can you share any stories or examples of how your company is making a difference to others, or how you’re making an influence in your sector?

Igor: We always see our businesses as an important part of the community and try to share our expertise and ideas with a wider audience.

Eric: I have worked with the IFC and several large banks around the world at a wholesale level to teach them world-class, best practices associated with selling and implementing SCF programs. It’s an extremely rewarding experience to watch a client succeed with this valuable tool as they bring revolutionary value to their clients on a broad scale.

Andrew: With my years of experience as an entrepreneur, the influence I can have and the wisdom I can share is now with respect to startups both speciality finance and FinTech and with respect to those companies in need of growth capital.