Every day FinTech companies bring in streams of new technology and potentially “disruptive models” that are changing the world of open account finance for the better. FinTechs can help bring efficiency into markets, automate, process and bring about major efficiency gains by removing legacy operations. FinTechs are enablers of straight-through processing, speeding up transaction times and less manual intervention. They are completely transforming the transaction banking landscape through platforms and marketplaces. We’ve still just scratched the surface when it comes to advanced machine learning, big data and AI, and ultimately, it’s down to the FinTechs that are transforming the world of open account trade.

In this interview series, we heard from 3 FinTech experts and assessed the real, viable applications of these technologies within international trade and open account. TFG’s Persiana Ignatova spoke to Andre Casterman, Kevin Day and Christopher Spoerry, who are members of World of Open Account (WOA). How is tech enabling trade?

Open Account Trade and FinTech’s

Persiana: Thank you so much for doing this with us! To start off, please tell us about your involvement with the WOA community?

Christophe: Thank you! Well, firstly I am just a member, trying to learn more each day about our sophisticated industry. I also try to help on questions regarding innovation and FinTech.

Kevin: We, LendScape were one of the first companies to become a founding member of WOA because we recognised that, although there are numerous local associations for receivables finance, there was no open, international forum for this type of finance. We are huge advocates of collaboration to drive the industry forward for the benefits of SMEs everywhere and the global economy.

Andre: I am a Learning Lab facilitator within WOA. The learning lab is entitled “Receivables as an investment class” and is chaired by Tradeteq. Christoph Gugelmann, founder and CEO of Tradeteq regularly provides deep insights on this emerging asset class and brings his investment banking expertise to this market, together with co-founder Nils Behling, CFO at Tradeteq. WOA runs quarterly webinars on this topic involving additional experts such as originators and non-bank investors.

TradeTech Explained: Data, Platforms and AI

Persiana: What are the FinTech trends in the open account trade space?

Christophe: In my views, the trends that are progressively reshaping open account trade a broader than purely FinTech: most of the influence we see comes from:

1. the platformization of trade, in particular through marketplaces,

2. the explosion of data combined with the unprecedented possibilities offered by data science, and

3. the gap between the capabilities of incumbents who mostly run on outdated technologies and the quasi limitless funding offered to startups to disrupt the industry.

Kevin: There is no doubt that FinTechs have added excitement to the open account trade space. The accessibility and ease of use of these lenders/facilitators has driven more established providers to invest in customer journeys and simplify their propositions. They have yet to achieve scale and it is interesting that banks are now partnering or acquiring FinTechs to enhance their offerings.

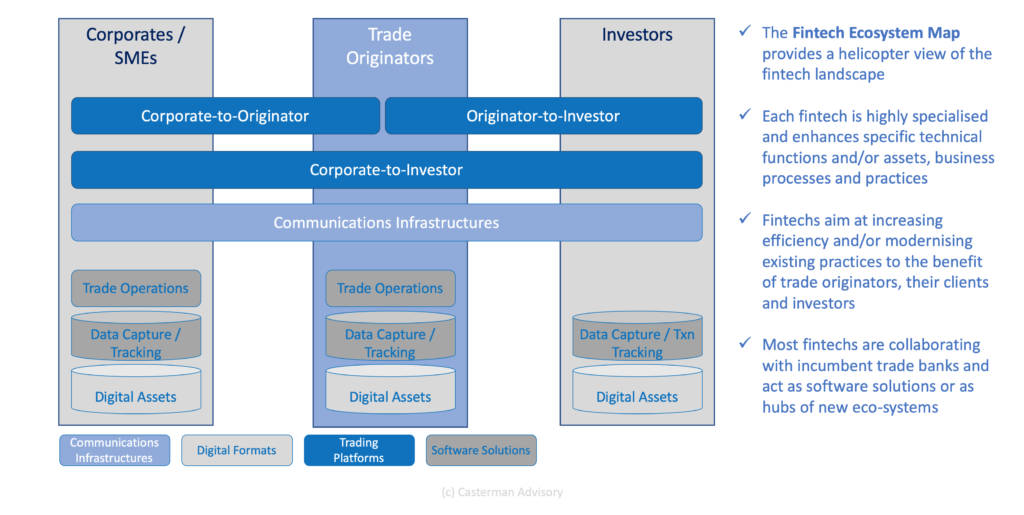

Andre: Trade finance is a wide and complex eco-system. One must identify the very segment or function that each particular “FinTech” is targeting. To help banks, I created a high-level chart so they can more easily map the various FinTechs to the eco-system. Most of the fintechs are highly specialised and some of them are working together (e.g., INTIX and Tradeteq on ML-based transaction-level credit scoring). Some of those fintechs are acting as software providers (e.g., INTIX, Traydstream) that banks can use independently of the technologies used by their counterparties whereas other fintechs operate community-centric trading platforms (e.g., Tradeteq, Fineon Exchange, Mitigram) so counterparties use a common technology hub to communicate and make deals.

FinTech’s Versus Banks: Competition or Collaboration?

Persiana: Are the FinTechs competitors or collaborators of the traditional financiers?

Christophe: Both – as in many other industries who experienced similar revolutions in the previous decades, what we are experiencing is a coopetition relationship, where new entrants and incumbents are both cooperating and competing with each other. What got me really excited in the previous months is the fantastic potential of ecosystem-wide innovation – and this is why I joined AREA42 as an entrepreneur in residence actually: in trade finance, and in open account trade, in particular, the most powerful and disruptive moves involve entire ecosystems, not just sporadic innovations from a FinTech or from a traditional financier. And AREA42 is one of those ecosystems where the future of the industry is being discussed and built, this is exciting.

Kevin: I would say a mixture of both. On one hand, they may well be “fishing in the same pond” for business, but it’s also true that they have created new market opportunities, especially with micro SMEs, where the ticket size versus the cost-to-serve are not viable for traditional financiers. The opportunity to collaborate with FinTechs is already being seized upon by established providers.

Andre: In trade finance, FinTechs are mainly collaborators of the incumbent institutions. This is specific to trade finance and different from payments where many FinTechs compete with banks. Most of the top transaction banks are now working with several FinTechs. This trend will continue as FinTechs become successful.

Traditional Finance Versus Alternative Finance

Persiana: Through what ways can FinTechs help financiers streamline their businesses?

Christophe: Fintechs and startups, in general, are fundamentally about exploring new, better business models. This is not really about streamlining the existing business, it is more about not missing the future of the business.

For example, most traditional financiers in open account trade are completely missing very important trends and subsequently new segments, that their current business models are unable to address: SMEs and freelancers, marketplaces and platforms, blockchain-based businesses, … Fintechs, corporate-startup studios, and startups, in general, have the risk appetite and the incentives to crack those new segments.

This being said, a number of FinTechs and startups are also about streamlining the traditional Financiers’s businesses, because of the capabilities gap of these financiers: this is a rather sad consequence of years of cost-driven management of these financiers with too little care and understanding of technology, R&D and upskilling of the teams. The best way to fix these gaps is to track at financier’s group level the percentage of services that are sourced from FinTechs vs from incumbent suppliers: in my experience, this is a very efficient way to progressively catalyse a culture of collaboration with innovators in the legacy business.

Kevin: The area of on-boarding and digital engagement with borrowers has been one where FinTechs have used technology to enhance and accelerate this process. The established players may have more robust back-end systems and processes, developed through many decades of economic ups and downs, that can provide an interesting “best of both worlds” offering to customers.

Andre: Through my research, I identified 4 industry trends where FinTechs help trade banks: “trade digitisation”, “data as an economic asset”, “trade finance automation” and “trade finance gap”. I mapped 20 FinTechs to those 4 trends. Take for instance the checking of documentary credits which is all about automating trade finance back-office processes. Traydstream, as an example, is helping banks achieve this by adding machine learning OCR and document validation next to existing back-office processes and systems. This is providing an augmented intelligence to internal operations teams, accelerating document scrutiny and reducing Days Sales Outstanding for exporters. This is a very promising space for banks to gradually digitize key paper-based processes as well as staff knowledge.

Are We In A Fintech Bubble?

Persiana: Are we in a FinTech Bubble?

Christophe: Where did I put my crystal bowl? (laughing) Jokes apart, I believe the FinTech wave is here to last, and we have not seen the summit yet. The valuations are already quite high in the B2C FinTech and SaaS verticals, but the trend is just starting in TradeTech, B2B FinTech, B2B InsureTech, reg tech … The amount of funding that is available for competent innovators and founders, to crack the numerous segments left by traditional financiers, is mind-blowing. This combined with uncertain horizons in trade finance fueled by protectionism and trade wars will lead to a big unbundling of how open account trade is financed in the coming years.

Kevin: I am old enough to remember the “dot.com” bubble of the turn of the century and there are similarities, in particularly the amount of investment FinTechs attract with valuations that seem hard to justify. I think the difference is that, unlike many dot.coms fantasies, the FinTechs are generally targeting legitimate needs. The challenge they face is channels to market, liquidity and untested risk algorithms. This is where established providers can form meaningful partnerships to address these areas.

Andre: I don’t think FinTech is a bubble. The FinTechs I am working with are delivering tangible value and addressing short-term pain points. They win clients and increase their market valuation every month. If any bubble, I would think about the huge funding of pure blockchain initiatives which might be successful in some 5+ years from now.

A Day in the Life of a FinTech

Persiana: What is the most interesting part of your role within Fintech?

Christophe: Most recently, this was when we made the team of an ambitious new marketplace really excited about how trade finance could help them deliver on their vision. This marketplace is founded by proven entrepreneurs who launched and scaled up several international platforms, and yet they had never found the solution to properly offer credit to B2B buyers while paying B2B sellers as early as possible. We worked with the marketplace experts at Marjory and with a visionary trade credit insurer, and we delivered what is probably the most forward-looking “open account trade as a service” solution to date.

Kevin: We are a technology provider and are really excited with the general digitalisation of commerce and the opportunities it creates to enhance the ease of use of receivables finance and the amount of finance that SMEs can benefit from. There is lots of activity and, no doubt a few false dawns, but the energy, creativity and innovation make this an exciting market.

Andre: Fintechs that are highly specialized and don’t get distracted will be successful. As I am advising FinTechs, I insist on how crucial it is to focus on real pain points and to deliver value in the short term. One has also to track market trends and spot emerging needs to expand value propositions in the right direction. This makes the job very interesting and convincing bankers about those new FinTech value propositions is a pure delight.

Trade Finance and the Community

Persiana: Can you share any stories or examples of how your company is making a difference to others, or how you’re making an influence in your sector?

Christophe: Our name embodies our most important value: Alpine Style. “Alpine style” refers to Himalayan mountaineering in a self-sufficient manner, as opposed to “expedition style” which uses a fixed-line of stocked camps, fixed ropes, sherpas, supplemental oxygen. As a venture builder, we invest in and build ventures ourselves, but we also have “venture builder as a service” activities, which have helped financiers, insurers and brokers to explore and launch new lines of business faster and with lower risk than when managing disruptive innovation internally. Alpine Style allows to go faster and to conquer new lines of business.

Kevin: We have invested heavily in the “user experience” for receivables finance. Our technology enables funders to offer a digital solution to its customers, where receivables data is automatically collected from the accounting system of the borrower to allow real-time, dynamic access to funding. Our online portal for suppliers and buyers is designed to be easy to use, but also provides lots of added-value features to enhance the experience of users and ensure that they maximise the benefits from receivables finance, whilst ensuring proper risk controls to protect lender and borrower alike. We are working with numerous start-up funders all over the world, in particular in Africa, the Middle East and Asia. We have focused energy on allowing these startups to benefit from the very best in technology, whilst reducing costs and barriers to entry.

Andre: I strongly believe in creating eco-systems where market-wide ambitions get executed with huge impact. Banks created SWIFT some 50 years ago when they realised they needed to automate the telex. This was visionary and it has become a 12,000-member strong community. My current focus in on creating a new eco-system in the trade finance distribution space also called the secondary market. This is the goal of the Trade Finance Distribution Initiative and Tradeteq. We are already working with 30 financial institutions to progress this collaborative ambition. Thanks for such efforts, it will become much easier for trade originators to engage with many more bank and non-bank funders. This has become a key objective for most trade banks given the stringent regulatory environment. This initiative will also help trade banks originate more flows from their clients as they get new tools to cope with balance sheet constraints. We call this moving to an “originate-and-distribute” model.