Estimated reading time: 4 minutes

Both ‘bill discounting’ and ‘invoice factoring’ are types of financial instruments that are used to provide working capital to businesses from accounts receivables (i.e., unpaid invoices).

The terms are often used interchangeably, although technically speaking this is incorrect.

In this article, we outline the key differences between the commonly used terms ‘bill discounting’ and ‘invoice factoring’ – but first, let’s examine what each is in its own right.

Bill discounting explained

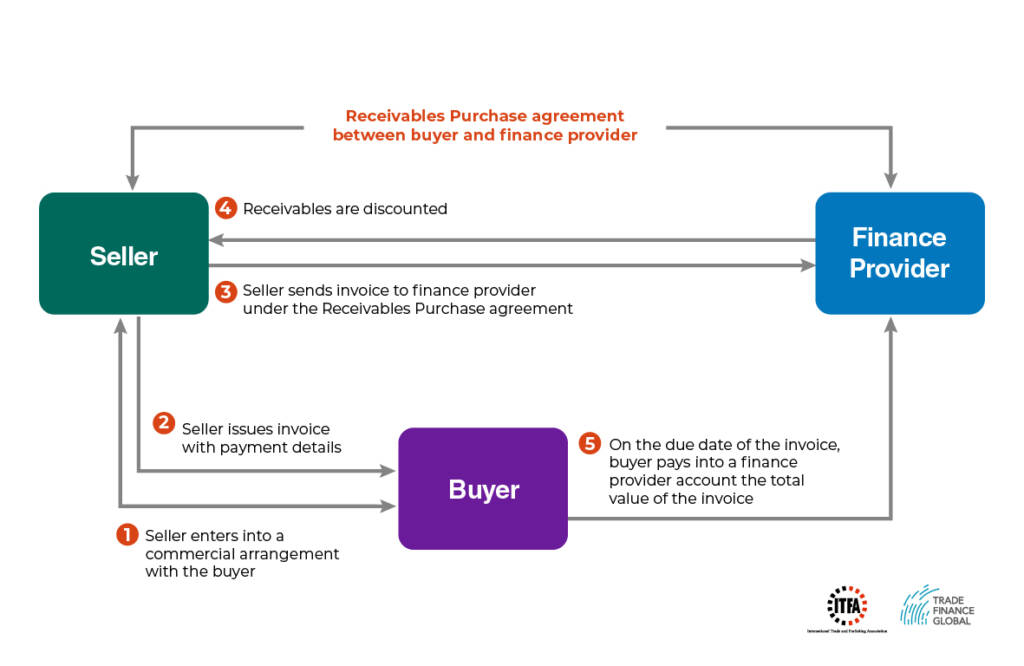

Bill discounting, or invoice discounting, is the act of sourcing working capital from future payables. Furthermore, the seller recovers a number of sales from the financial intermediaries before the due date.

Bill discounting can be defined as the advance selling of a bill to an intermediary (an invoice discounting business) before it is due to be paid.

This results in fewer administrative charges, fees, and interest. The interest and fee are calculated based on the risk of non-payment from the buyer, and so a funder will look at the creditworthiness and trading history of the customer rather than the business it is funding for payment.

In this arrangement, the initial owner of the invoices that are sold is still in control of its own sales ledger and will chase payment in the usual way.

Invoice factoring explained

Invoice factoring involves a third party which is placed between the buyer and the supplier.

The third party – who is the factor in this scenario – purchases a company’s accounts receivables (unpaid invoices) at a discounted rate.

This gives the company in question access to a pool of funds that were tied up in the future and it gives the third party higher value debt which will eventually pay.

There is also a concept of reverse invoice factoring which is where the third party commits to paying the company’s invoices at an earlier date in exchange for a discount.

The reverse factor then takes its fees out and passes them on to the company involved.

Bill discounting vs Invoice factoring

While the concepts are largely similar, the main difference lies in which party takes the liability of the sales ledger and which one claims the responsibility of collecting payment.

Correspondingly, there is an essential variation in the confidentiality surrounding the instrument:

Invoice factoring in 30 seconds:

- The third party takes responsibility for the sales ledger, and will also carry pursue payment collection and credit control surrounding the transaction.

- The customer will settle their invoice with the third party factor. Consequently, customers are more likely to be aware of the factor arrangement in place, which may cause issues as the company is technically accepting a lower price.

Invoice discounting in 30 seconds:

- The original company that owns the accounts receivables will continue its obligations to collect payment and maintain the sales ledger.

- The customer will still pay the company directly, and not the third party. Therefore, the customer has no means of knowing – or right to know – about any discounting arrangement applied to the transaction.

Invoice financing has many benefits for small and medium-sized businesses, the main being a material improvement in the business’s access to liquid cash.

Other benefits include:

- Improved cash flow and working capital

- Quick access (since funds can be released within 24 hours)

- Risk transfer (since the risk of bad debt or non-payment can be passed on to the financier)

- The borrower only pays on the amount of money used, unlike a business loan

Invoice financing is also considered beneficial for smaller or newly established businesses that do not necessarily have a robust credit rating to lean on.

This is because the decision to approve funding is not based on the strength of the firm that is being financed, but rather on the strength of the firm that is ultimately paying the invoice.

A business without a strong credit rating then may be able to secure financing through invoice financing when they are unable to secure another form of a loan.

The devil is in the detail

As with all invoice financing products, it’s important to understand where the liability and risks lie in the transaction.

As a business, it’s important to understand your obligations in such transactions.

To learn more about the various trade finance techniques and what to be aware of for each, check out our SME trade and export finance guide.

At Trade Finance Global, our global team of receivables and invoice finance experts are here to help your business. Visit our receivables finance hub here, to see how you can access discounting or factoring services.