Normal may soon be very different. Amidst the growing fallout of Covid-19, many once-normal aspects of commerce and lifelike business processes, ways of working, and social attitudes will be forced to change. These changes may mark the beginning of a new normal. A normal that, for better or worse, has been kickstarted by this global pandemic. The changes that are taking place are not just related to how we work. The past few weeks and months have seen unprecedented measures taken to quell the spread of a virus that just 100 days ago no one had even heard of. In the midst of a widespread mix of cancellations and closures, many people are bombarded with virus-related information, carrying mixed levels of reliability.

Sifting through this information and understanding what impact the 2020 pandemic will have is a difficult task with changing answers across various industries and situations. When it comes to global trade, the situation seems even more unpredictable than ever.

At Trade Finance Global we strive to unpack the hype around a given topic and narrow in on the reality as indicated by current data. To try and make sense of the impact that the novel Coronavirus will have on the international trade industry, we must first look at what has already occurred.

Here’s what we know about the events that have unfolded

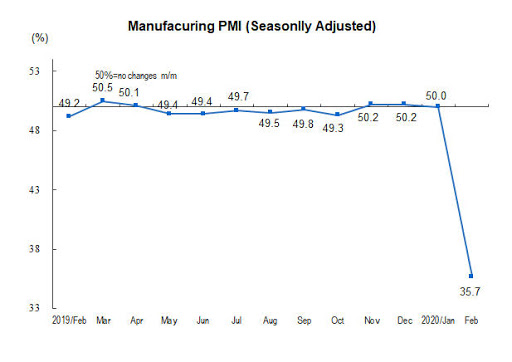

In February, production in China was predominately brought to a grounding halt by lockdowns put in place to help stop the spread of the virus. The China Manufacturing Purchasing Manager’s Index (PMI), a critical production index, was driven down around 22 points in February. This index correlates heavily with exports and a decline of this magnitude implies an annualized reduction in exports of approximately 2 percent. Another index, the Shanghai Containerized Freight Index has also experienced steady declines through February. Changes of this nature indicate a growing excess of shipping capacity likely brought on by a lower demand for container vessels. These two indicators together paint a more cohesive picture: less goods are coming out of China to be shipped worldwide.

This sharp decline of Chinese exports carries many downstream supply chain implications. According to the United Nations Conference on Trade and Development (UNCTAD), around 20% of manufacturing intermediary goods originate in China. This Covid-19-induced slowdown of Chinese production of intermediary parts, coupled with the increasingly prominent practices of Just-in-Time inventory management and Lean manufacturing has the potential to soon leave any non-diversified manufacturing supply chains out of materials. Unfortunately, it is no longer just China. As the virus has spread worldwide, so too have the lockdowns and closures. Given this, any company not directly impacted by the virus itself will surely be experiencing considerable disruption at some downstream portion of their supply chain.

Sparked by this potential disruption and further fueled by fear, the broader financial world has experienced quantifiable declines. Since February, the Dow Jones Industrial Average has lost nearly 35% of its value, with the S&P 500 and Nasdaq indices both trading around 30% lower in the same time frame. It is no secret that the state of financial markets holds considerable importance for the global trade ecosystem, and the global economy as a whole. This forces us to ask the question, what does this all mean for the broader trade industry going forward?

What does all of this mean for trade?

The short answer: It is difficult to tell.

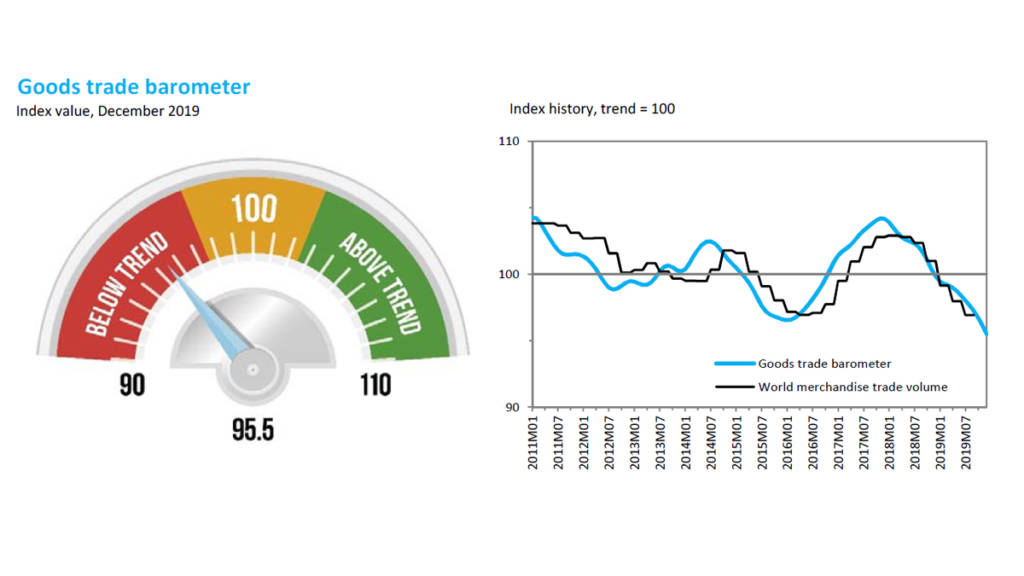

The World Trade Organization (WTO) is expected to release their annual trade forecast in the coming weeks, but the organization has noted that the rapidly changing situation is causing economists to revise their forecasts almost daily. The WTO’s Goods and Services Trade Barometer, issued on 11 March, shows a weakening of trade growth at the end of 2019. While the indicator does not yet fully reflect the economic impact of the COVID-19 virus and the WTO has suggested that it may decline further in the coming months.

Reductions in global trade could have wide-ranging impacts on the broader economy. Euler Hermes has predicted that the Eurozone GDP will contract by -1.8% in 2020 should the full lockdowns last for one month, or by -4.4% should they last two months. Many estimates suggest that the near-lockdown measures currently in place in much of the world today will continue beyond this 2-month threshold, with some suggesting they may continue for 18 months.

The good news for trade, is that no matter how many social distancing or state imposed lockdown measures are put in place, people will still need stuff. And trade, as it would be explained to a toddler, is all about getting people the stuff they want. This, coupled with the fact that many of the global restrictions and border closures do not currently apply to commercial trade, seems to show that trade will not be exorbitantly negatively impacted in the coming months. Goods will continue to flow.

This scenario seems to rely on the assumption that the state of the world will not drastically change overnight, a generally safe assumption to make in normal times to avoid an overzealous analysis by paralysis. These, however, are not normal times. In a month that has seen the unprecedented cancellations of a wide array of face-to-face work, cultural events, and sports seasons, anything is possible. That’s real March Madness. What would happen to trade if the current border restrictions are expanded to also prevent goods from crossing borders? What happens if producers become unable to produce goods at all? Questions like these, once relegated to the domain of doomsday action movies, seem all the more likely to need to be addressed.

Furthermore, it seems important to note that the global economic slowdown the world is experiencing has brought about larger than normal levels of (hopefully temporary) unemployment, particularly among the travel and hospitality industries. High unemployment naturally brings about a growing state of unrest and uncertainty. Will these increasing levels melt away public support for liberal trade policies, pushing nations ever further into a nationalistic mindset, heavily favouring domestic over foreign anything? Again, any answer to this question would be highly speculative.

While the future remains unclear, we can turn and look at how events have unfolded in the past. In the wake of the last global financial crisis, the 2008 sup-prime mortgage crisis, the WTO estimated that global trade volumes fell by around 12%. It seems entirely possible that a decline of this nature may occur again, with global markets in decline and overarching fear and uncertainty preventing individuals and organizations from making larger purchases or other financial commitments. On the other hand it seems possible that this will not be the case. People around the world have had their entire lives upended to help wage war against this virus. Perhaps, once our modern day enemy has been driven off the field of battle, an overwhelming desire to return to normalcy will take over the world, driving global demand for goods and services. A situation that would require a strong global trade system.

Impact on trade finance

Trade finance has been building a reputation as a safe asset class over the last few years. According to the International Chamber of Commerce (ICC), default rates between 2008 and 2018 in all trade finance regions were low, sitting at 0.76% for import and export loans and dropping to as low as 0.05% for instruments like export letters of credit. Covid-19 seems set to disrupt this. Many firms are experiencing severe working capital restraints as they are experiencing temporary shutdowns and rapidly decreasing demand. These conditions will disproportionately impact this Small and Medium Enterprise (SME) sector, increasing their default risk in the process. Given that this has already been the type of firm most affected by the $1.5 Trillion trade finance gap, the outlooks do not look good for extending credit to these firms.

With this in mind, it is important to note that many countries, including the United States, have or are in the process of approving massive economic stimulus packages that will aid their economies and SMEs in remaining afloat during these uncertain times. Such stimulus package announcements have had positive effects on the global stock markets, but their impact on global trade finance is currently yet to be realized. In addition to these packages, the International Institute of Finance (IIF), along with many development and multilateral development banks, have released a 5-step policy response plan for combating the economic fallout from Covid-19.

Despite its vast negative implications, the Covid-19 pandemic may be inadvertently accelerating trade digitization. As many companies have implemented work from home policies and social distancing measures are encouraging people to conduct their daily lives from within their own homes, many companies and banks are being forced to implement or scale up their digital offerings. Existing technological solutions are available for logistics and trade. Rapidly implementing them out of the necessity that the current situation is presenting will be an excellent step in the right direction for trade digitization on a broader scale as we transition to the post-Covid-19 new normal.

Podcast: Development banks step up in the fight against COVID-19: Asian Development Bank

Recent Stories from the TFG COVID-19 HUB

- [April 6 2020] Oil falls 12% on doubts over any Saudi-Russia deal

- [April 3 2020] WTO issues new report on worldwide trade in COVID-19 medical products

- [April 3 2020] UKEF expands protection against non-payment for UK exporters in response to Coronavirus

- [April 2 2020] Pandemic to accelerate digitisation of global trade, say trade authorities

- [March 26 2020] Financial crime levels increase as COVID-19 pandemic grows

Conclusion

Given the rapid spread of both the virus and the information pertaining to it, any data and information about Covid-19 and its fallout is bound to be outdated the moment it is collected. Accepting that any picture we have of the situation is bound to be both incomplete and imperfect, the best we can do is try to make sense of what has been presented to us. At the end of the day all we can say for sure, is that the world as we know it in this moment remains veiled in a complexly interwoven shroud of medical, social, and international uncertainty.