- A compelling submission to an insurer includes trading history, recent financials, credit memos, and deal structure detail.

- Common pitfalls include lack of transparency, inconsistent purchasing behaviour, and cherry-picking policies.

- A frequent misconception is that insurers seek to avoid paying claims, when in reality their business depends on doing exactly that.

Insurance is built on trust. An insurer will look for signs that help build that trust with a new client, such as transparency, good communication, cooperation, and an understanding that they are entering a partnership relationship, in which risk is shared, not transferred entirely.

At Aon, we see clients large and small, and this chapter serves as a cheat sheet as to what an insurer is thinking when you approach them.

What does a strong insured look like in practice?

1. Communicate a clear strategy

It helps to start with a clear insurance strategy. Why are you looking to insure? While mitigating risks is the obvious rationale, it’s often not the main driver for the market or for our clients.

More commonly, it could be:

- Access to finance through lending;

- Building on internal credit limits to grow larger trading lines; or

- Achieving a competitive edge against industry peers through obtaining highly sought-after capacity on counterparties.

Communicating a clear strategy will help the insurers understand your motivations, build that trust, and greater support will be provided.

2. Demonstrate risk appetite and initiative to grow

We also see great support for those clients who can show signs of a strong risk appetite. In essence, those who are not simply looking to offload risk, but use the insurance market as a means to strategically build a partnership to share risk and enable more trade and business growth.

Typically, credit insurance is structured on a 90% indemnity basis, meaning the insured holds, at minimum, 10% of the risk, colloquially referred to as ‘skin in the game’. If the insured can share a greater percentage (20-50%, perhaps), this is a good sign for the insurer.

Alternatively, if the insured can demonstrate that they are comfortable with holding exposure above and beyond the insured limit, this will help the insurer look more favourably on them.

Insurers favour insureds who undertake a considerate share of risk, and not just offload the poorly rated counterparties into the market.

Other elements that help build a good case are:

- Strong trading history with the counterparty(ies), for example, having an ongoing relationship for a number of years, significant volumes being traded, and a lack of adverse experiences

- Recent financials for the counterparty(ies)

- Credit memos (sharing of the insured’s due diligence on the counterparty(ies)

- A strategic angle to the underlying trade/ project

- Deal structure, e.g. bank/ letter of credit (LC) support

- Clear communication of the motivation for purchasing insurance

Sub-investment-grade insureds

Understandably, an insured will find a lot more support for an investment-grade risk (risk associated with securities that have a relatively low possibility of default) than one rated BB (has the capacity to pay, but exposed to economic shifts) or lower. Although there is a pool of insurers who will consider covering risks sub-investment grade, the supporting factors discussed above and below need to be that much stronger to justify coverage and convince the insurers to take on the risk.

Factors that are compelling for an insurer to cover a lower graded counterparty include a stronger parent company that will step in, such as a parent company guarantee. Or, if the underlying transaction is strategically important, such as one supplying power to a national institution (a necessary and fundamental product to daily life).

Essentially, under circumstances where there would likely be external (such as state) support for the counterparty if anything went wrong, the likelihood of a loss is reduced.

Common red flags that reduce coverage

- Lack of transparency: the insured not sharing information

- If the insurer has experienced a previous serious loss in a certain sector: a broker may have this information if they regularly see similar cases, but it’s certainly not an expectation that they or an insured should know about the market’s experience.

- Experience of an insured’s inconsistent purchasing in the insurance market (cherry-picking insurance policies, rather than investing in building trust and a market relationship)

Confidentiality and sharing of data

As brokers, we are often questioned by clients about the sharing of sensitive commercial information, and there is an understandable reticence around doing this.

As stated above, the insurance market was built on trust. It still is, but we also have many more checks and balances to ensure client confidentiality and embed non-disclosure into day-to-day insurance market activity.

All policies are confidential, as bound by the insurance contract. Brokers have terms of business agreements with all insurers they transact with, including terms on the protection of confidential information.

If clients require another level of comfort, we can arrange non-disclosure agreements with a client and the market.

Common misunderstandings

- Insurance can be a great enabler, not just a risk mitigation tool.

- Not all insurers have great insight into our clients’ counterparties, and they highly rely upon the information provided by clients to help with their risk consideration.

- On any given inquiry, the more detail that can be shared, the better on any given enquiry. This will not jeopardise a client’s commercial relationship due to the confidential nature of insurance.

- Insurers are working to support clients, not avoid risk or escape claims. If they didn’t pay claims, our market would not exist!

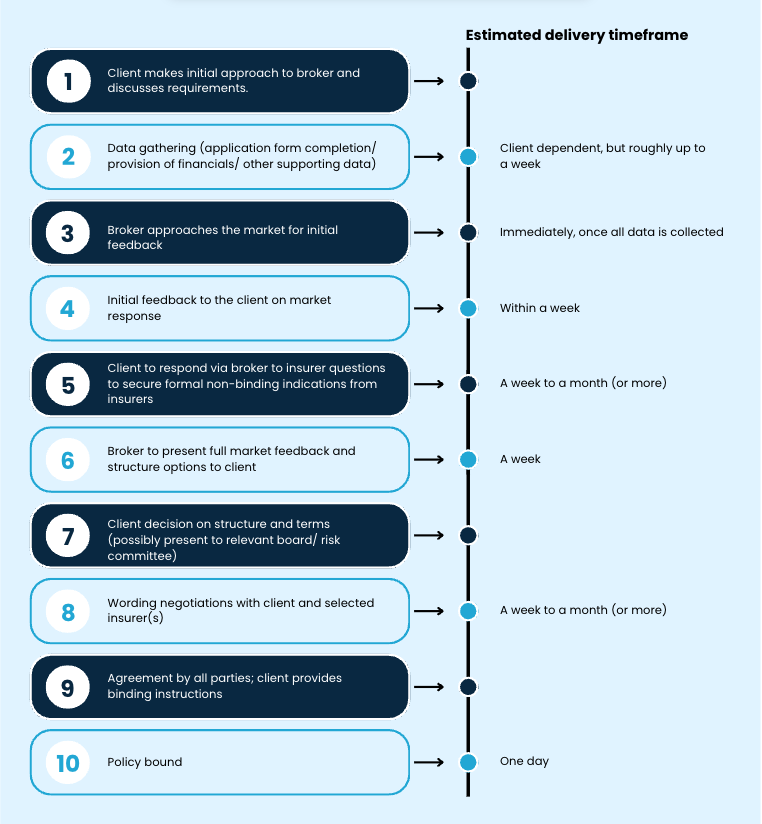

Credit insurance timeline: From inception to delivery

The following provides a very high-level example of how a new credit insurance enquiry becomes a policy, with estimated timeframes. Each case is different, and this should be taken as a very rough guide.

Case study 3: Aon and an international energy company

An international energy company (the insured) was struggling with internal limits on counterparties. They were new to the market and needed to establish a strong foundation relationship to get the support they required.

The energy company had a good appetite to share risk with the insurance market.

The counterparties were a mixed bag, buying or trading gas and/ or power under Energy Traders Europe (EFET) agreements, standardised master contracts for trading electricity and natural gas in Europe (being the market standard under EFET).

Aon (the insurer) proposed a portfolio approach to optimise pricing and risk acceptance – the insured provided a portfolio of names to be agreed upon at inception.

Risk share was set at 50%, creating an equal level partnership with the insurer.

A bespoke wording was tailored to the specific needs of the insured, including having:

- A dynamic portfolio of counterparties

- Securities in place

- Flexibility to manage retained exposures

The significant risk share fostered a strong relationship with the insurer and showed the new insured was serious about engaging in a partnership.

The facility allowed the insured flexibility to introduce or exchange counterparties mid-way through the policy.

The insured was able to grow their business with the certainty that insurance coverage will be available.

Options for large corporates

Author: Joep van der Bijl, Short Term Trade Solutions (STTS), Lead Underwriter Continental Europe, Liberty Specialty Markets

TCI can be tailored to a wide range of corporate profiles. For large businesses, the starting point is typically how the solution aligns with their existing risk management approach.

Rather than treating all receivables uniformly, many corporates look for structures that protect strategic key exposures, preserve internal decision-making, and support growth.

At a high level, the main trade credit solutions for large corporates include multi-buyer cover, single-buyer cover, top-up cover, and excess-of-loss structures. Each serves a different purpose.

- Multi-buyer policies are useful for companies seeking broad protection across a selected portfolio of customers, for instance, in a certain sector or region.

- Single-buyer cover is more targeted and can be used to protect a particularly important counterparty.

- Top-up cover extends capacity when existing market limits are not sufficient.

- Excess-of-loss structures allow a company to retain more frequent, smaller losses and transfer only the larger, less predictable ones.

For large corporates, the real value lies in the flexibility to combine and tailor these solutions. In addition, they are not only about protection – they are also an effective tool to enhance access to financing.

Why some of these policy features work well for strong MNCs

Liberty Specialty Markets standardly supports non-cancellable limits, a feature which is particularly valuable for corporates that need certainty. Large multinationals often rely on stable trading relationships and need predictable coverage to plan and support sales, credit lines, and cash flow.

Where a buyer is strategically important, the ability to secure a more durable limit reduces the risk of disruption and provides confidence to both credit teams and treasury functions.

A key benefit for large corporates is the ability to enable receivable financing and to monetise insured receivables.

By insuring exposures – particularly on a non-cancellable basis – companies can:

- Sell or assign receivables to banks

- Access receivables finance/ factoring/ securitisation structures

- Improve liquidity and working capital efficiency

From a bank’s perspective, insured receivables represent a de-risked asset, which can translate into increased advance rates, better pricing, or broader financing capacity.

Discretionary credit limits (DCL) can also be highly effective for large corporates with strong internal credit capabilities. These policies are best suited to companies with mature internal credit processes, strong financial reporting, and experienced teams that already assess counterparties closely.

In these cases, the insurer is not replacing internal risk underwriting but rather complementing it. The insured retains operational flexibility by setting their own credit limits up to a certain level while still transferring part of the risk.

This is especially relevant for excess-of-loss-type structures, where the business is willing to absorb some first-loss itself in exchange for broader support and more efficient cover on key names.

First-loss retention and excess-of-loss structures are often a strong fit for large MNCs because they align with how these businesses manage risk in practice. Many large corporates are comfortable retaining a layer of predictable loss.

What they want protection against is the less frequent but more severe event: a major buyer failure, a regional shock, or a sharp deterioration in a key market. Excess-of-loss cover allows them to protect the balance sheet while maintaining control over day-to-day credit decisions.

This approach is particularly attractive for corporates with:

- Strong credit management and internal controls

- Diversified buyer portfolios

- Significant turnover and concentrated key-name exposure

- Operations across multiple regions

- Appetite to retain some risk in return for better economics or more tailored support

The right structure has the potential to support growth into new markets, provide confidence around strategic customers, and offer resilience during periods of volatility – all on top of protecting risk against non-payment, and tailored to the large corporate’s needs.

In summary…

Author: Silvia Andreoletti, Senior Reporter, Trade Finance Global (TFG)

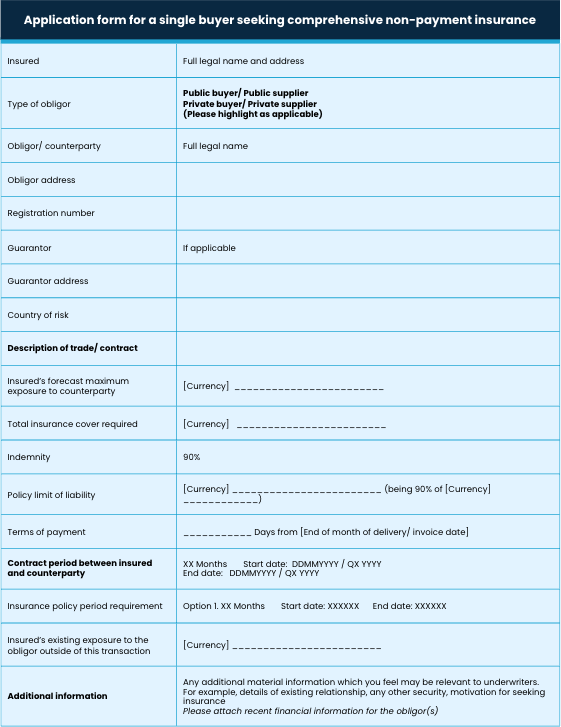

The documents an insurer needs can vary depending on the size of the business it is insuring and the nature of the transactions, but the purpose is always to determine – and verify – the risk an insurer is taking on. These documents will often include:

- The supplier’s/ policyholders’ financial statements: these are necessary to determine the supplier’s/ policyholder’s own financial health, which can influence the credit limit.

- A list of customers, their open account terms, and their payment history: this is used to determine business’ exposure to each client. Customers who have been trading with the business for longer and have always paid invoices on time will be seen as lower risk, while longer payment terms, large transaction sizes, and a history of late or missed payments will make a business higher-risk.

- Details of customers’ financial history: this is especially important if a TCI policy only covers one or a few major customers. If a customer is financially sound, it will carry less risk, so an insurer will be more willing to insure the transaction and propose a higher credit limit.

- Any outstanding, overdue, or unpaid invoices: this helps the insurer understand the bad debt a business already holds and influences the overall risk rating.