Estimated reading time: 12 minutes

Documentary credits and availability

A documentary credit (“credit”, “letter of credit”, “LC”) is a bank undertaking to pay its beneficiary based on the presentation of required documents, provided that the presentation complies with the terms and conditions of the credit.

The ‘availability’ of an LC determines to whom a presentation may be made, and the acts that the bank (to whom a presentation is made) shall or may perform.

An LC may be available with a nominated bank, in addition to being available with the issuing bank.

This means that the beneficiary may ‘avail’ the credit by making a presentation to a nominated bank if one is stated on the credit.

If the LC states that it is available with “any bank”, a presentation can be made to any bank.

A complying presentation made to a nominated bank is binding on the issuing bank, and any confirming bank, which it must then honour.

The issuing bank undertakes to reimburse a nominated bank that has honoured or negotiated a complying presentation and that has forwarded the documents to the issuing bank.

A confirming bank incurs a similar undertaking to reimburse a nominated bank that has honoured or negotiated a complying presentation and that has forwarded the documents to the confirming bank.

ARTICLE: Sanction clauses under documentary credits

As defined in UCP 600, honour means:

- to pay at sight if the credit is available by sight payment.

- to incur a deferred payment undertaking and pay at maturity if the credit is available by deferred payment.

- to accept a bill of exchange (“draft”) drawn by the beneficiary and pay at maturity if the credit is available by acceptance.

Negotiation means:

- the purchase by the nominated bank of drafts (drawn on a bank other than the nominated bank) and/or documents under a complying presentation, by advancing or agreeing to advance funds to the beneficiary on or before the banking day on which reimbursement is due to the nominated bank.

The letter of credit must state whether it is available by sight payment, deferred payment, acceptance, or negotiation.

Sight payment

Payment at sight with a nominated bank means that when the nominated bank determines that a presentation made to it is complying, it will honour it by paying the beneficiary.

To be reimbursed, the nominated bank must forward the documents to the issuing bank, or confirming bank (if any).

If the nominated bank is also a confirming bank, it must pay the beneficiary at sight for a complying presentation.

Unless the nominated bank is a confirming bank, it has no obligation to pay the beneficiary at sight for a complying presentation and may forward the documents to the issuing bank (or confirming bank, if any) for payment.

Deferred payment

If a credit is available with a nominated bank by deferred payment, the nominated bank may honour it by incurring a deferred payment undertaking for a complying presentation.

By incurring a deferred payment undertaking, the nominated bank undertakes to pay the beneficiary at maturity.

The deferred payment undertaking of a nominated bank ought to be expressly communicated and the nominated bank may prepay its deferred payment undertaking if the beneficiary so requests.

To be reimbursed, the nominated bank must forward the documents to the issuing bank, or confirming bank (if any).

Although not mentioned in UCP 600, honour of a deferred payment credit by the nominated bank is logically on without recourse basis to the beneficiary.

This is regardless of whether the nominated bank is a confirming bank because by incurring a deferred payment undertaking, the nominated bank has an obligation to pay at maturity, independent of the issuing bank’s undertaking.

If the nominated bank is also a confirming bank, a deferred payment undertaking is incurred when a complying presentation is made, and the confirming bank must pay at maturity.

Acceptance

If a credit is available with a nominated bank by acceptance, the nominated bank may honour it by accepting a draft drawn on it for a complying presentation.

By accepting a draft, the nominated bank undertakes to pay the beneficiary at maturity.

Before accepting the draft, the nominated bank has to be careful to examine the presentation to determine that it is complying with the credit, as acceptance of a draft represents an unconditional and irrevocable promise by the drawee/acceptor to pay.

Having accepted a draft, the nominated bank or drawee may prepay or purchase its own accepted draft, if the beneficiary so requests.

To be reimbursed, the nominated bank must forward the documents to the issuing bank, or confirming bank (if any).

Honour of credit available by acceptance is without recourse to the beneficiary, regardless of whether the nominated bank that honoured is a confirming bank.

This is because it honours by accepting a draft drawn on itself, and thus incurs its own independent payment obligation under the draft.

If the nominated bank is also a confirming bank, a complying presentation made to it obligates the bank to honour, and it must pay at maturity.

Negotiation

If a credit is available with a nominated bank by negotiation, the nominated bank may negotiate a complying presentation.

UCP 600 has defined negotiation as the purchase of drafts and/or documents under a complying presentation.

The drafts must be drawn from a bank other than the nominated bank, and this differentiates negotiation from acceptance.

(It should be noted that drafts are not mandatory for credits available by negotiation, and the ICC has published guidance to discourage the use of drafts for documentary credits.)

Purchase is by way of the nominated bank advancing funds to the beneficiary before the date that reimbursement is due from the issuing bank.

Alternatively, the purchase may be by way of the nominated bank agreeing (in effect, undertaking) to advance funds to the beneficiary on or before the date that reimbursement is due from the issuing bank (which implies that the nominated bank ought to effect payment to the beneficiary using the nominated bank’s own funds).

To be reimbursed, the nominated bank must forward the documents to the issuing bank, or confirming bank (if any).

If the nominated bank is also a confirming bank, it must negotiate without recourse a complying presentation.

ARTICLE: April 6, 2020; The day trade finance went from paper to paperless

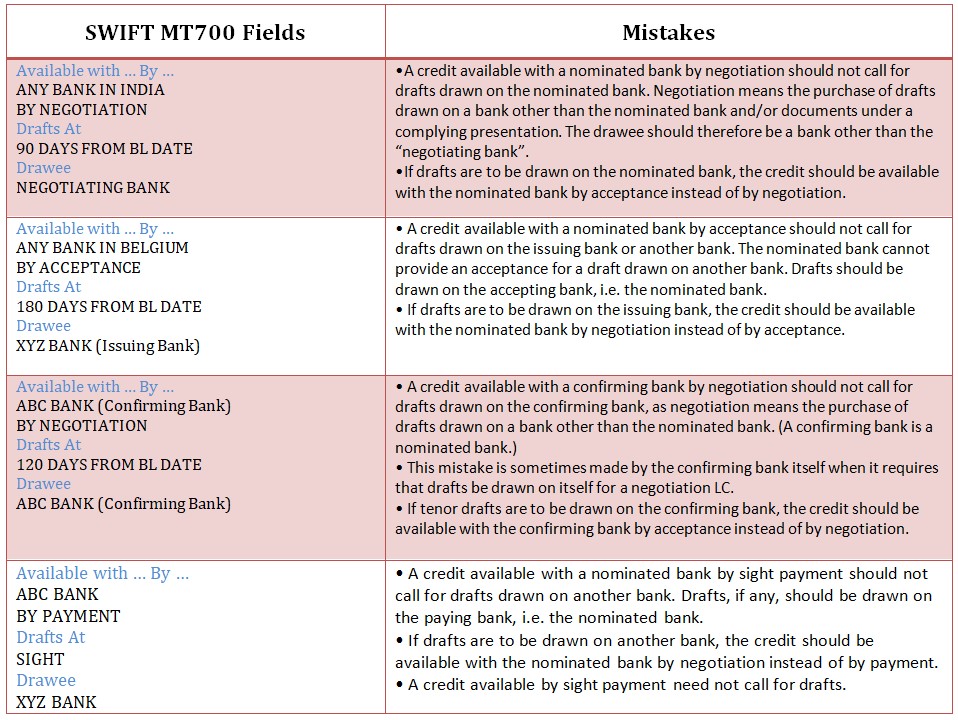

Incorrect availabilities on documentary credits

Documentary credit practice is not without problems.

Some LCs are unfortunately incorrectly issued in relation to the UCP 600’s provisions on availability. A few examples are illustrated in the table below.

Differences between deferred payment and negotiation credits

It is often explained that the key difference between availability by deferred payment and availability by negotiation is the non-use of drafts in deferred payment credits.

This is incorrect.

Credit can be issued available by negotiation without calling for drafts, and hence, the use or non-use of drafts is not the differentiator between the two types of credit.

The key distinction for what makes a deferred payment credit is that it is honoured by incurring a deferred payment undertaking.

A nominated bank is authorised to incur a deferred payment undertaking for a complying presentation and to prepay its deferred payment undertaking.

There is no provision in UCP 600 for a bank to prepay or “discount” the deferred payment undertaking of another bank.

The nominated bank acts on its nomination by incurring a deferred payment undertaking and paying at maturity or prepaying.

In a credit available by negotiation, the nominated bank negotiates (not honours) a complying presentation by purchasing drafts (drawn on a bank other than itself) and/or the documents.

The nominated bank is authorised to advance monies or undertake (agree) to advance monies that are due at maturity from the issuing bank.

A credit available by deferred payment can either be available solely with the issuing bank or also be available with a nominated bank.

Whereas if credit is to be available by negotiation, it ought to be available with a nominated bank, as negotiation can only be performed by a bank other than the issuing bank.

Differences between acceptance and deferred payment credits

The key difference between availability by acceptance and availability by deferred payment is the use of drafts in acceptance credits.

The use and non-use of drafts is the key differentiator between these two types of credit.

An acceptance credit is honoured by the acceptance of a draft for a complying presentation.

A nominated bank is authorised to accept a draft drawn on it by the beneficiary and to prepay or purchase its own acceptance.

It does not prepay or purchase drafts drawn from another bank.

In a credit available by deferred payment, the nominated bank honours a complying presentation by incurring a deferred payment undertaking independent of a draft.

Both acceptance credits and deferred payment credits can either be available solely with the issuing bank or also be available with a nominated bank.

Where drafts drawn on a nominated bank were not accepted by the nominated bank, it is not necessary to draw drafts for the issuing bank’s acceptance, as an issuing bank must honour when a complying presentation has been made to a nominated bank.

If a nominated bank does not incur a deferred payment undertaking, it is not necessary for the issuing bank to issue a separate deferred payment undertaking, as an issuing bank must honour when a complying presentation has been made to a nominated bank.

Differences between negotiation and acceptance credits

The key difference between availability by negotiation and availability by acceptance is that in negotiation, the nominated bank is making an advance on another bank’s undertaking to honour (the issuing bank’s), whilst in acceptance, the nominated bank is providing its own independent undertaking to pay and thereby honouring.

Drafts, when used in negotiation credits, are to be drawn on a bank other than the nominated bank.

Drafts for an acceptance credit are drawn on the nominated bank.

Credit can be available by negotiation without requiring drafts, and negotiation includes the purchase of documents without drafts.

A credit available by acceptance is honoured by acceptance of a draft and payment thereof at maturity.

Negotiation is the nominated bank’s purchase of drafts (when required in a negotiation credit) drawn on another bank, whereas in an acceptance credit, purchase or prepayment by the nominated bank is on accepted drafts drawn on itself.

For a credit available by negotiation, only a nominated bank can negotiate.

An acceptance credit can be available with a nominated bank or be available solely with the issuing bank.

(Where credit is available by acceptance with the issuing bank only, drafts drawn will be on the issuing bank.)

Differences between negotiation and sight payment credits

It ought to be mentioned that sight payment can be a payment term for a credit available by negotiation.

The key difference between sight availability by negotiation and availability by sight payment is the difference between ‘negotiation’ and ‘honour’.

For a credit available by negotiation, a nominated bank that agrees to act on its nomination may advance funds when it determines that the presentation is complying, or set a date by which to advance funds according to its estimation of when reimbursement will be received.

For a credit available by sight payment, a nominated bank that agrees to act on its nomination shall pay when it determines that the presentation is complying.

A credit available by sight payment can be available solely with the issuing bank (i.e. not available with a nominated bank).

Credit cannot be available by negotiation without a nominated bank.

A nominated bank that is not a confirming bank has no obligation to honour or negotiate.

When it does honour or negotiate, it ought to make it clear to the beneficiary, the issuing bank and the confirming bank (if any), that it has thus acted.

This is because when the nominated bank honours or negotiates a complying presentation, it is in its interest to remove any doubt that it has done so, to protect its right to be reimbursed by the issuing bank and/or a confirming bank.

Receipt or examination and forwarding of documents by a nominated bank that is not a confirming bank do not make that nominated bank liable to honour or negotiate, and do not constitute honour or negotiation.

The undertaking of an issuing bank and a confirming bank to reimburse a nominated bank is independent of their undertaking to the LC beneficiary.

If a nominated bank is taking the risk of the issuing bank or a confirming bank to provide financing under an LC, it would be wise to make sure that the issuing bank and/or confirming bank shall be obligated to reimburse it at maturity.

This is why a nominated bank ought to take care that it not only acts but is able to evidence that it has acted, pursuant to the provisions of UCP 600 when it finances under a letter of credit.

ARTICLE: Negotiable instruments are going through a makeover – the who, what, where, why

Type of availability to the credit beneficiary

The beneficiary is the most important party to a documentary credit because the LC is for its benefit.

The location of a nominated bank close to the beneficiary may be an important factor in the timely presentation of documents.

(If

eUCP credits and electronic presentations are used, physical proximity to the bank to whom presentations are to be made becomes immaterial.)

The type of availability of the credit, and with whom the credit is available, are important to the beneficiary because of these questions:

– When will it be paid for a complying presentation?

– Does it wish to be paid before reimbursement is due from the issuing bank?

– Is the nominated bank agreeable to advance funds or prepay before maturity?

– Which type of availability is the nominated bank willing to act on?

Having an understanding of the types of LC availability, and the differences between them will help the beneficiary formulate the terms of the letters of credit that it would be willing to accept and mention such terms in their discussions and sales contracts with their clients.

Incoterms – All you need to know

The Incoterms are a series of pre-defined commercial terms designed to help prevent confusion in foreign trade contracts by clarifying the obligations of buyers and sellers.

While they are in heavy use today, their origin dates back to the early 20th century.