Estimated reading time: 5 minutes

The dematerialisation of invoices and other supply chain documents is set for rapid growth. Most importantly, the B2B market can be expected to build on the success of larger enterprises in automating their accounts payable and receivable processes to spread e-invoicing practices to small and medium-sized enterprises (SME).

This endeavour will be supported by public policies to create mandates in many countries for the compulsory use of e-invoicing in public procurement and to produce data for the tax reporting of VAT and similar indirect taxes.

Many governments have implemented such measures, including the Latin American countries that acted as pioneers in the development of continuous transaction controls (CTC) and digital reporting requirements (DRR), and are now joined by others in Europe, the Middle East and Africa, and across Asia.

Brief historical background

As a context for these developments, let us recount the evolution of e-invoicing over the last decade or so. For more than fifteen years, the European Union (EU) has adopted bold policy positions to promote and support electronic invoicing.

This includes putting it on the same legal and fiscal basis as paper with rules for authenticity, integrity, and legibility (2010) and covering both structured machine-readable invoices (e.g., XML) and unstructured formats presented in the form of PDF.

In 2014, the EU legislated to require all public contracting authorities, at all levels, to be able to receive e-invoices in a prescribed standard which came into existence as a European Norm (EN 16931). The standard was published in 2017, but the legislation relied on voluntary adoption on the sender side, although Member states were free to issue mandates to compel adoption by suppliers.

The focus is on the public sector, where the EU felt it had direct leverage, rather than a ‘whole economy’ approach. The result has been a variable take-up, which is now the subject of a post-implementation review that could lead to further policy action.

In the US, the Federal Reserve Bank of Minneapolis has for some years been facilitating the Business Payments Coalition (BPC), which has an agenda to promote the use of electronic means of payment and the complementary use of e-invoicing to reinforce each other.

These public policy initiatives are supported by a growing service and solution provider community which has had considerable success in automating large corporate supply chains; 80% e-invoicing penetration is now quite common in that segment.

E-invoicing for SMEs

With the exception of Nordic countries, there is still limited success in the SME market, where the business case is a challenge in such a heterogeneous space. Elimination of paper by PDF is actively used in this sector, although its benefits are much less than full automation.

The SME segment requires significant effort by all stakeholders, for example among service providers, ERP and software providers, networks, accountants, and financial institutions.

The size of the prize is huge, with benefits in terms of reduced costs, more rapid trade payments from buyers to sellers, reduced errors and fraud, transparency, and more satisfied supply chains.

SMEs may, however, struggle to make the business case and dedicate their scarce internal resources to implementation. They need easy-to-use solutions, offering the functionality to provide peace of mind, data compliance, full traceability, and a return on investment.

Next steps for e-invoicing

Network solutions that provide end-to-end interoperability between trading parties are growing in importance. Some of these are national initiatives, such as Chorus Pro in France and SdI in Italy. These initiatives are usually related to the requirements for tax reporting by all enterprises, offering both direct submission and the use of service providers and software as a service.

Networks often provide mechanisms not only for reporting data to tax authorities but also for the transmission of e-invoices and other documents to intended recipients. But these solutions are currently very different from one another, and the European Commission has started its VAT in the Digital Age programme (VIDA) to coordinate policy in this area and address intra-EU flows.

Consultation is underway. A recent initiative by an expert group from the private sector has proposed a Next Generation Decentralised CTC and Exchange solution (DCTCE), where the reporting mechanism for tax reporting is juxtaposed with a four-corner model for the delivery of invoices between trading parties.

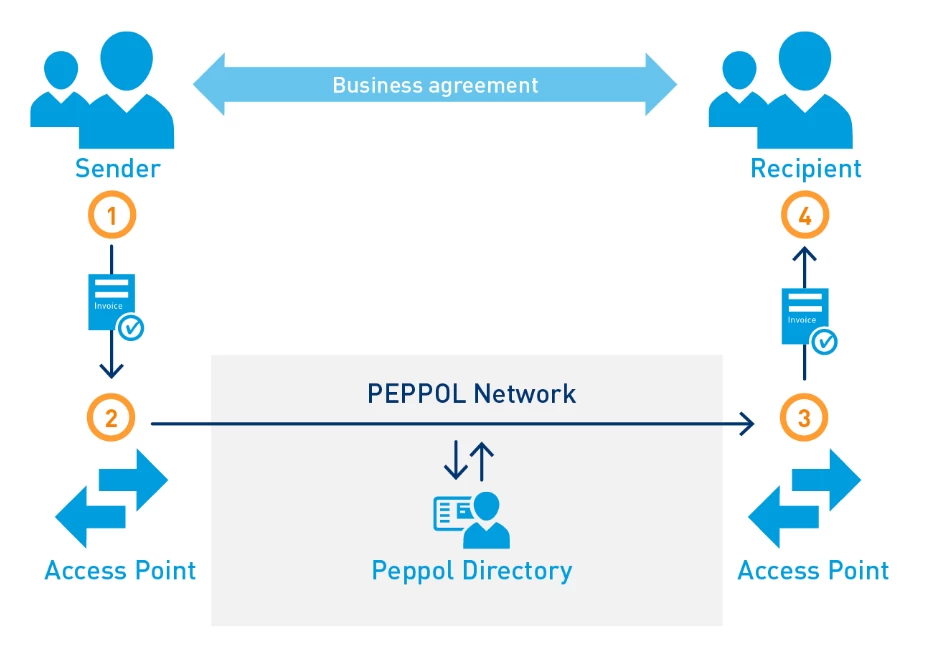

Peppol is an important global four-corner network that originated in Europe and is now present in many countries to support interoperability. Recent expansions have taken place in Singapore, Australia, New Zealand, and Japan. End-users (at corners 1 & 4) work with Access Point service providers (at corners 2 & 3) to transmit invoices and other documents in a standard form across a secure and reliable network using building blocks.

The Peppol network is provides for

- Delivery (transmission protocol and the trust infrastructure)

- Discovery (information about locations and capabilities of receivers)

- Data formats (standards with potential room for restrictions and extensions plus attachments)

- Governance framework (applicable rules).

Peppol Authorities at the country and global level provide oversight and support. Peppol is engaged in ambitious development plans to extend its geographic footprint and now also offers a generic module of services to support CTCs and DRR in the tax sphere.

In addition, its building blocks are finding favour in other interoperability networks such as the US BPC e-invoicing exchange framework, and the European E-invoicing Service Providers Association’s (EESPA) EIN.

Indeed, these various initiatives sharing these common, open standards-based building blocks are increasingly working together to coordinate and converge on common solutions for global interoperability. Interoperable network solutions are now a reality based on well-proven components to deliver automation and common standardisation.

An opportunity for collaboration

E-invoicing is helping to transform the supply chain finance industry with techniques such as factoring. Whereas an invoice is not a negotiable instrument, it is evidence of a receivable and acts as the workhorse of the open-account receivables finance industry.

In dematerialised form, the e-invoice opens opportunities for new financing models and partnerships between service providers and banks or fintechs. In turn, banks could help support e-invoicing with their online banking solutions and new payment initiation methods such as request-to-pay. There is great scope for cooperation and alliances in this space.

In summary, the period ahead is riding on the wave of governments simultaneously and perhaps serendipitously discovering the benefits of e-invoicing and data capture for ‘tax gap’ elimination. As these initiatives progress, mandates for adoption are becoming more common.

There is a strong challenge here to reap the benefits of supply chain efficiency at the same time as closing the tax gap. Coordinating these motivations for e-invoicing will create a win-win for all stakeholders.